Bitcoin’s ongoing price correction is deepening as US investor demand weakens, leaving the world’s largest cryptocurrency increasingly exposed to leveraged positions below $60,000.

According to Crypto Slates data, the top crypto was trading at $59,800 at the time of writing, down 16% this month. This decline has brought the asset closer to price levels where forced liquidations could intensify selling pressure.

Record withdrawals from US exchange-traded funds, deteriorating performance during US trading hours and defensive positioning in the options market indicate that buyers have not yet regained control.

Without a recovery in spot market demand, Bitcoin risks sliding towards a critical test of support below $60,000.

US demand is weakening despite a friendlier policy environment

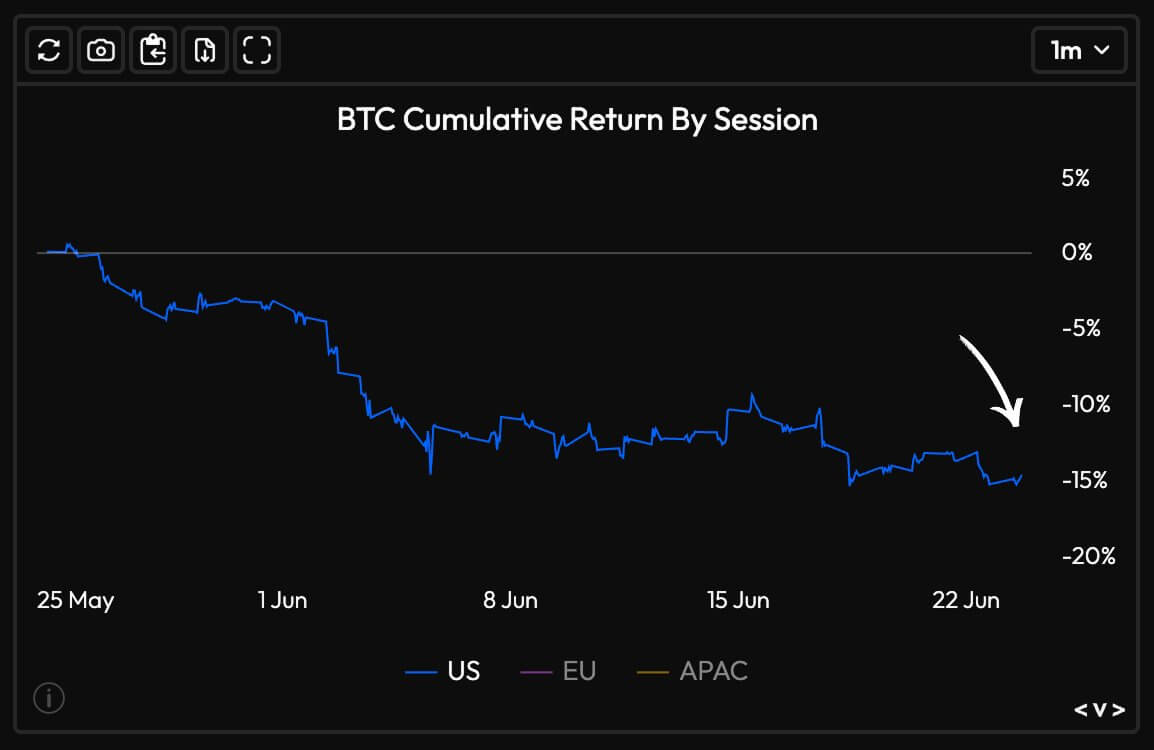

The clearest sign of weakening US demand came during US trading hours, a period that previously benefited from stronger exchange activity and buying by institutional funds.

Velo data showed that Bitcoin’s cumulative return during the US session over the past month was around -15%. A strategy that held Bitcoin only during those hours would therefore have posted a 15% loss, indicating that the US session has become a source of selling pressure rather than support.

This achievement stands in contrast to the country’s increasingly favorable attitude towards the cryptocurrency industry.

Over the past year, President Donald Trump’s administration introduced a more supportive policy environment than its predecessor, reinforcing expectations that the US would become a leading center for digital asset investment.

