Bitcoin’s biggest buyers are no longer acting as a reliable safety net for the largest cryptocurrency.

The exchange-traded funds, state-owned government bonds and Bitcoin-linked stocks that helped define the market’s institutional era are showing signs of strain just as the world’s largest digital asset struggles to stay above $60,000, one of the most closely watched price levels.

This ongoing decline has led to a broader reevaluation of the cryptocurrency’s role in institutional portfolios, raising questions about whether the current environment reflects temporary profit-taking or a structural withdrawal from digital assets.

Demand for Bitcoin ETFs Turns into Headwinds

The clearest turnaround has come from US spot Bitcoin ETFs, which have become one of the key drivers of market demand in 2026.

For much of the period following their debut in January 2024, the funds were treated as evidence that traditional financial investors were steadily adopting Bitcoin.

Their inflows helped create a simple bull market thesis showing that access to Wall Street would bring more capital into a steady supply, making Bitcoin a sustainable source of upside.

However, that statement has been severely tested in recent weeks.

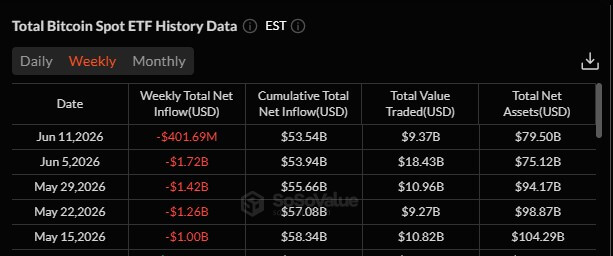

Facts from SoSoValue shows that US spot Bitcoin ETFs have recorded a five-week outflow streak totaling more than $5 billion.

This is further confirmed by Glassnode factsshowing that the 30-day moving average of net ETF flows has fallen to -2,450 BTC per day, the fastest sustained rate of outflows since the products launched.

The size of that flow is significant because it exceeds the network’s daily supply of newly created Bitcoin.

After the 2024 halving, miners will produce approximately 450 BTC per day. Sustained ETF outflows of 2,450 BTC per day are more than five times the new supply, turning what was once a source of absorption into a source of pressure.

Short bursts of ETF selling are not uncommon in volatile markets. A negative 30-day moving average carries more weight because it smooths out the daily noise and captures broader changes in positioning. Until this trend improves, institutional flows are less likely to provide support for Bitcoin prices.

Moreover, trading in the ETFs has also cooled down. The 30-day moving average of daily volume in U.S. spot Bitcoin ETFs has fallen to about $960 million from $4.4 billion in October, a decline of 78%, Glassnode reported.

This decline indicates more than just profit-taking. It shows that speculative demand from traditional market participants has declined, even as repayments have accelerated.

Lower volume can make price movements more difficult to absorb because there are fewer buyers available when selling intensifies.

BTC DATs are losing momentum

The ETF’s reversal coincided with a slowdown in another major source of Bitcoin demand: digital asset treasury companies.

These companies, often publicly traded, raise capital or use balance sheet assets to accumulate Bitcoin as a treasury. Their rise helped expand institutional adoption beyond ETFs, giving investors another way to express demand for Bitcoin through the stock markets.

Like the ETFs, their buying has faded in June.

Glassnode Analysts noted that while these companies remain net buyers overall, their daily accumulation has slowed to a fraction of the pace seen earlier this quarter.

According to them:

“Corporate bond accumulation has slowed sharply, with net inflows falling from highs above $500 million per day to near-zero levels since June.”

This slower buying removes one of the market’s clearest sources of incremental demand, at a time when ETF flows are also negative.

Some of the concerns center on Strategy, Bitcoin’s largest public company holder. The company announced that it sold 32 BTC in the last week of May, a small amount relative to its total holdings but a symbolically important move given its role in popularizing the Bitcoin treasury model for businesses.

Strategy later returned to the market during the sell-off and purchased approximately $100 million worth of Bitcoin. However, the purchase could not prevent the price from falling below $60,000.

Other BTC-focused companies have also attracted attention. Fold and Nakamoto have sold some of their Bitcoin holdings, adding to concerns that Treasury trading is becoming less one-way than it seemed during the rally.

While these sales do not represent a broad withdrawal by corporate buyers, they show that some government bonds are becoming more selective, more liquidity-conscious and more willing to adjust their positions as market conditions deteriorate.

