Bitcoin traders have identified Michael Saylor as a new suspect in the latest sell-off, while the numbers tell a different story.

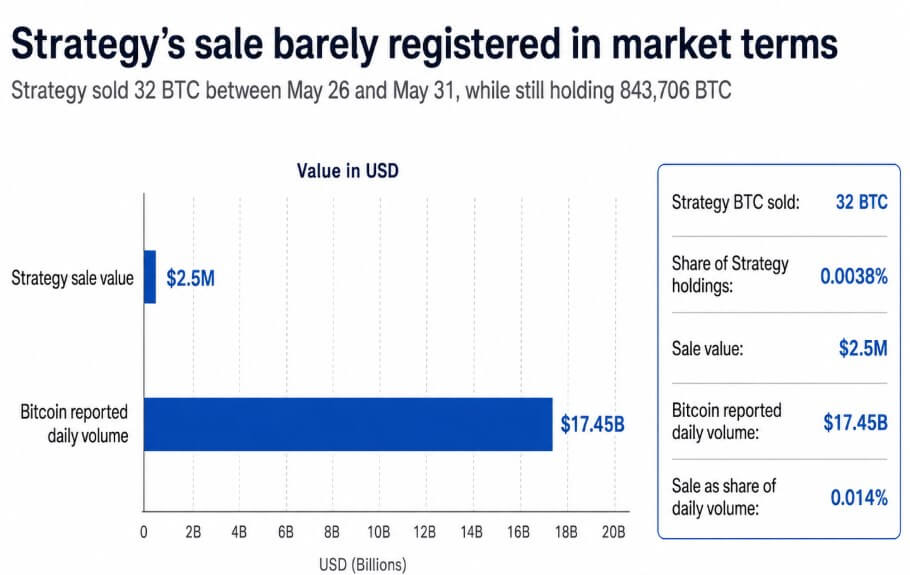

The strategy revealed in a June 1 Form 8-K that it sold just 32 BTC for $2.5 million between May 26 and 31, at an average net price of $77,135, with the proceeds going to finance preferred stock distributions.

The company still owned 843,706 BTC as of May 31, with those sales representing 0.0038% of Strategy’s total holdings and approximately 0.014% of Bitcoin’s reported daily volume of $17.45 billion on that day.

A sale of that size carries no supply-side weight against a $17 billion daily market, and ends up as a narrative event that breaks a narrative that traders had built their trust on.

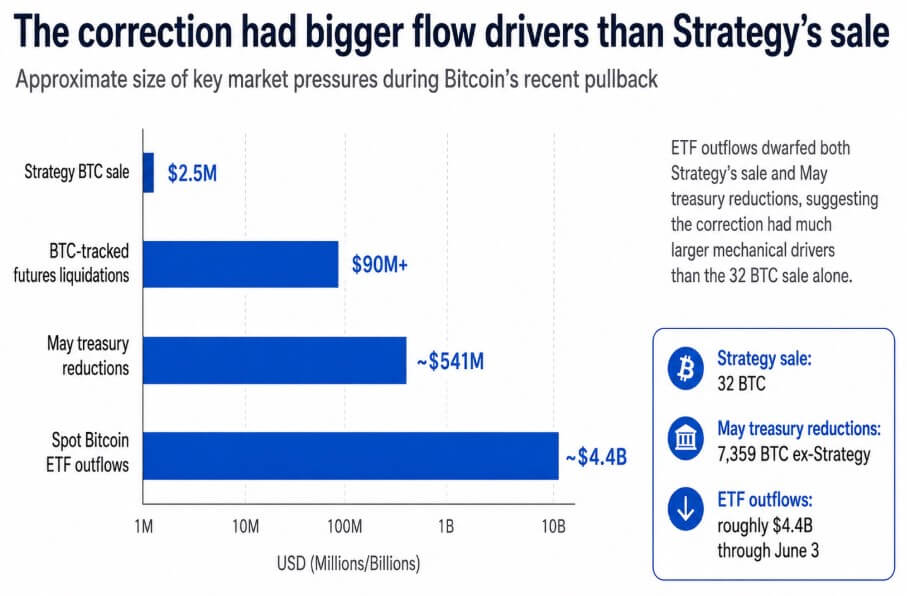

Bitcoin fell below $71,500 after the revelation, a drop also attributed to Iran-related geopolitical tensions and more than $90 million in BTC-tracked futures liquidations, making Strategy’s sale one of many.

The bigger sellers hide in May

Four other companies were responsible for the bulk of Bitcoin’s Treasury cuts in May, dwarfing their combined total sales of Strategy.

According to BitcoinTreasuries it is The Bitcoin reductions at listed companies have added up approximately 7,500 BTC during the month, with Strategy’s 32 BTC included in the following month’s count due to the submission date of June 1.

