Bitcoin is undergoing a multi-pronged attack on its spot market liquidity as exchange-traded funds, short-term speculators and cryptocurrency miners distribute assets simultaneously.

This coordinated selling pressure has reduced market demand at the fastest pace since the collapse of the Terra/Luna ecosystem in 2022.

As a result, the price of BTC has fallen 12% over the past week, pushing the top crypto to the $60,000 level amid heavy hedging activity from market traders. BTC is exchanging hands at $64,036 at the time of writing, according to Crypto Slates facts.

Yet this spot market flush has created a structural paradox that could still catapult BTC’s value.

The selling volume has left the derivatives market in increasingly lopsided shape, with a record wall of short positions now anchoring the market.

However, while traditional spot indicators point downwards, any selling pause could trigger a mechanical short squeeze, turning the traders who bet on Bitcoin into forced buyers fueling the next rally.

Bitcoin ETF exodus trails AI trading

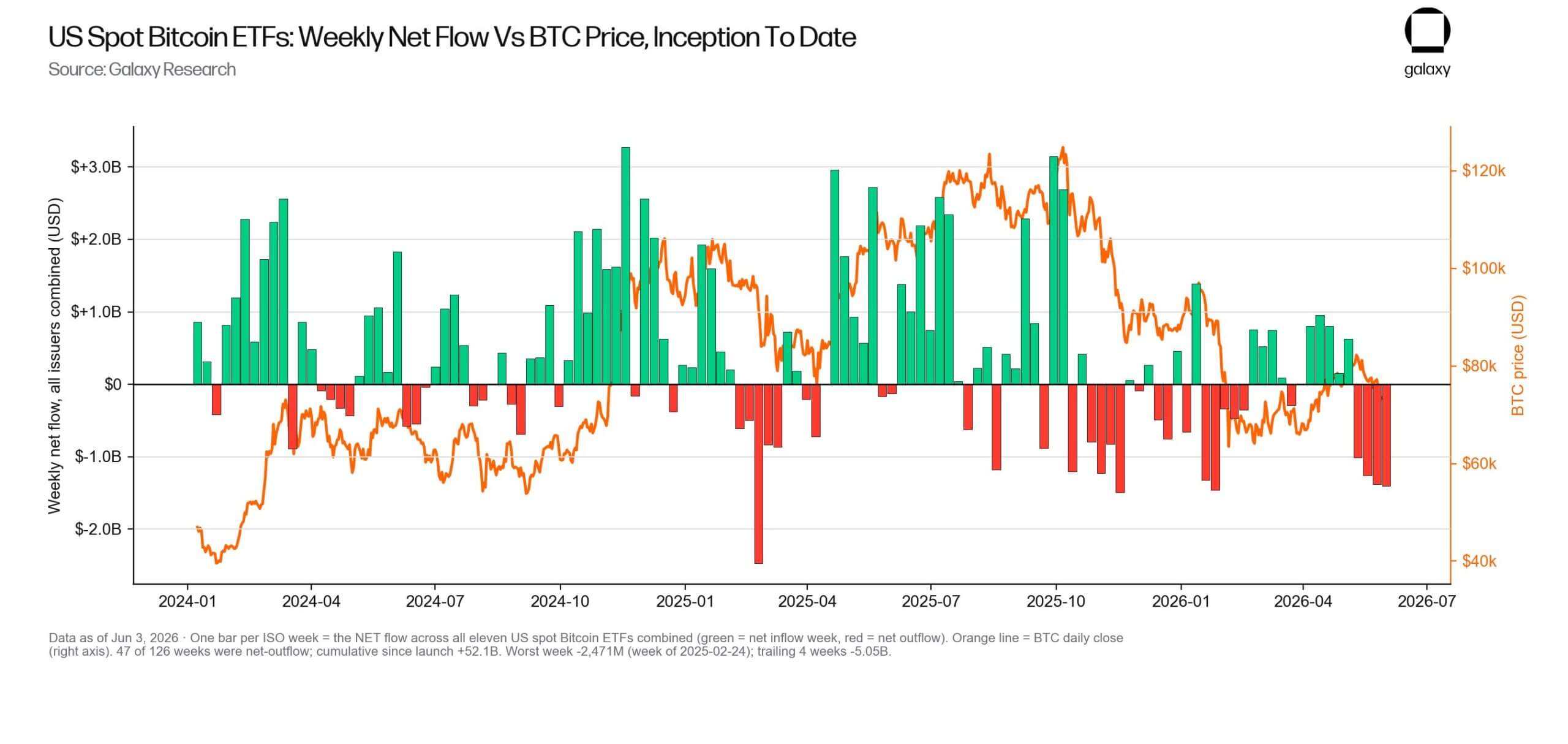

The main cause of Bitcoin’s recent price weakness is a sharp reversal in institutional capital flows. Spot Bitcoin ETFs recently recorded a 13-day streak of consecutive liquidations between mid-May and early June.

According to Galaxy Research, these funds have lost 59,351 BTC, removing approximately $4.33 billion from the market.

Over a seven-day period, the funds lost $2.78 billion, representing the worst outflows ever for Bitcoin. The bleeding continued for a period of ten days, with an outflow of $3.06 billion. In the 14-day period, $4.21 billion left the market, while in the 20-day period, an outflow of $5.42 billion was recorded, losing 73,080 BTC.

Galaxy research noted this 20-day period is the largest outflow window ever recorded, both in terms of dollar value and total Bitcoin volume.

Industry executives view this as a macroeconomic realignment rather than an internal failure of the digital asset class. Traditional capital markets are currently pumping approximately $400 billion into artificial intelligence infrastructure over a six-month period.

Michael Saylor, Chairman of Strategy, said:

“This is a capital rotation, not a Bitcoin squeeze. Capital markets are financing AI expansion on a historic scale. Volatility creates opportunity.”

Jeff Park, an advisor at Bitwise, echoed this sentiment. He suggested traders are tapping into their Bitcoin allocations to fund the coming “hot moneyball” trades in the market, shifting liquidity to chase tech companies like SpaceX and Anthropic.

Going forward, Park noted, this correlation breakdown itself will become the fuel for future market movements.

Speculative panic and capitulation of miners

As institutional support declined, private and short-term investors entered a phase of outright capitulation.