This shift is important because the corporate treasury model is partly dependent on trust. When stock prices are strong and investor demand is high, companies can raise capital, buy Bitcoin and benefit from the perception that they are providing leverage for the asset.

However, when Bitcoin falls and demand for shares weakens, the model becomes harder to sustain.

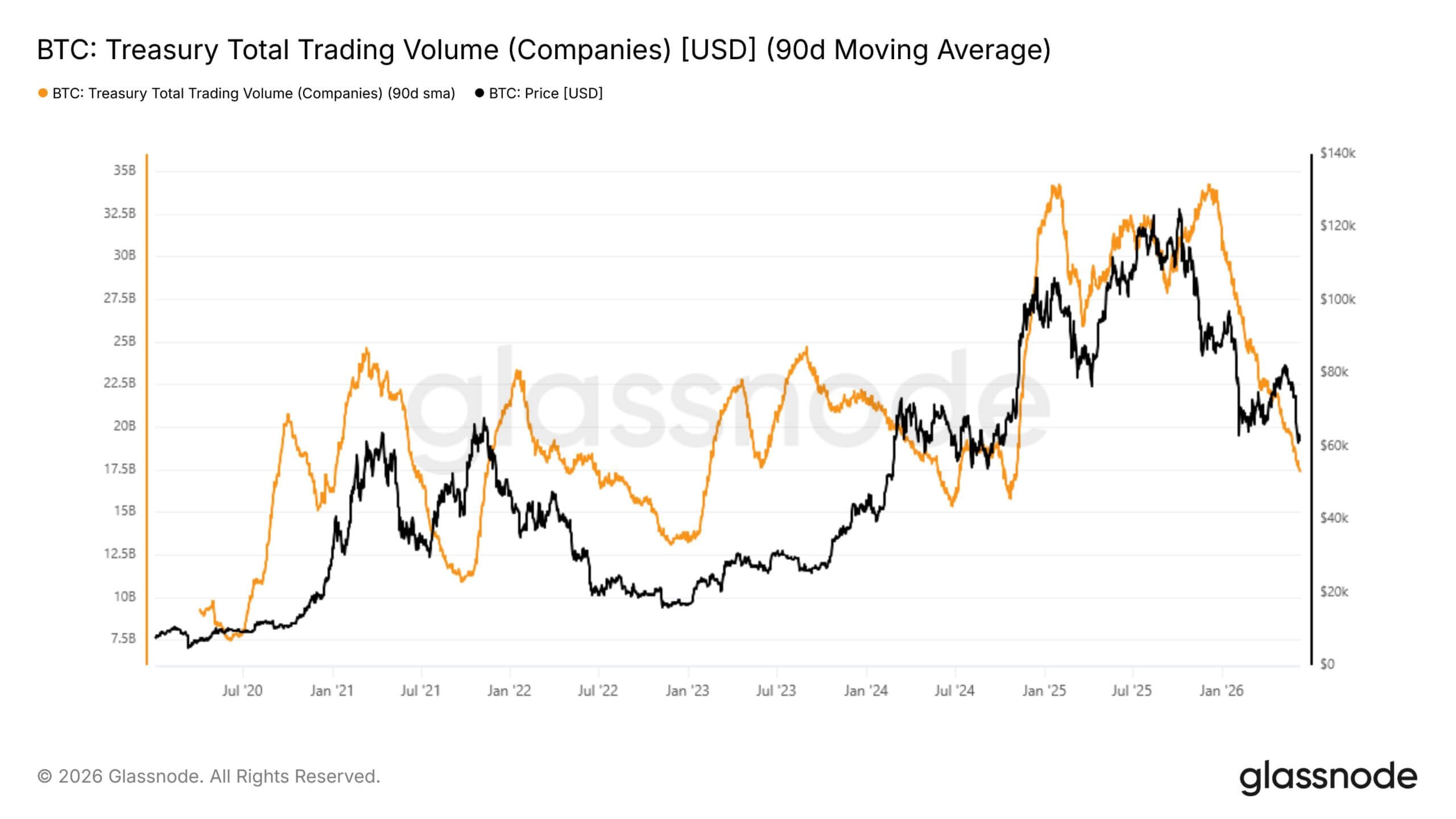

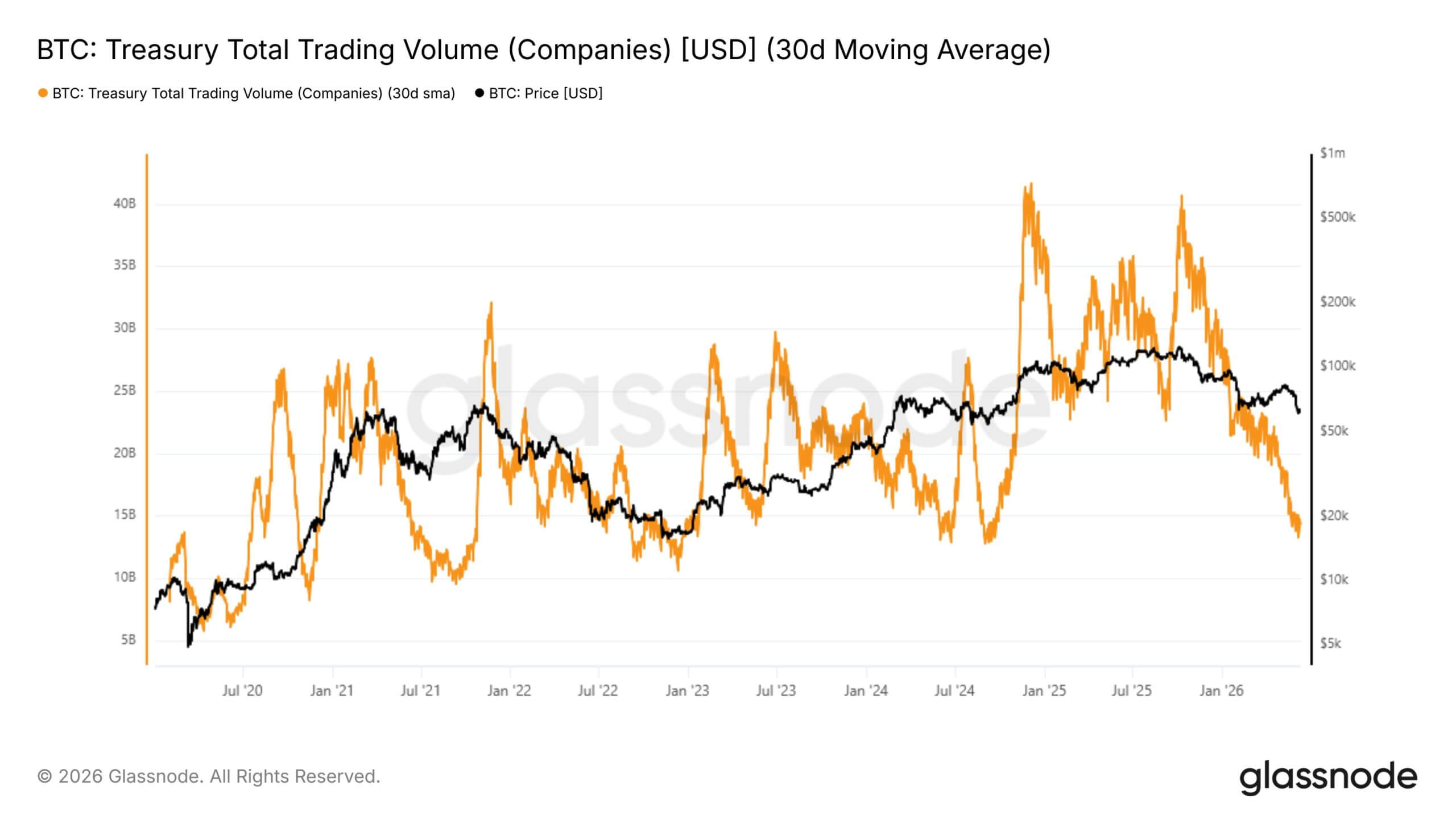

Meanwhile, this slowdown is also clearly visible in the trading activity in the shares of these companies.

Showing Glassnode data that total daily trading volume for large publicly traded Bitcoin holdings, as measured by the 30-day simple moving average, has fallen 49% in recent years about six months. Their volume fell from $34.2 billion in December to $17.4 billion at the time of writing.

That decline signals that investors are withdrawing from the broader sector Bitcoin proxy tradingnot just of the asset itself.

During stronger market periods, public Bitcoin holders often attract investors looking for leverage exposure. Their shares could rise faster than Bitcoin if sentiment improves, as they combine government bonds, operations and capital market opportunities.

That made them popular vehicles for traders who wanted exposure to crypto in the stock market without directly owning tokens. But as Bitcoin corrected, that demand has weakened significantly.

