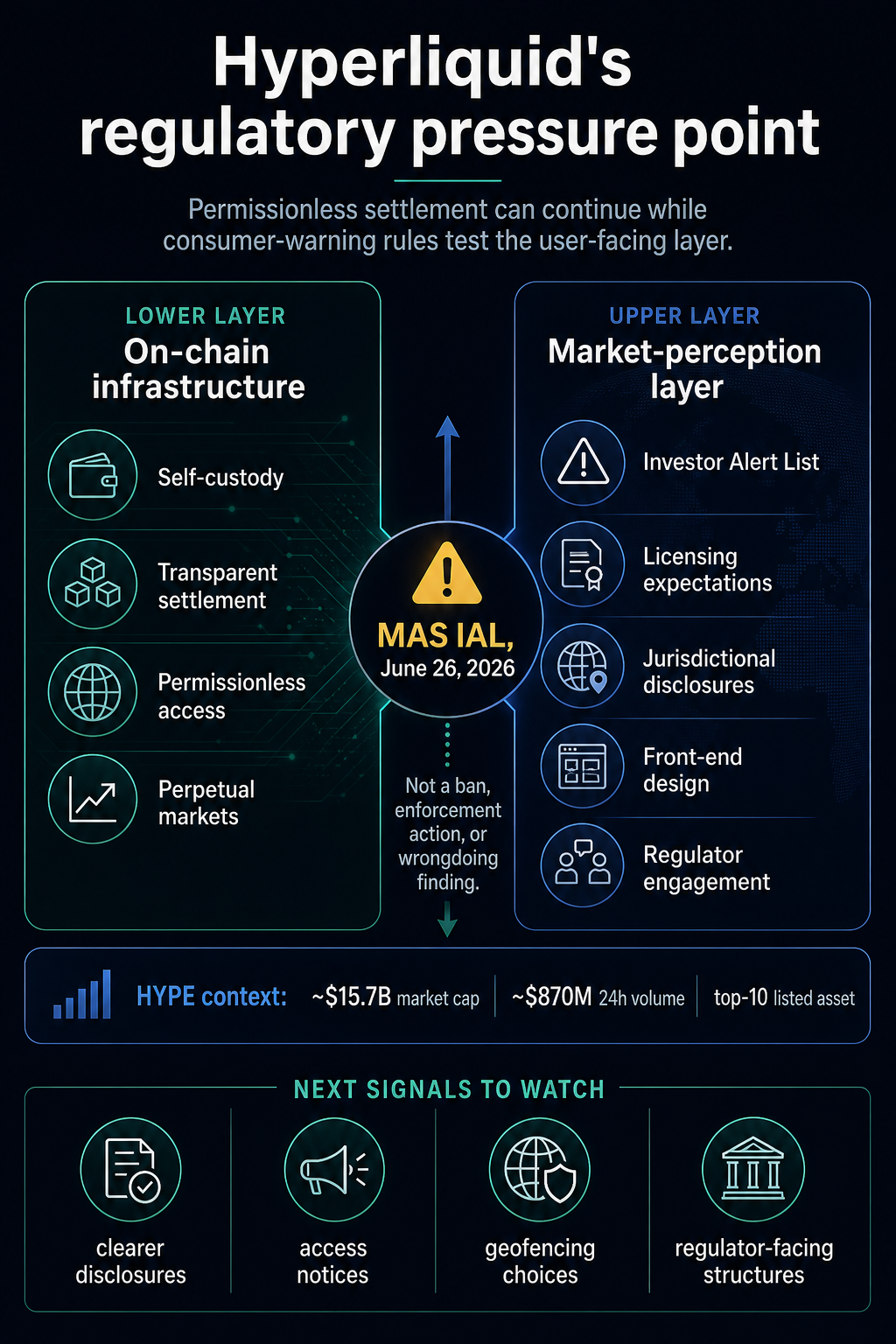

Hyperliquid has been added to Singapore’s Investor Alert List, putting DeFi’s permissionless pitch to a consumer protection test: the network can continue to transact, while the interface and public messaging around it attracts regulatory scrutiny.