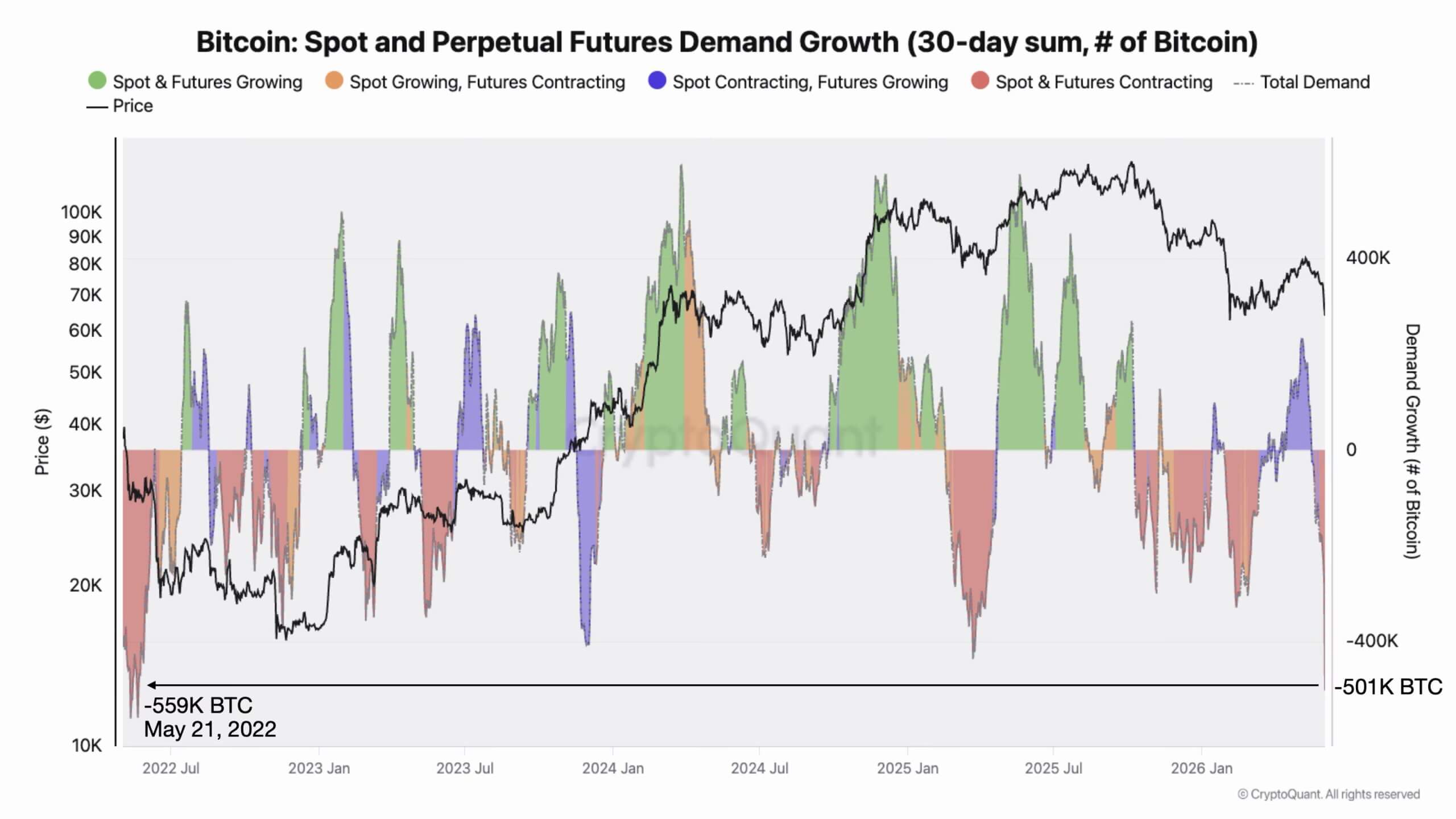

Data from CryptoQuant shows that total demand for Bitcoin, which is a combination of speculative and spot market purchases, shrank by 501,000 BTC in the past month.

At the same time, short-term BTC holders are responsible for the most concentrated loss-driven transfers of the year.

Over a 24-hour period, these holders moved 53,800 BTC directly to exchanges. CryptoQuant researchers highlighted the critical split: 100% of these coins moved while making a loss, while inflows on the profit side fell to zero.

This means that these underwater buyers choose to liquidate their positions immediately in market weakness, rather than waiting out volatility.

Historically, CryptoQuant noted, spikes in loss-driven inflows from short-term holders cluster around local capitulation events. They highlight weak hands, washouts, and the transfer of supply from over-indebted latecomers to higher-conviction holders.