However, this political shift has not translated into sustained buying during Bitcoin’s latest decline.

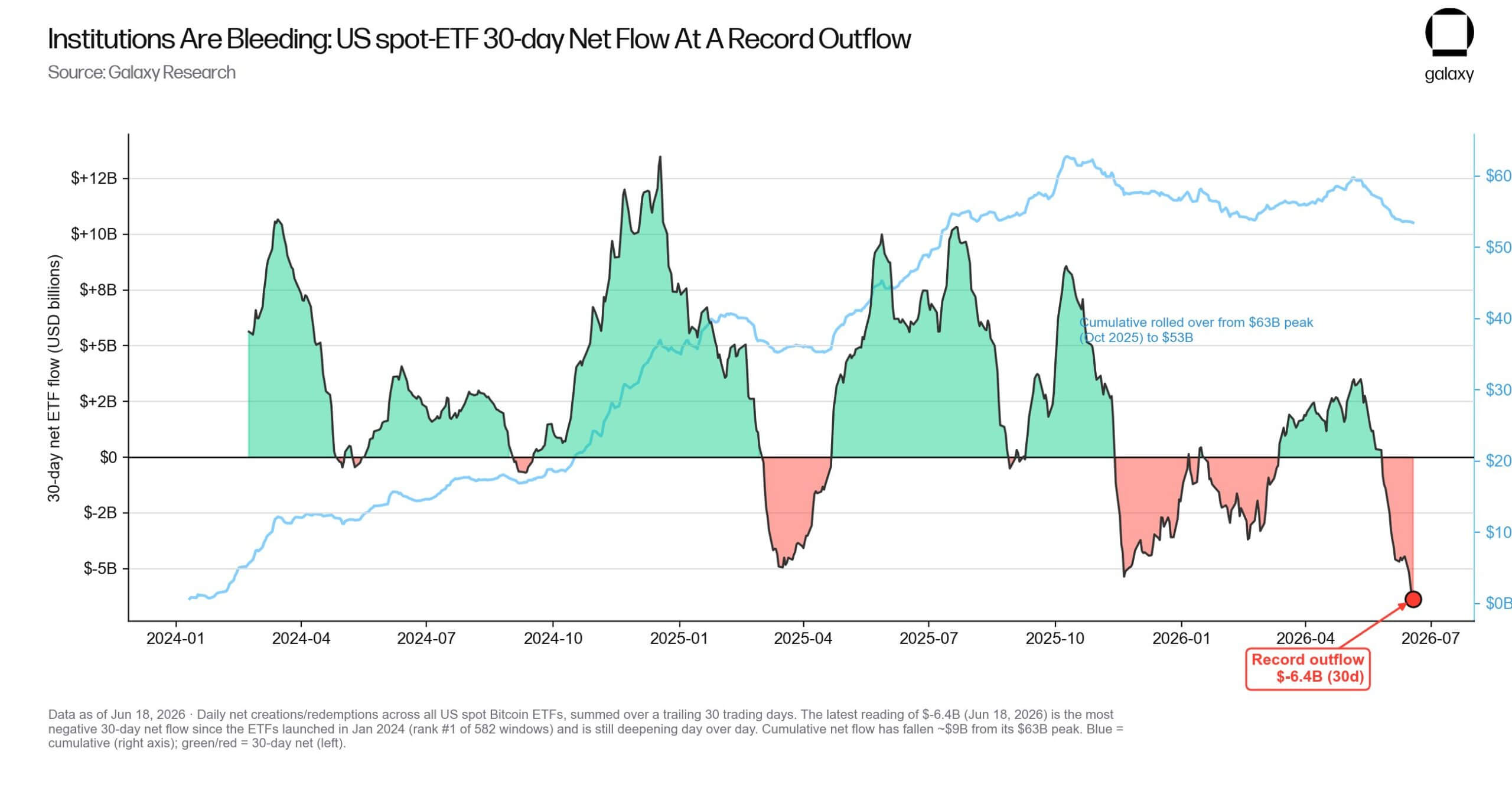

Evidence of this weakening of BTC demand can also be seen in flows into regulated investment products.

