The macro FUD is easing, markets are deleveraging, and Fed policy is changing.

According to CoinGlass data, approximately $1.8 billion in liquidations hit the broader crypto market over the past 72 hours, with more than 75% of the total outflow coming from long positions, in line with Bitcoin’s weekly decline of more than 5%.

The flush was not entirely unexpected. BTC has been consolidating around $60,000 for almost two weeks, allowing long debt exposure to accumulate.

Once the price lost that range, this move naturally led to long liquidations, leaving clearing traders positioning themselves for a bullish continuation. Against this backdrop, Ansem’s third-quarter BTC thesis is starting to make more sense.

According to the analyst, the flush did what it was supposed to do: reset the excessive leverage and shake out weak hands. With positioning much cleaner, Bitcoin could be in a better place to regain momentum, provided market demand returns.

On the macro side, the analyst argues that the backdrop is still supportive. After a four-week run on the US dollar, the rotation into gold has started to fade, while inflows into AI have left many sitting on large unrealized gains.

As macro FUD is eased, the market is increasingly leaning towards a return to risky assets.

Against this backdrop, Ansem has flipped its Bitcoin [BTC] stance from bearish to bullish, with the start of the third quarter seen as a clear, long setup. However, unrealized losses among long-term holders of BTC continue to mount, raising questions about whether the market is underestimating the downside risk.

Bitcoin Setup: Macro Tailwinds vs. LTH Stress Signals

Is it too early to call Bitcoin’s current dip a buying opportunity?

Even as macro FUD cools around the Strait of Hormuz, expectations for a Fed rate hike have risen to over 27%, up from 11% last month, ahead of the upcoming FOMC meeting on July 29. This shift adds a new layer of uncertainty to BTC’s setup, even as liquidity conditions show early signs of easing.

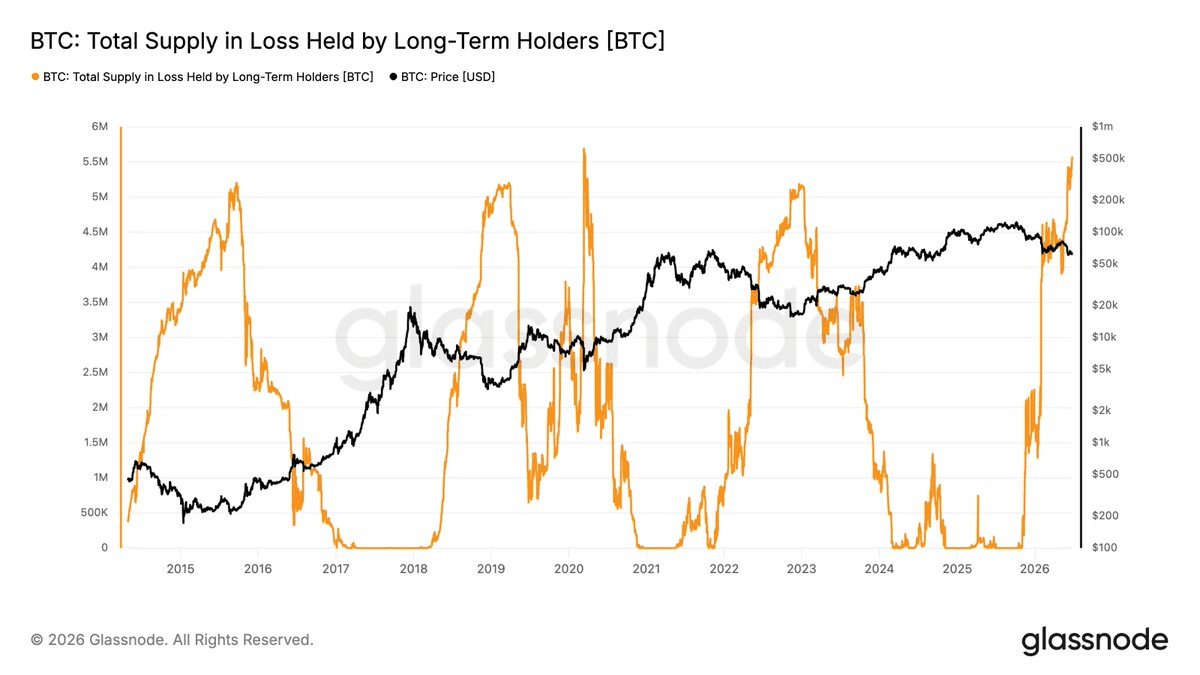

In this context, the growing number of holders with unrealized losses is becoming increasingly important. As the chart below shows, almost 11 million BTC are now in losses, which is the highest level ever.

Bitcoin’s drop to $59.1k has pushed 10.83 million BTC underwater, according to data from Glassnode. LTHs now hold 14.8 million BTC, about 75% of the circulating supply, of which about 37% is currently in the red.

Against this background, Ansem’s call may come a bit early.

Without strong catalysts coming through, that of Bitcoin mock question still looks weak. In that context, it may be premature to view the recent downturn as merely a short-term deleveraging exercise. Meanwhile, macro FUD continues to weigh on sentiment among long-term investors.

This obviously increases the risk of LTH capitulation. Overall, this makes a strong Bitcoin setup for the third quarter less convincing for now, with the market potentially underestimating the downside risk.

Final summary

- Leverage resets and macro conditions improve, allowing Bitcoin to recover when spot demand returns.

- Weak demand, Fed uncertainty and rising LTH losses increase the risk of further downside.