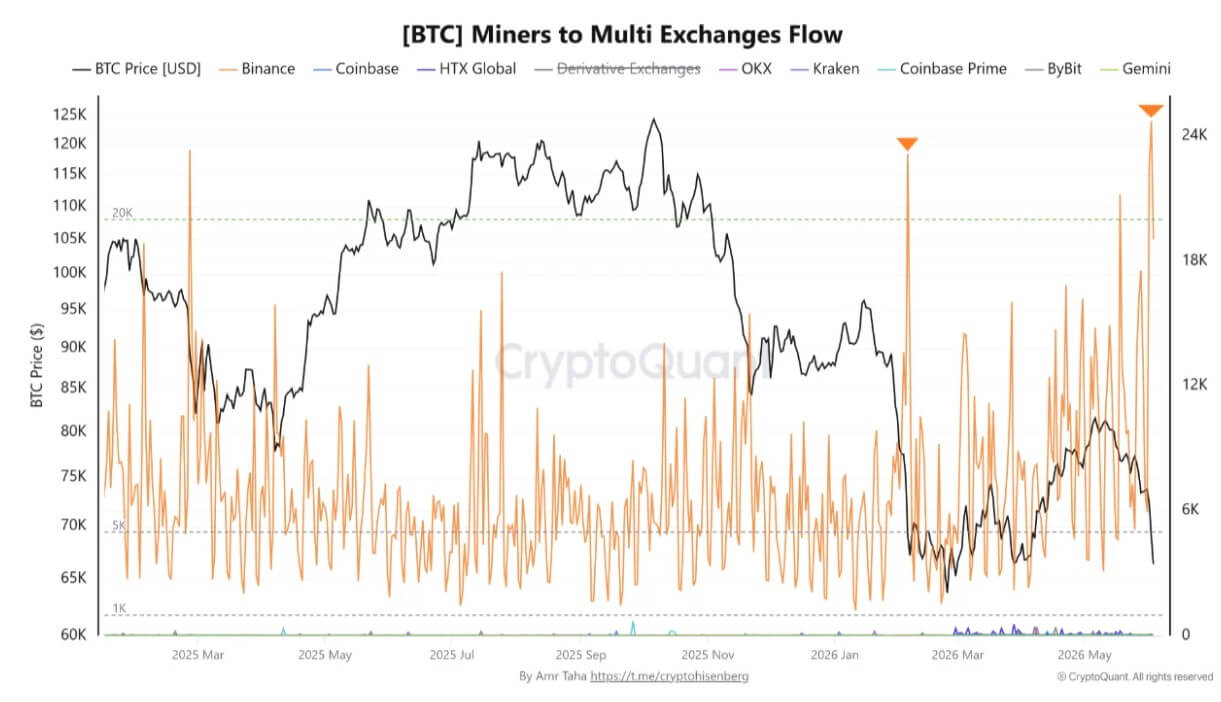

To supplement the overhead supply, BTC miners also move coins. CryptoQuant noted that on June 2, Bitcoin miner inflows to the Binance exchange spiked to 24,716 BTC, surpassing the February peak by 6.8%.

CryptoQuant researchers pointed out that the large influx of miners does not confirm immediate sales on the open market. Miners often move coins for strategic purposes, including hedging, liquidity management, or rebalancing the internal treasury.

However, concentrating this volume of Bitcoin on a single exchange means that miner-managed supply has shifted right next to market liquidity.

If these inflows remain high in the coming days, traders may interpret the data as a sign of a renewed distribution of miners.

The supply absorption puzzle

This relentless selling creates a structural puzzle compared to long-term accumulation data. As short-term speculators flee, sophisticated investors aggressively absorb the overhead supply.

Brian HoonJong Paik, CEO of Bitcoin-focused company Smash Fi, pointed out that long-term holders added 200,000 BTC to their wallets this month and now hold 16.3 million BTC, which is close to their highest holdings ever.

Paik said:

“The people who have held Bitcoin the longest are not selling this weakness. They are buying your panic.”

Still, the sheer number of coins hitting the market indicates a massive change in ownership.