According to data from Galaxy Research, US exchange-traded Bitcoin exchange-traded funds have recorded a net withdrawal of approximately $6.35 billion over the past 30 days. This is the largest outflow among the 582 rolling 30-day periods covered by the company’s analysis.

While the drawdowns don’t necessarily indicate that every ETF investor has turned bearish, the magnitude of the redemptions has weakened a source of demand that has helped absorb Bitcoin supply during previous rallies.

Additionally, the Coinbase Premium Index has also remained negative at around -0.13. The measure compares the price of Bitcoin on Coinbase to prices on offshore exchanges and is often used to gauge relative demand from US investors.

The index has improved from its late February low of around -0.25, suggesting that selling pressure is less intense than it was then. However, the inability to return to positive territory shows that buyers on Coinbase are still unwilling to pay more than traders on offshore platforms.

Together, these data points show a broad pullback in U.S. demand, rather than an isolated decline on one exchange.

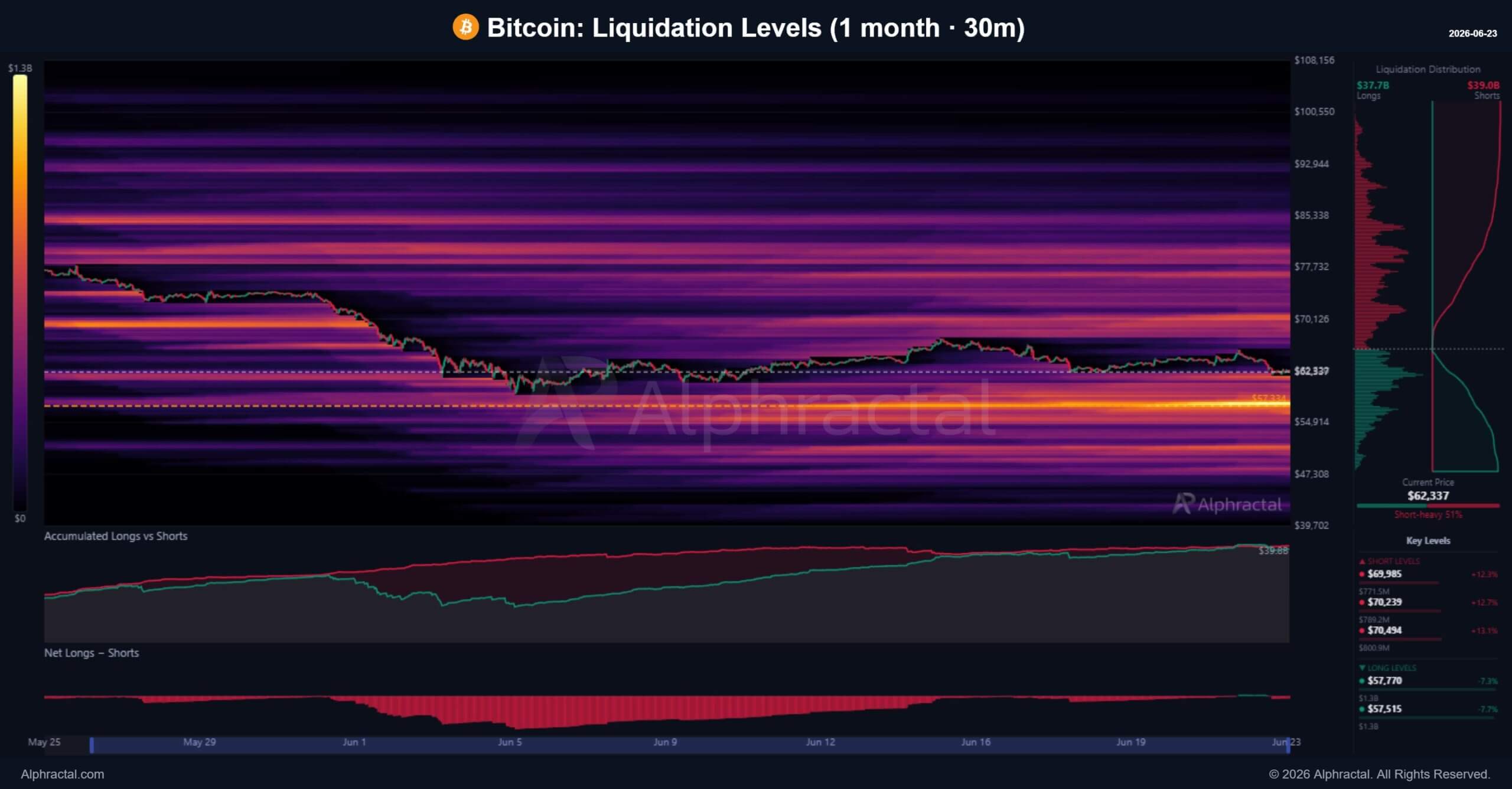

$57,300 emerges as the next leverage test

With demand in the spot market subdued, the market has become more sensitive to leveraged derivative positions.

João Wedson, CEO of analytics platform Alpharactal, identified $57,300 as significant liquidation level after examining data from 30 exchanges over the last 30 days.

Liquidation levels are price levels at which leveraged traders may no longer have sufficient collateral to maintain their positions. Exchanges can then automatically close these trades, adding sell orders to the market during a decline and potentially increasing volatility.

The concentration around $57,300 therefore represents a risk if Bitcoin falls below $60,000 and continues to lose strength.

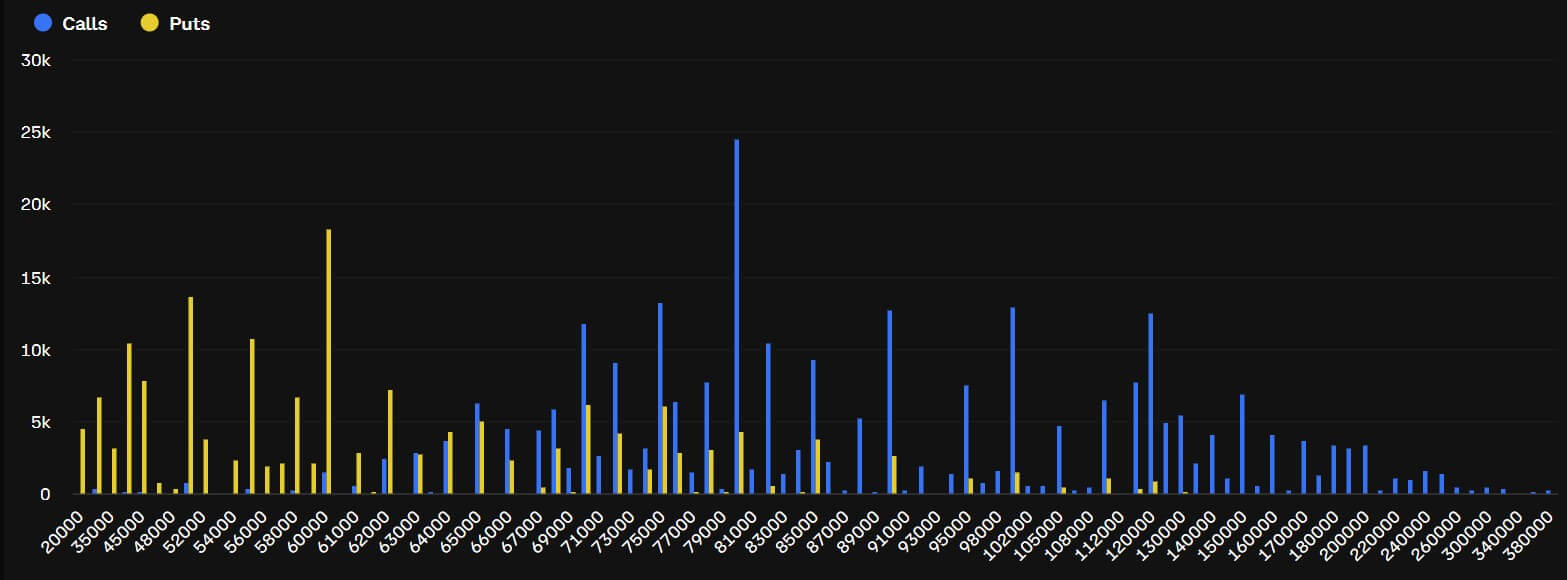

Derivatives traders on the Deribit options exchange in particular are actively positioning themselves for this downward scenario.