The inflow of foreign exchange signals widespread concern in the market

The institutional division has created a climate of widespread market unease, impacting participants across the wealth spectrum.

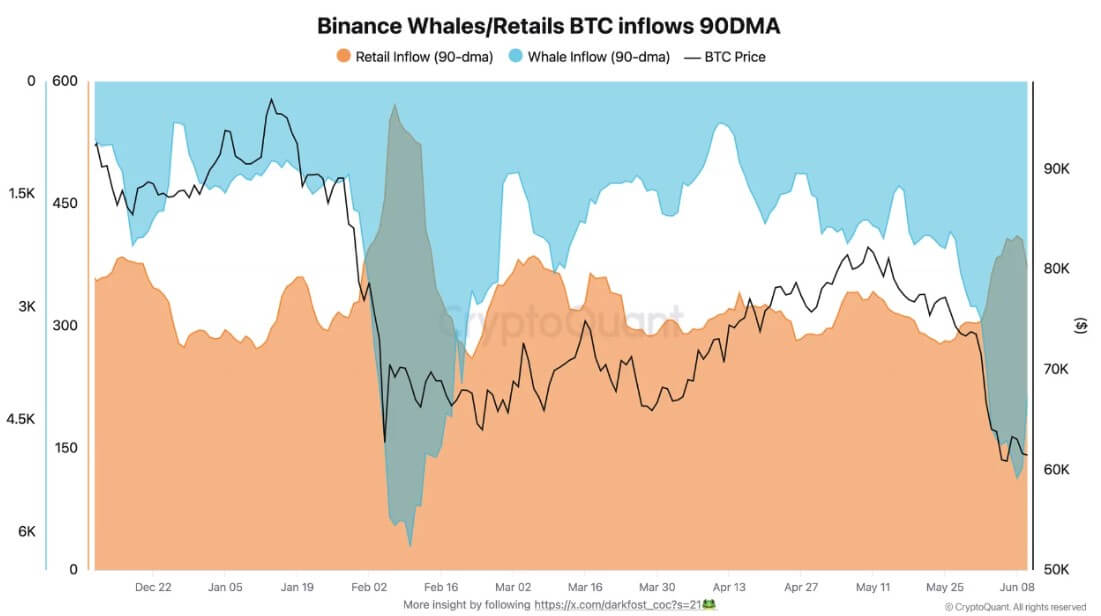

Facts of CryptoQuant indicates a significant increase in deposits from both large-scale holders and retail investors. Such deposits are usually accompanied by an intention to sell.

When Bitcoin briefly breached the $60,000 mark, large holders, or “whales,” accelerated their movement of assets onto trading platforms.

Over the past three months, whale inflows to the Binance exchange have averaged 5,280 BTC per day, a sharp increase from the daily average of 1,900 BTC observed in March. Retail investors have reflected this change in behavior, with their average daily currency inflows increasing to 410 BTC.

This parallel movement highlights how macroeconomic uncertainty is leveling the playing field in investor psychology.

The current environment marks the second major episode of increased deposits this year. A similar pattern emerged in early February, when Bitcoin tested the $60,000 threshold, with whale inflows reaching 6,200 BTC and retail inflows reaching 570 BTC.

Such periods of heightened market tension historically facilitate the transfer of assets from short-term speculators to long-term holders, although the immediate effect is significant downward price pressure.

