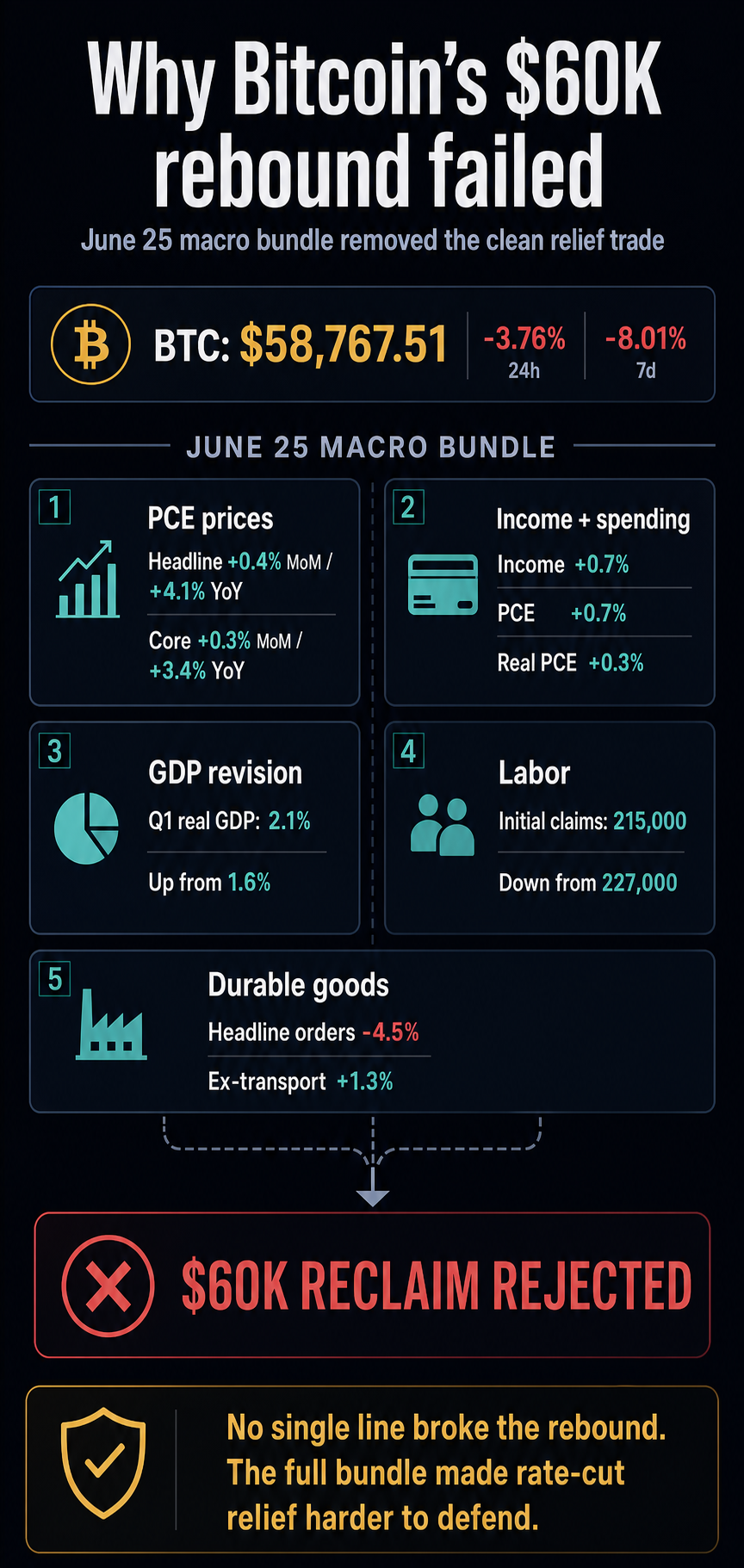

Bitcoin’s recovery above $60,000 failed simply because the bundle of US macro data released on June 25 gave risk traders the opposite of clean relief: strong inflation, robust demand, a stronger growth revision, lower unemployment claims and resilient ex-transportation orders.

Bitcoin briefly crashed in a liquidation-induced flush, falling from an intraday high of nearly $61,844 to a low of around $58,189 before recovering some of the move to trade around $59,630. The recovery sees BTC move off intraday lows as of this writing, but the price remains below the pre-decline range.

The move coincided with a very one-sided liquidation. MintGlass Liquidation readings showed about $482 million in crypto liquidations in a one-hour time frame, with about $427 million coming from longs and only about $54 million from shorts, while BTC accounted for about $272 million of the total.

The stock move was also sharp, but partially recovered. SPY fell from the high $730 to the $728 to $730 area before returning to $737 during the last 30-minute candle. That candle showed an open at $735, a high at $737, a low at $734, and a close at $737, while the chart label still showed a SPY decline of about 1.30%.