According to the company’s data, approximately $1.1 billion in positions are concentrated at $60,000, making that level an immediate point of interest. Another $1.4 billion was split between the $50,000 and $55,000 strikes.

The figures show substantial exposure to derivatives below current prices, although the data provided does not indicate that all positions represent outright bearish bets. Options can be used to hedge existing holdings, generate income, or build strategies involving multiple strikes.

Still, the accumulation shows how much attention has shifted from recovering from previous highs to managing the possibility of a deeper decline.

Weak demand makes Bitcoin’s recovery vulnerable

Bitcoin’s market structure suggests that buyers have yet to return with enough force to reverse the current decline, leaving short-lived recoveries vulnerable to renewed selling.

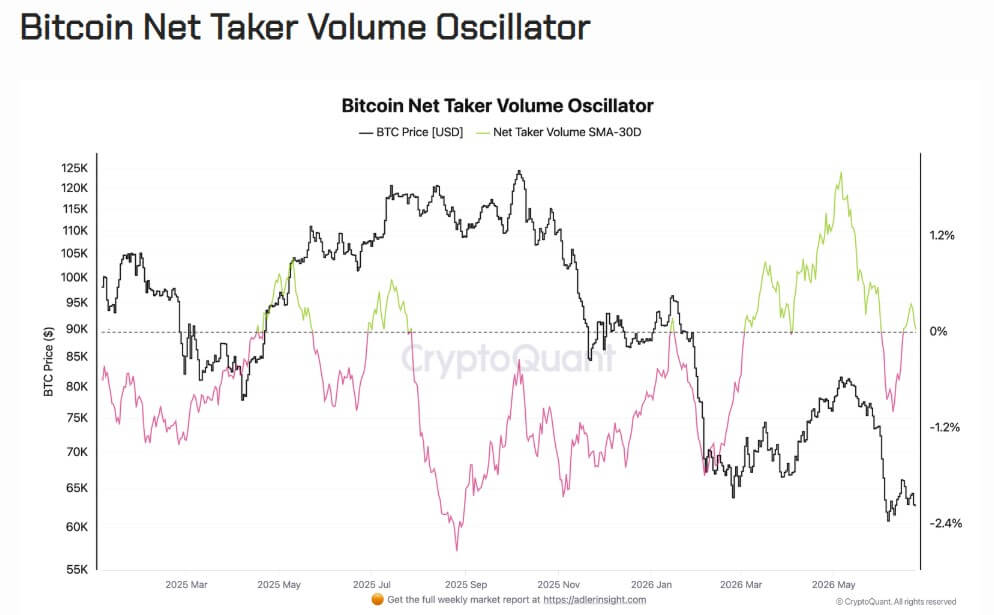

CryptoQuant analyst Axel Adler pointed to the Net Taker Volume Oscillator, which measures the difference between market buys and market sells and smooths the result with a 30-day moving average.

The indicator shows which side is trading more aggressively as market orders are executed immediately against available liquidity.

The oscillator remained solidly positive two months ago, climbing to around 1.7% in mid-May, as aggressive buying helped Bitcoin to local highs. It later fell to -0.9% during the early June sell-off before recovering to the zero line.

Although the return to zero indicates that the previous dominance of market sellers has waned, it does not indicate that buyers have regained control.

For a stronger recovery, the oscillator would have to move decisively above zero and stay there. This would be a signal that traders are once again willing to buy at prevailing market prices.

Adler said the current numbers instead reflect a balance, with insufficient demand-side initiative to support a sustainable recovery.

Liquidation activities reinforce that assessment. CryptoQuant’s liquidation oscillator was 18.4%, showing that long positions accounted for the majority of forced closes. That marks a sharp reversal from mid-May, when the indicator fell to around -13% as rising prices forced short sellers out of their positions.

