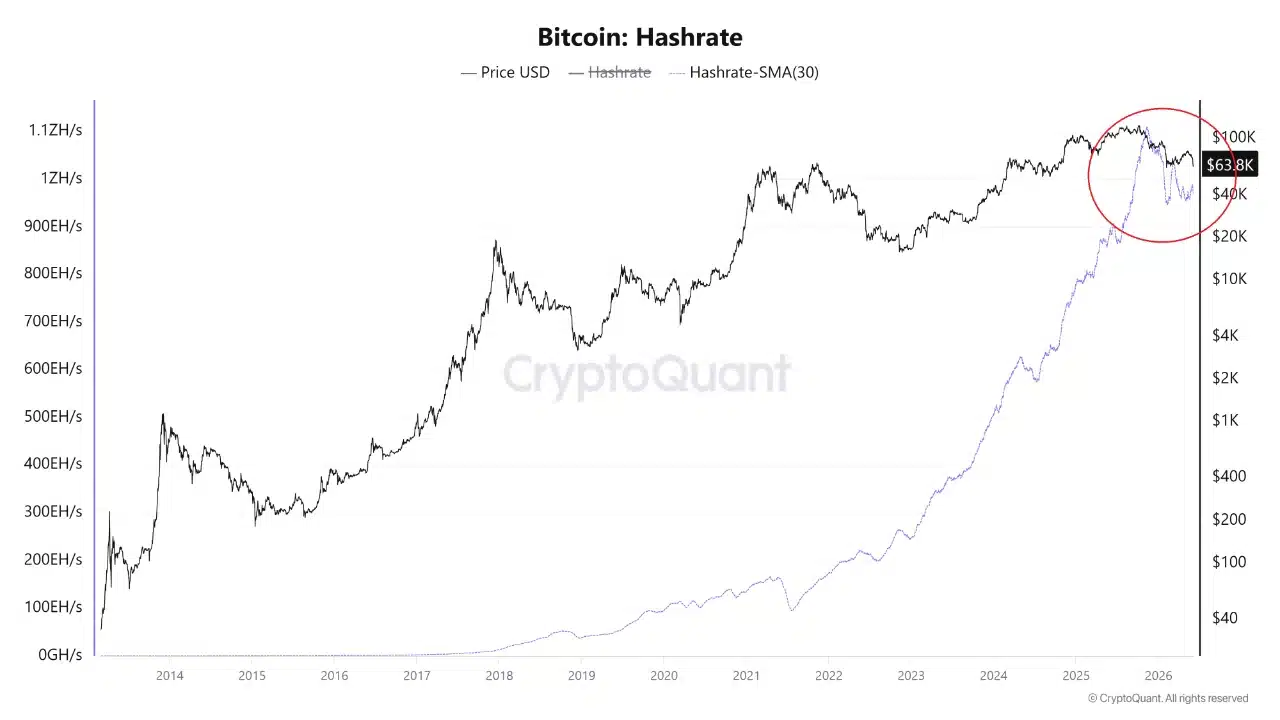

Since December 2025, Bitcoin [BTC] hashrate has slowly decreased. After a near-continuous increase in hashrate from the third quarter of 2021, the downturn over the past six months is concerning.

In a post on CryptoQuant Insights, analyst Woominkyu pointed out that a meaningful drop in the 30-day moving average of the hashrate was not unprecedented. The most notable dips were during the 2021 mining ban in China and the bear markets of 2018 and 2022.

The current declines of roughly 6.6% in the 7-day MA and 3% in the 30-day MA are much shallower than previous capitulation events, the analyst noted. Instead, the hashrate rollover represented the capitulation of miners. This could lead to a market bottom in the coming months.