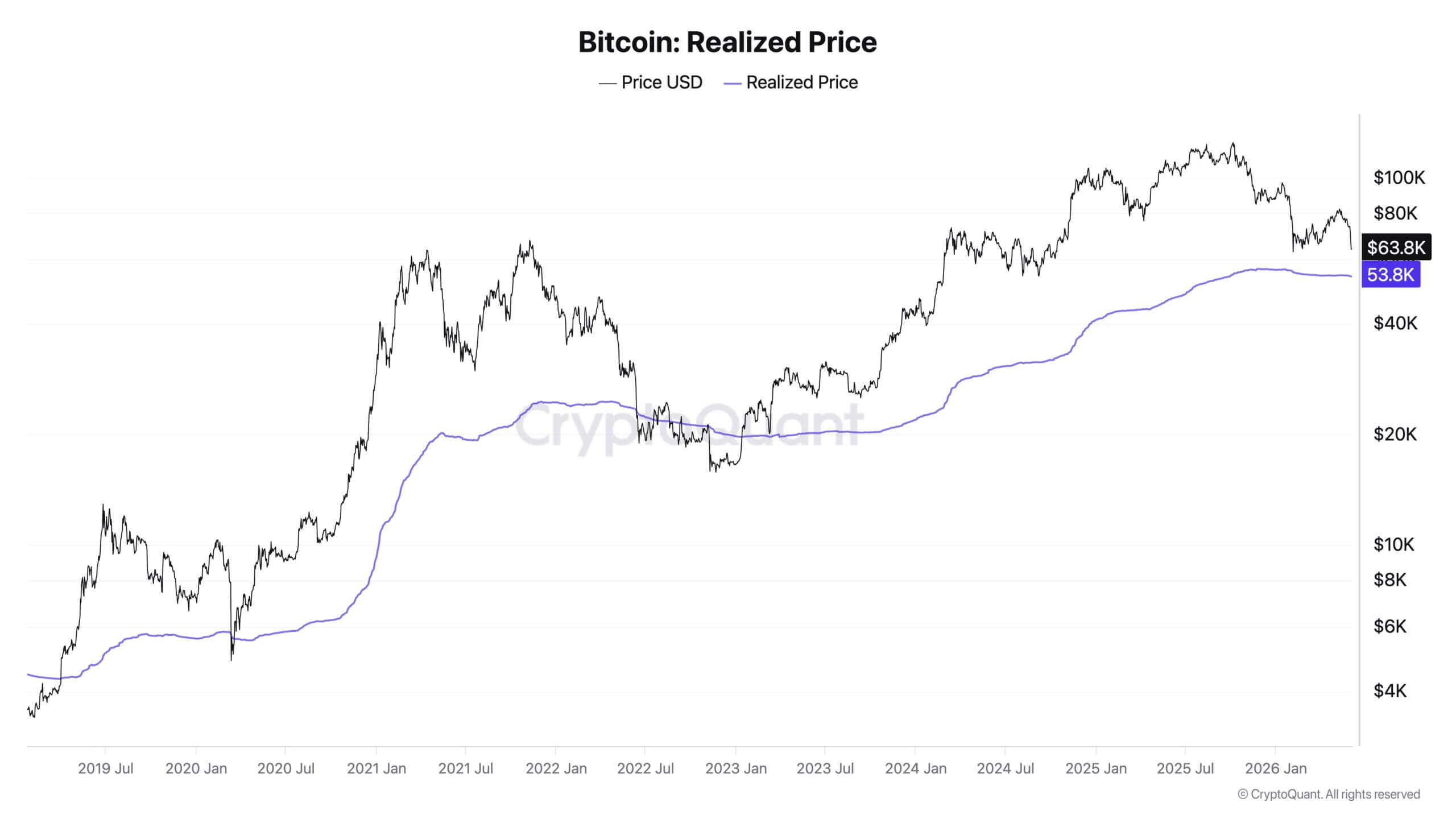

CryptoQuant CEO Ki Young Ju noted that historically, bear markets only end after the spot price falls below the realized price. This metric places the current average investment cost basis around $53,000.

Reaching that level should theoretically prove difficult, however, given the wall of institutional capital that has invaded the market.

Ki Young Ju broke down the math to illustrate the extent of this absorption: Since January 2023, Strategy (formerly MicroStrategy) has bought 711,206 BTC and sold only 32, effectively locking up 711,174 coins.

Additionally, since Bitcoin traded at $63,000 in March 2024, spot ETFs have absorbed an additional 509,102 BTC, while Strategy acquired an additional 650,706 BTC.

In total, institutions swallowed 1,240,808 BTC, but the spot price remains anchored at the same level.

