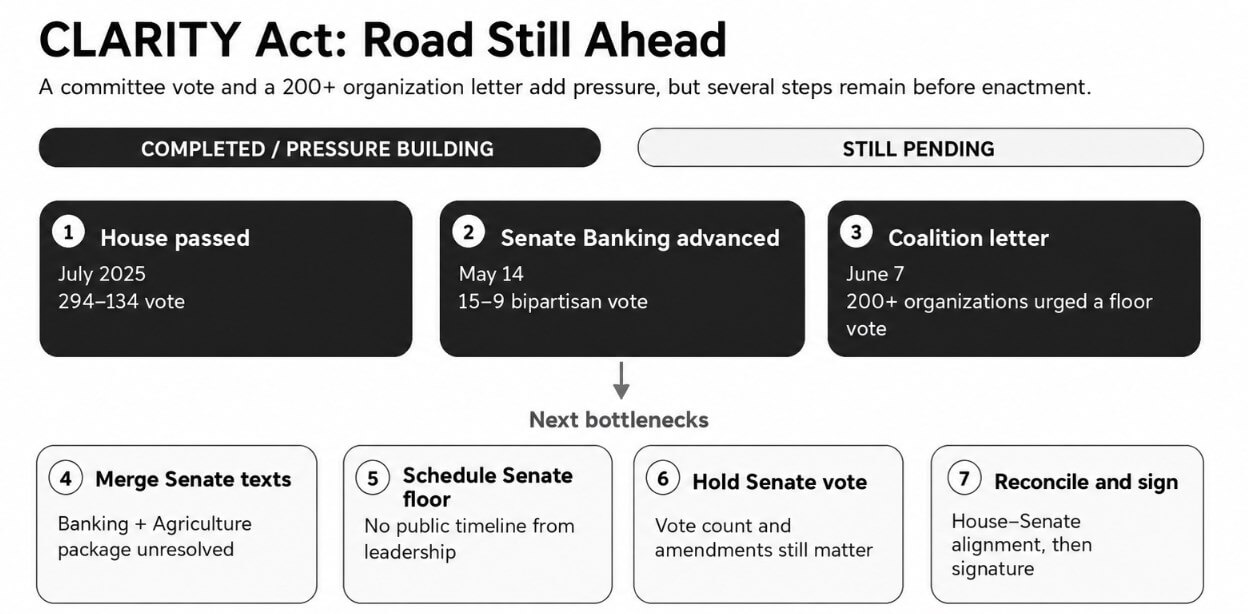

A coalition of more than 200 businesses and organizations sent a letter to Senate Majority Leader John Thune and Senate Minority Leader Charles Schumer on June 7, urging them to bring the CLARITY Act to the full Senate for a vote without delay.

Signed by Stand With Crypto, the Blockchain Association, the Crypto Council for Innovation and The Digital Chamber, the letter describes the bill as a competitiveness imperative, arguing that without a federal framework, digital asset activity will continue to move to offshore jurisdictions with weaker consumer protections and less transparency.

The move comes about three weeks after the Senate Banking Committee advanced the CLARITY Act on a 15-9 vote on May 14. The bill is now awaiting final scheduling, but Senate leadership has not publicly committed to a timeline.

According to Davis Wright Tremaine’s analysis, the Senate Banking Committee’s replacement text must still be aligned with the Senate Agriculture Committee’s Digital Commodity Intermediaries Act before the Senate fully considers this bill, and any version the Senate passes would then have to be aligned with the House-passed CLARITY Act.

Senate GOP allies are amplifying the urgency

Senator Cynthia Lummis, one of the bill’s most vocal proponents, posted on June 7 that CLARITY “passed out of committee” and that “the floor is next,” adding that supporters did not travel so far “to stop at the 5-yard line.”

Senate Banking Chairman Tim Scott followed suit on June 8, saying CLARITY would “sit with everyday Americans” and bring digital assets into a “safer, fairer and more transparent” system.

As chairman of the committee whose panel produced the bipartisan 15-9 vote that advanced the bill to this stage, Scott’s involvement goes beyond standard advocacy.

The Crypto Council for Innovation and Hedera both posted on June 8 that they had joined the coalition letter and reiterated calls for Senate leadership to schedule consideration “as soon as possible.”

The coalition letter’s momentum culminates in another letter, sent June 4 and signed by the National Consumers League, Americans for Financial Reform, Consumer Federation of America, Public Citizen and other advocacy groups, calling on Thune and Schumer to oppose the Senate version.

The letter cites three concerns: the weak Bank Secrecy Act and anti-money laundering requirements, insufficient ethics provisions, and a loophole regarding stable coin returns.

These objections target precisely the provisions that Democratic vote counters and some moderate Republicans flagged as requests for review before the floor vote can be considered, and they explain why a large coalition on one side has not set a date for the floor vote.