A thinner market awaits a catalyst

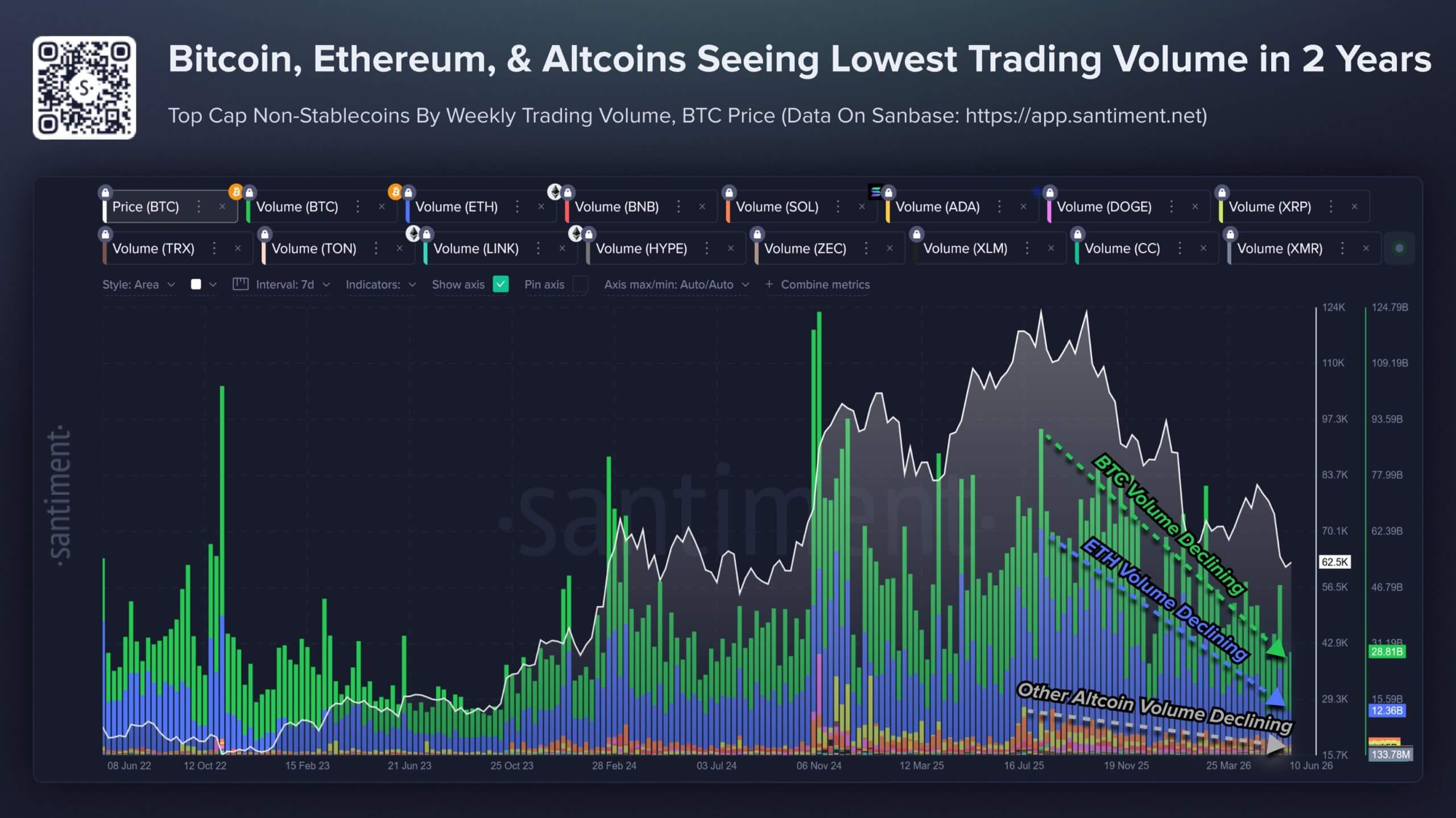

This mainstream market has arrived as broader crypto trading activity has also cooled.

Data from Santiment shows that trading volume of the largest non-stablecoin crypto assets has fallen to levels last seen in mid-2024. The decline reflects a market in which many traders appear unwilling to push prices higher or sell aggressively amid recent liquidations, macro uncertainty and geopolitical risks.

For Bitcoin, this creates a two-sided setup.

On the one hand, a small volume can make the market vulnerable. When participation is low and large buyers are less active, even modest sales can have an outsized effect on price. A negative ETF flow trend, slower government bond accumulation, and weaker demand for proxy stocks may therefore outweigh the gains in a stronger liquidity environment.

On the other hand, low volume can also indicate exhaustion. Some of crypto’s stronger rebounds followed periods of weak trading activity, attention, and conviction. Markets often recover when positioning has already been lowered and sidelined capital begins to return.

That possibility keeps the current setup from being a simple bear market call. Bitcoin still has institutional holders, buyers of publicly traded companies, and long-term investors. Development in the broader digital asset sector has not stopped and the ETF market remains an established bridge between Bitcoin and traditional finance.

But the direct question is more limited. Bitcoin doesn’t need institutions that will let it down to be squeezed. All it takes is for the biggest buyers to slow down, sell selectively or stop absorbing supply at the same pace.

That’s what the market is facing now.

Until ETF flows stabilize, demand for government bonds recovers, or trading activity returns to Bitcoin-linked stocks, the market may remain exposed to a more difficult reality: the institutional bid is still there, but it is no longer strong enough to sustain trading on its own.