DXY returned lower after rising towards the 101.8 area and fell back to 101.376 at the last print. The US 10-year yield also fell hard, moving from the upper 4.4% range to around 4.374%, leaving yields near the bottom of the range shown after the flash move.

This move kept Bitcoin closer to the $58,000 area than a recovered upside margin, turning $60,000 from a recovery target to the level buyers had yet to prove.

The rejection was more than just another card-level failure. The release came after Bitcoin had already fallen below $60,000, subsequently denying traders the soft-data story that could have helped the risk asset recover.

The June 25 releases showed continued price pressure, strong incomes and spending, a firmer growth revision, lower unemployment claims and an orders report whose weak headline was mitigated by a stronger ex-transport value.

The data undermined the aid trade

The most direct pressure came from the May personal income and expenses be disclosed. BEA said personal income rose 0.7%, disposable personal income rose 0.7%, PCE rose 0.7% and real PCE rose 0.3%.

Prices also remained high. The overall PCE price index rose 0.4% month-over-month and 4.1% year-over-year, while the core PCE rose 0.3% month-over-month and 3.4% year-over-year.

That combination gave the market a difficult mix. Spending and revenues were still rising, while inflation had not cooled enough to make it easier to price rapid policy easing.

For Bitcoin, this meant the recovery was battling the same macro headwinds that often hit long-dated, high-beta assets first.

The growth data reinforced that message. BEAs third estimate for first quarter GDP real growth revised from the second estimate of 1.6% to 2.1% annually.

A stronger growth revision combined with persistent inflation generally makes immediate rate cuts more difficult to price.

Labor data added another piece. That of the Labor Department weekly damage report showed initial unemployment claims of 215,000 for the week ending June 20, down from the previous week’s revised 227,000.

Lower claims kept the labor market slowdown argument from fueling the rebound in risky assets.

Durable goods were more mixed, but the details still leaned toward an easy lenient interpretation. The Census Bureau advance durable goods report showed orders fell 4.5% in May as transportation equipment caused the decline.

Orders excluding transport rose 1.3%, making the underlying signal more resilient than the overall decline suggested.

| Data point | Last lecture | Why it put pressure on risky assets |

|---|---|---|

| May PCE Awards | Title +0.4% monthly, +4.1% annually; core +0.3% monthly, +3.4% annually | Inflation remained too persistent for clean aid trade |

| Income and expenses | Personal income +0.7%; PCE +0.7%; real PCE +0.3% | Demand seemed robust rather than clearly slowing |

| Real GDP in the first quarter | Revised to +2.1% YoY from +1.6% | Growth appeared stronger than the previous estimate |

| Jobless claims and durable goods | The number of claims fell to 215,000; Orders for durable goods excluding transport increased by 1.3% | Details about labor and orders limited the delay argument |

Bitcoin became the high-beta expression

The market reaction required a smaller catalyst than a uniform downside surprise would have done. The full bundle only had to weaken the idea that the US data had softened enough to drag down policy expectations.

That’s why the failed recovery of nearly $60,000 was different than a standalone support test. Bitcoin was already vulnerable after the last decline, and the macro release came at a time when buyers needed a reason to defend the recovery.

The data pointed to an economy that still had sufficient demand and labor to keep inflationary pressures relevant.

CryptoSlate’s Bitcoin data showed how far the asset had already moved. BTC’s 8.01% seven-day drop and $48 billion in 24-hour volume indicated heavy trading around the break.

The $60,000 level had become both a test of confidence and a round number.

The market also entered the release with other crypto-specific stress points already in sight. Recent CryptoSlate coverage had charted liquidation risk near the $57,300 area, ETF flow pressure around the $58,000 zone, and the possibility that Bitcoin’s PCE response could collide with quarterly options expirations.

These factors can amplify a move once the price starts to fall, while the macroeconomic release was the broader reason why the recovery lost support.

Bitcoin’s next attempt to hit $60,000 now appears to be tied to broader liquidity conditions and not just crypto-native dip buying.

If risky assets stabilize after absorbing the June 25 releases, BTC could treat the data shock as another failed downside push and attempt to rebuild above the recovery line.

On that path, the market should stop treating strong activity data and persistent inflation as a new reason to put pressure on high-beta assets.

If the dollar and interest rate-sensitive parts of the market continue to weigh on risk, the $58,000 area remains vulnerable. That would keep liquidation zone pressure and ETF flow relevant as accelerators, especially if option expiration is close enough to impact positioning.

The next signal is bigger than crypto native dip buying. Bitcoin needs the macroeconomic backdrop to stop fighting the recovery before buyers can turn $60,000 back into support.