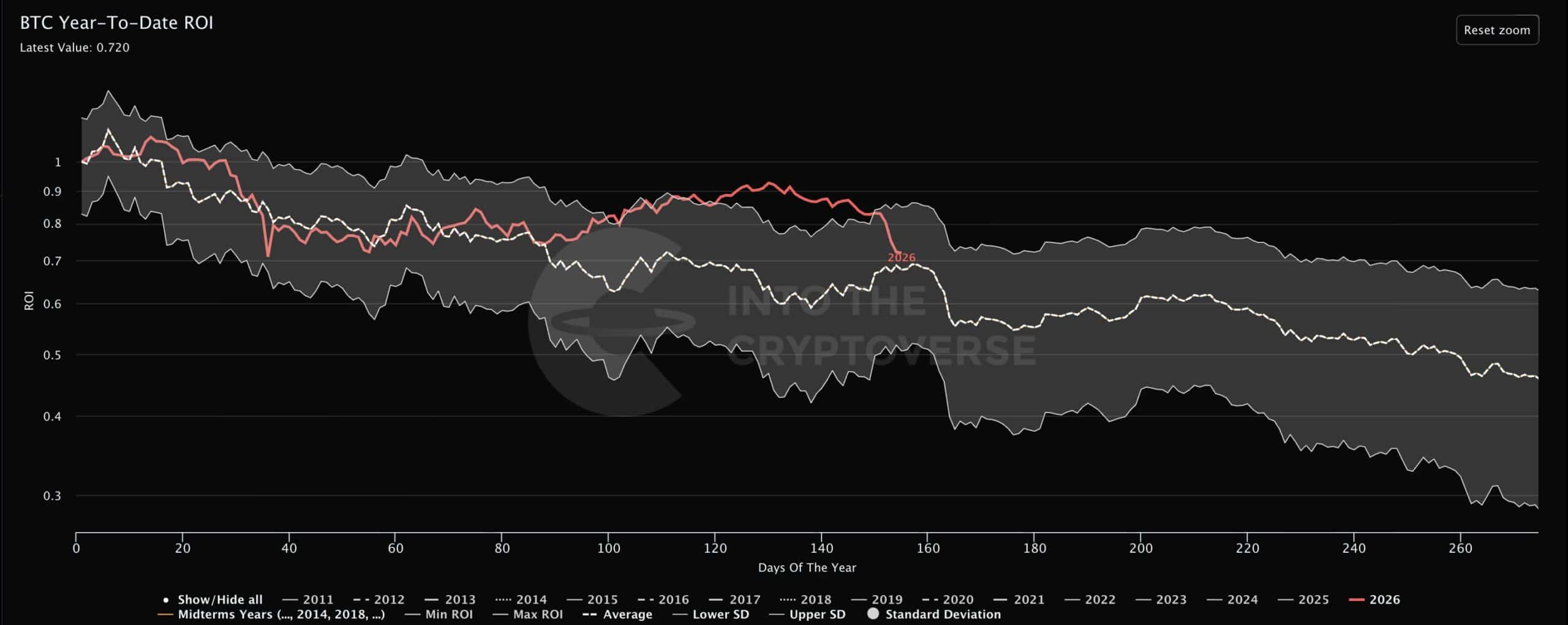

In a post on X, founder and CEO of Into The CryptoVerse, Benjamin Cowen, said

While these times may feel different, this is normally true BTC is in the middle years at this point.