For context, total global foreign exchange reserves hover around 2.7 million BTC, and Satoshi Nakamoto’s estimated assets are around 1 million BTC.

Even though the market absorbs a supply shock greater than Satoshi’s entire supply, the price remains low.

This dynamic highlights that while traditional long-term holders and institutions are accumulating heavily, an unusually motivated cohort of sellers continues to hold back any upward momentum.

BTC’s coil spring setup

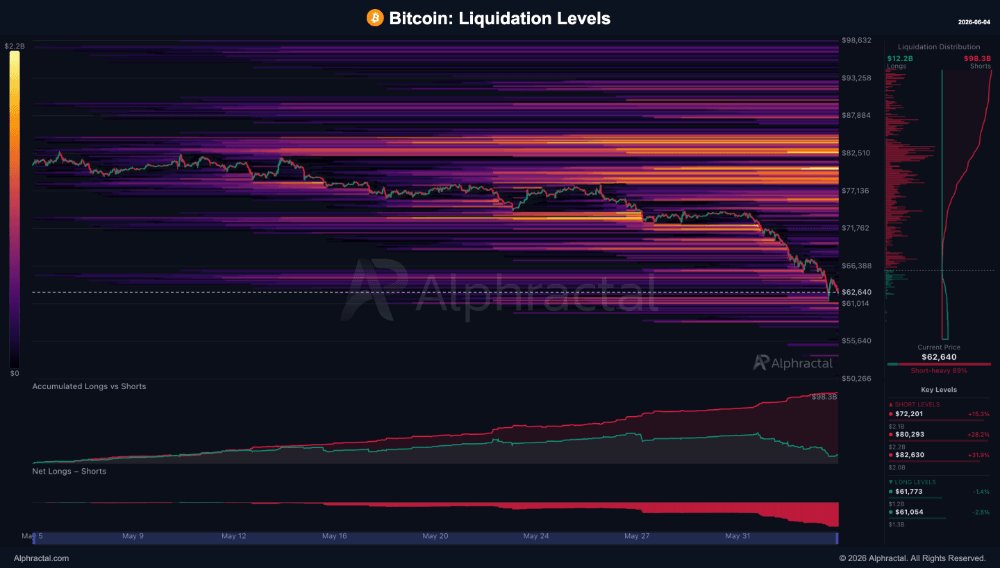

While the spot market paints a picture of exhaustion, the derivatives market has turned into a coiled spring. The rush to short Bitcoin during this crisis has created a top-heavy leverage structure.

Facts from analytics firm Alphractal shows a dramatic 72-hour shift in the global liquidation map. On the first day of the flush, the market was 66% short-heavy.

On day two this reached 76%. On day three, the market shifted to an extreme short position of 89%. The benchmark now has $98.3 billion in short positions versus a long stack of $12.2 billion.

The short-to-long ratio is 8.06x. Since the market has already wiped out most leveraged long positions, downside risk remains limited on the chart. The downward magnetic level of $61,054 implies only $1.3 billion in long-term liquidations.

Conversely, the uptrend is heavily clustered with short liquidation triggers. A modest upward move opens three waves of forced buying: $2.1 billion at $72,201; another $2.2 billion for $80,293; and a final layer of $2.0 billion resting at $82,630.

According to Alphractal, short sellers have piled on more than $6.3 billion in sensitive liquidation triggers that are between 15% and 32% above the current spot price.

The closest structural analogy to this data set occurred in November 2022, when the same metric printed a short-heavy value of 84%. Over the next 11 sessions, Bitcoin rose by about 24%.

Bitcoin is currently facing undeniable pressure from miners, panicky retailers and fleeing ETF capital.

However, by allocating too much in bearish trades, the market has set a mechanical trap.

The underlying selling pressure remains real, but the resulting structural imbalance means that the slightest break in spot distribution could easily trigger a violent upward cascade, driven entirely by the traders betting on Bitcoin’s decline.