This shift means that leveraged buyers are now absorbing a greater share of market losses. It also increases the risk that short rebounds will attract new long positions that can be liquidated if Bitcoin resumes its decline.

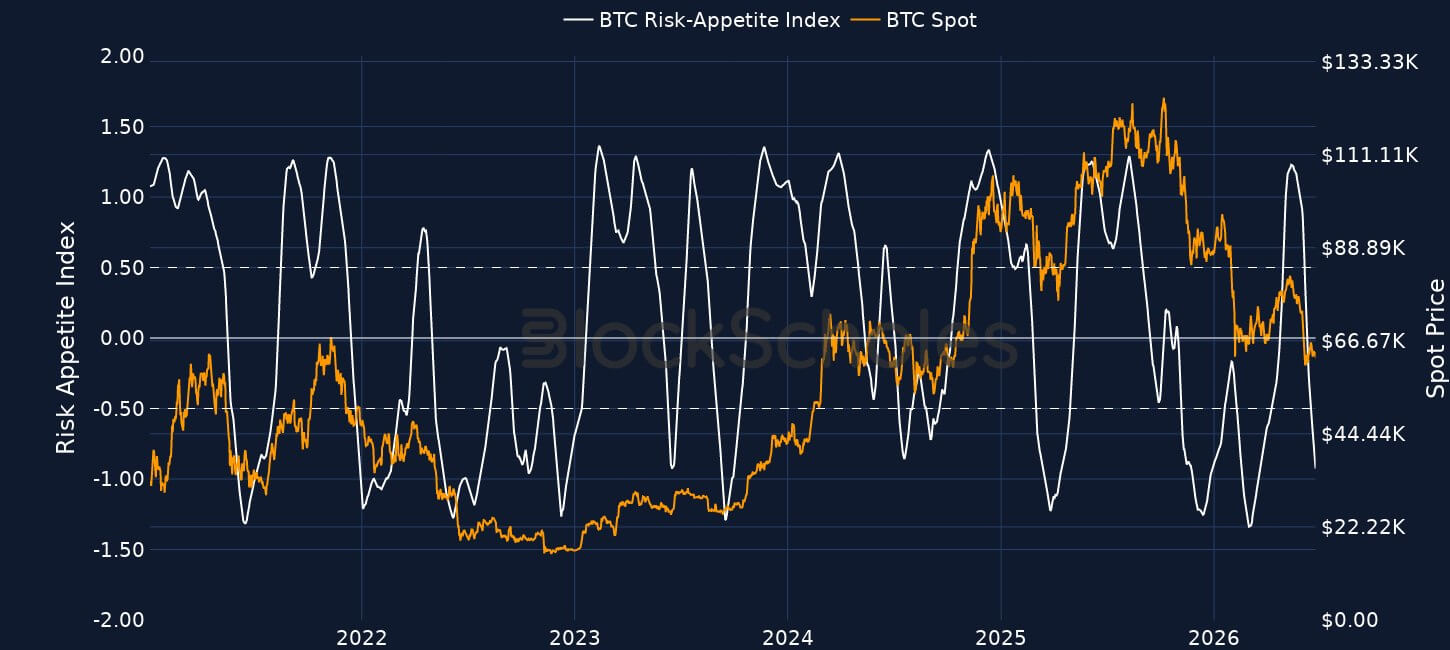

Block Scholes’ risk appetite indicators point to a broader pullback. The Bitcoin measure has moved closer to the -1.0 threshold associated with weak risk appetite, and has previously shown greater resilience than ETH.

Indeed, Ethereum had already entered weak risk territory, but Bitcoin’s continued deterioration has narrowed the gap between the two assets.

The convergence suggests that investors are reducing their exposure to the cryptocurrency market rather than treating Bitcoin as a relative haven.

Together, the indicators show that selling pressure has diminished without meaningful returns for buyers.

Until demand for market orders strengthens and prolonged liquidations subside, Bitcoin’s recovery will provide temporary relief rather than mark the start of a sustainable recovery.