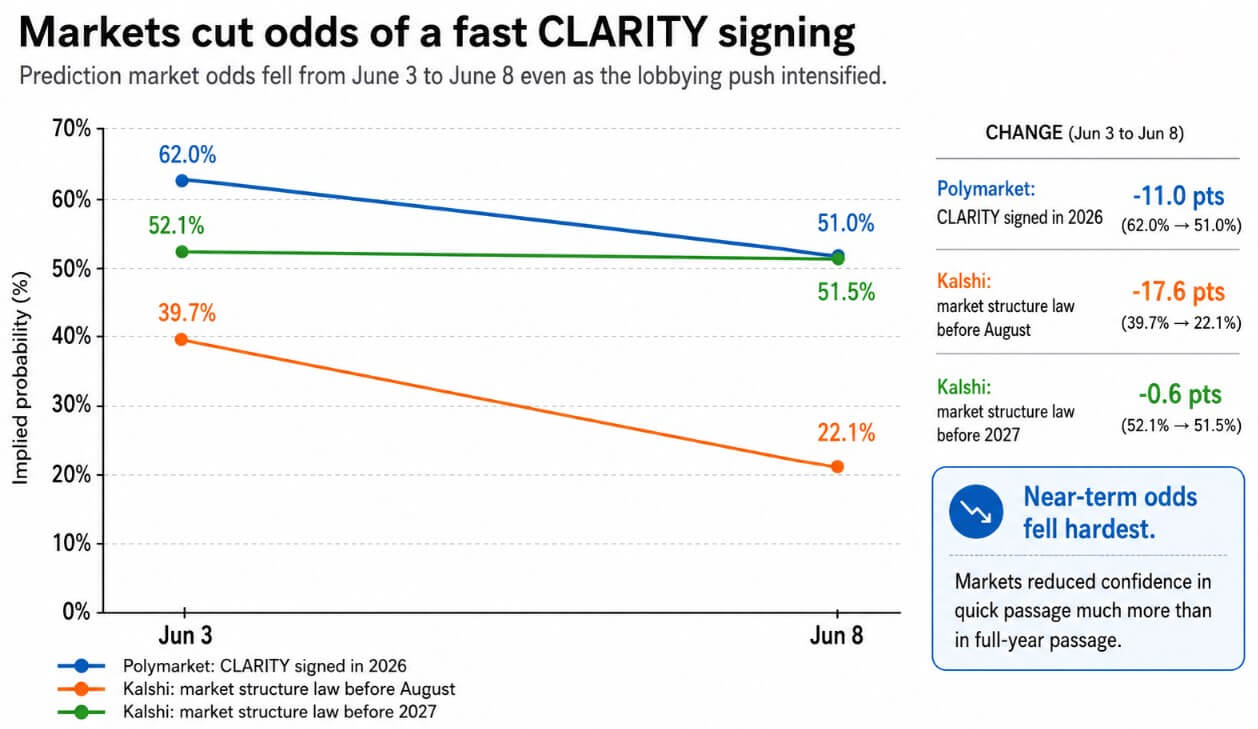

Markets prize the discrepancy between noise and results

Polymarket’s contract on whether CLARITY will be signed into law in 2026 was at 62% on June 3, dropping to 51% on June 8.

The probability implied by Kalshi’s market that a law on the structure of the crypto market will be passed before August fell from 39.7% to 22.1% over the same period. Kalshi’s contract on whether such a law would be passed before 2027 rose only marginally, from 52.1% to 51.5%, indicating that traders see an outside opportunity to make the law take effect for the entire year but have sharply lowered their assessment of a quick signing.

Third-party forecasters have moved in the same direction, with Galaxy Digital’s Alex Thorn reportedly cutting his 2026 CLARITY passage estimate from 75% to 60% based on Senate calendar risk, while JPMorgan cut its own estimate below 50%.

Predictive market traders have retreated even as institutional investors reached their loudest point since the commission’s approval.

Those markets are touting three concrete sticking points: whether Senate leadership can find floor time, whether the ethics and AML disputes can be resolved without reopening larger fights, and whether the calendar survives competition from budget reconciliation, national security legislation and other election-year priorities.

What the bull and bear cases actually cost

In a bull case, Senate leadership will find the time in July and revise language on ethics and illicit finance enough to keep the bipartisan coalition together without sparking a new wave of defections.

Under that outcome, Polymarket could reprice to 70% to 80%, Kalshi’s pre-August market could recover to 40% to 55%, and institutions exposed to currency regulation, token issuance, and tokenized asset markets could see the policy discount in their valuations shrink.

| Scenario | Legislative trigger | Forecasting market repricings | Market impact |

|---|---|---|---|

| Taurus case | Senate leadership will find floor time in July; ethics and illegal financial language have been revised enough to maintain bipartisan support | Poly market moves towards 70%-80%; Kalshi before August recovers towards 40%-55% | Policy discount compressions for exchanges, token issuers, tokenization companies; Bitcoin receives secondary support from improved institutional risk appetite |

| Bear case | No floor time before recess; The Senate calendar is filling up with higher priority legislation; Disputes over AML, ethics and language for stablecoin generation remain unresolved | Poly market drifts towards 25%-40%; Full year kalshi market falls below 35% | Crypto markets are refocusing on ETF flows, macro liquidity and Bitcoin’s technical reach; The case for offshore migration is getting stronger |

Bitcoin would see a secondary bid due to improved institutional risk appetite and normalization of ETF flows, after 13 consecutive sessions that pulled $4.4 billion in flows from US-traded spot Bitcoin ETFs.

In the bear case scenario, there will be no speaking time before the recess, the Senate calendar will be filled with higher priority legislation, and the coalition letter will become the latest in a series of well-organized but ultimately ineffective pressure campaigns.

In that scenario, Polymarket drifts toward 25% to 40%, Kalshi’s annual market falls below 35%, and crypto markets refocus on ETF flows, macro liquidity, and Bitcoin’s technical range rather than regulatory catalysts.

That outcome would also accelerate the offshore migration argument used in the coalition letter to label CLARITY as urgent, as the EU’s MiCA transition period ends on July 1, after which crypto asset service providers without a MiCA license must stop serving EU customers.

The U.S. regulatory vacuum described in the coalition letter is already costing market share to jurisdictions that completed their frameworks first.

The June 7 coalition letter ranks as the industry’s most formally coordinated push for a CLARITY vote since bipartisan approval by the Senate Banking Committee in May.