Exclusive Strategy dropped MARA 3,386 BTC, Core Scientific dropped 1,990 BTC, Sequans lost 1,481 BTC and Prenetics left 502 BTC, a combined 7,359 BTC.

At Bitcoin’s May 31 price of $73,579, that cut had a notional value of about $541 million, about 230 times the size of Strategy’s sale.

| Company | BTC reduction | About. value at $73,579 BTC | Context |

|---|---|---|---|

| MARA | 3,386 BTC | ~$249 million | Linked to banknote buyback activity in March |

| Core Scientific | 1,990 BTC | ~$146 million | Reservations on retroactive methodology |

| Sequins | 1,481 BTC | ~$109 million | Debt service/treasury strategy settles down |

| Prenetics | 502 Bitcoin | ~$37 million | Complete exit from BTC’s treasury position |

| Total | 7,359 BTC | ~$541 million | No coordinated May dump |

BitcoinTreasuries noted that the May summary used a methodology that included retroactive data and specifically flagged Core Scientific’s 1,990 BTC reduction as a reduction that would not have appeared under the previous methodology.

MARA’s larger decline also traced back to a March disclosure, when the company sold 15,133 BTC between March 4 and March 25 to finance $1 billion in convertible bond buybacks, and not a new decision from May.

Sequans was winding down a failed Bitcoin treasury strategy to pay down debt, and Prenetics had already authorized a full exit from Bitcoin to redirect capital to its IM8 health business.

Each cut had its own logic and timeline, and none reflected the shared judgment that May was a good time to sell.

BitcoinTreasuries’ net picture makes the dump thesis harder to sustain, as public Bitcoin treasuries companies added or disclosed 51,000 BTC before the May cuts and 43,500 BTC net after the cuts.

Why Saylor’s sale turned out differently

The market’s disproportionate reaction to 32 BTC reflects Strategy’s position as the symbol of Bitcoin corporate sustainability.

Since 2020, Michael Saylor has built that reputation into the company’s identity as an accumulator that never hands out and views every dip as a buying opportunity. That positioning attracted a class of investors who used Strategy as a benchmark for the belief that companies would become structural Bitcoin buyers.

A single sale to meet a preference share distribution obligation left the accumulation thesis mechanically intact, but introduced a variable that Strategy has ongoing financial obligations, and Bitcoin is the only asset available to meet them.

The ensuing fear is rational, even if the immediate reaction was exaggerated, as Strategy involves debt and preferred stock obligations with fixed distributions.

If Bitcoin prices fall further, the gap between these liabilities and the company’s ability to finance them through equity issuance or operating cash will narrow.

The sale of 32 BTC confirmed that the option to sell exists and that management will exercise it under sufficient financial stress.

Traders who built positions based on a permanent buyer now have to price in an occasional seller, and a repricing doesn’t require a big sell.

The actual anatomy of the correction

Attributing Bitcoin’s weekly decline of more than 12% solely to government bond sales misinterprets the flow data.

US-traded spot Bitcoin ETFs saw approximately $4.4 billion in outflows over the past 13 recorded trading days through June 3.

These outflows dwarf Strategy’s $2.5 million sale and May’s combined $541 million bond cuts by an order of magnitude.

Geopolitical tensions over Iran added a distinct layer of risk, and futures liquidations worth more than $90 million reinforced the directional move already underway.

The unveiling of Strategy arrived in that environment as a narrative accelerator; traders looking for a reason to reduce exposure found one, and the symbolic weight of Saylor’s sales kept the move a headline.

Geoffrey Kendrick of Standard Chartered retained one $100,000 by the end of 2026 Bitcoin target after the decline, where the decline is considered a positioning reset.

This framework will remain in place as long as the ETF outflow cycle reverses and net accumulation of the government bond sector continues, giving way if holders of Strategy or other indebted government bonds face persistent stresses that require large-scale liquidation.

What the treasury model must now prove

If the market realizes that small tactical sales can fund liabilities without ending the accumulation thesis, Strategy’s June 1 unveiling will become a footnote for the board.

The net accumulation of 43,500 BTC in May, continued ETF inflows once the current outflow cycle is exhausted, and Standard Chartered’s unchanged price target all support this reading.

Bitcoin stabilizes, Strategy’s premium to intrinsic value recovers, and the sale of 32 BTC is recorded on the balance sheet.

If investors instead revalue the treasury model and decide that debt and preferred bond companies are conditional buyers, May becomes a template for repeat principal risk.

Every quarterly filing season, every preferred distribution date, every convertible bond maturity date creates a window for another small sale to land with outsized leverage.

The price correction resulting from this repricing would come from the erosion of the premium investors allocated to Strategy’s continued accumulation.

Corporate Bitcoin treasuries based their market value in part on the promise of one-way purchases, and the sale of 32 BTC raised the question of how many times a permanent buyer can sell before the market no longer considers it permanent.