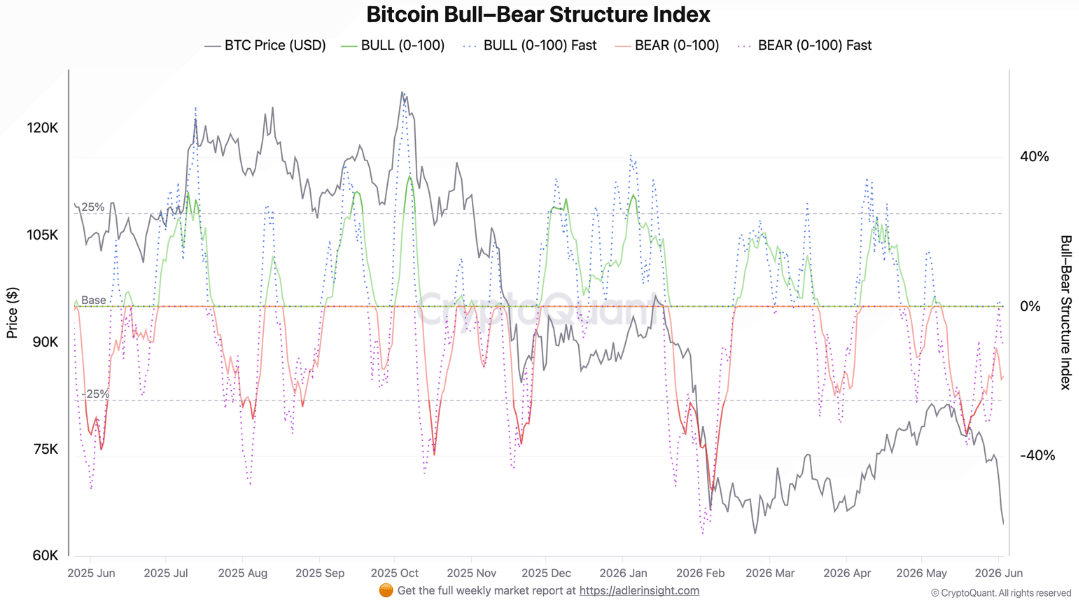

Bitcoin sentiment reaches extreme fear, but capitulation is yet to be seen

The bull-bear index takes into account factors such as spot aggression, OI, funding, ETF flows and currency flows. According to the same report, the BEAR side is active, but not near the -40% extremes that marked the severe sell-off in February.

The moderate capital outflows showed controlled weakness, and not an outright panicky capitulation in the Bitcoin market.

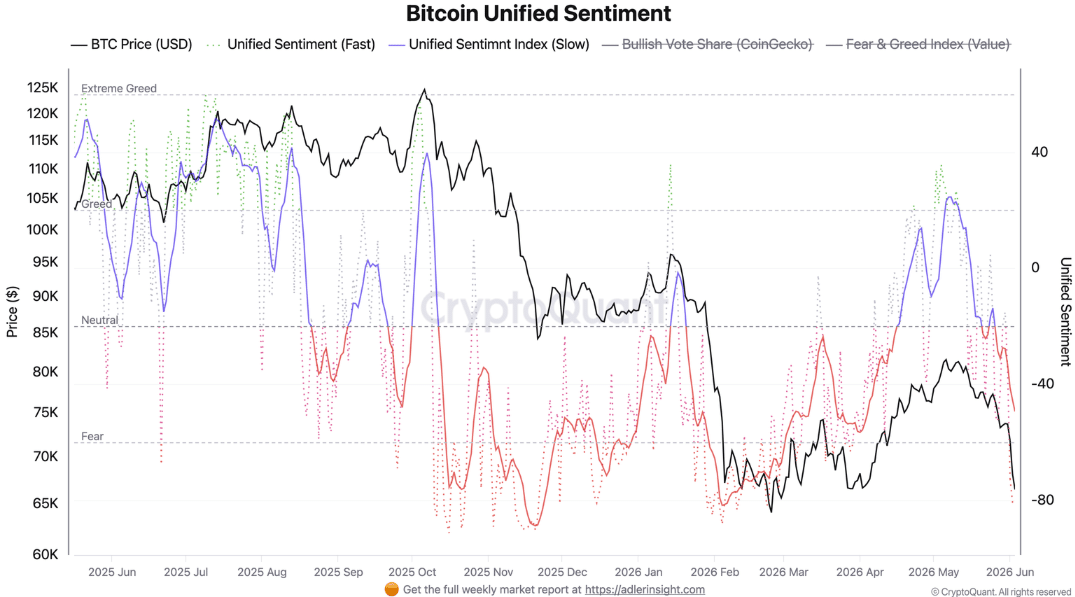

The sentiment has sunk through the floor. Extreme fear tends to give courageous buyers more risk/reward, but in itself extreme fear does not mean a bottom for the market.

Emotions have fallen more than capital flows, the analyst noted. It created an interesting scenario as Bitcoin fell to its February low.

There is a chance for a positive reaction at $62K, but any rebound would be a relief rather than a recovery.

A breakdown below $60,000 would open the way to a real capitulation.

Final summary

- The drop in hashrate is part of the cycle, and Bitcoin’s pullback hasn’t been much different than previous years.

- There is a chance of a price increase from $62,000, but a recovery is not yet in sight.