Hyperliquid said in a June 26 statement that its appearance on the Monetary Authority of Singapore’s list was a warning list rather than a ban, enforcement action or finding of misconduct.

The project also said it had not claimed to be licensed by MAS, describing itself as a permissionless infrastructure, and that users maintain self-control while transactions are transacted transparently on-chain.

The resulting pressure is applied to the user-facing layer. A well-performing on-chain derivatives platform can continue to process trades and still face questions about whether its interface, documentation and public messaging lead retail users to believe they are accessing a regulated market.

Singapore’s alertness is therefore now shifting the regulatory test to consumer perception.

The warning list tests the market-oriented edge

The MAS Investor Alert List is a public warning tool. Singapore’s public materials frame the list of unregulated individuals or entities that could be misconstrued as licensed or authorized by MAS.

MoneySense, Singapore’s national financial education program, warns that consumers dealing with unregulated individuals may forego the protections available under the MAS regulations, and that the list is not exhaustive.

That consumer protection framework is separate from any finding that Hyperliquid violated Singapore law. MAS said when it launched the IAL in 2004 that publishing a name on the list did not mean the authority had concluded the person had broken the law.

Hyperliquid’s own response leans toward the same boundary. The venue’s statement said the listing does not amount to a ban or enforcement finding, while also emphasizing that users are not giving up custody of the protocol and that transactions are settled on-chain.

These points can all be true at the same time. A regulator can prevent a protocol from being banned, and the protocol can continue to function as designed, while the warning still changes the public framework around who must use it, what protections users have, and whether the interface gives the appearance of regulated access.

Hyperliquid’s documentation describes a high-quality on-chain derivatives infrastructure and broad coverage of perpetual markets. That’s central to its appeal: it gives users a comprehensive derivatives venue while routing the main settlement story through on-chain infrastructure.

The MAS list tests the part of that model that leaves the technical architecture open. A protocol can be permissionless at the settlement layer, yet most users still comply with it through a website, user interface, documentation, social posts, market pages, and third-party discussions.

These layers create expectations before a transaction ever occurs.

Singapore’s public materials focus on whether consumers believe an entity is licensed or authorized, and MoneySense highlights what users lose by trading outside the regulated perimeter. For on-chain derivatives platforms, this puts pressure on both the presentation of access and the availability of code.

The practical questions are simple. Does the interface tell users which areas of law it is aimed at? Is it stated what protection users do not have? Does this prevent or discourage access if the operator sees a clear regulatory risk? Will the venue work with regulators as its user base and market footprint grow?

Scale turns disclosure into a live test

The market context makes the warning more than a footnote for niche compliance. HYPE is currently in the top 10 assets as of June 26, with a market cap of approximately $15.7 billion, approximately $870 million in 24-hour trading volume and strong performance over 90 days.

Warnings from regulators come out differently when the subject is a large, liquid location, rather than a small experimental app. A retail user who sees a large token, visible volume, active markets, and a polished trading experience can infer a level of market acceptance that is different from local authorization.

That is the gap that Singapore’s warning framework was built to address. The framework asks whether consumers may misunderstand the status of the entity they are dealing with and whether they understand that MAS protections may not apply.

For Hyperliquid, the consequences are reputational and operational rather than technical. The network can continue to handle transactions, but the public attitude of the project may now be at a higher level.

Clearer jurisdictional disclosures, access notices and communications with regulators become more important as the size of the site makes it more difficult to argue that consumer perception is outside the operator’s responsibility.

The pressure also comes at a time when Hyperliquid’s entry model is already under discussion. A CryptoSlate article from June 24 reported that Changpeng Zhao praised Hyperliquid’s no-KYC model before noticing it The involvement of a lawyer is a practical limitation.

Earlier in June, another CryptoSlate article covered a UK alert raising concerns about unauthorized companies around Hyperliquid.

The case of Hyperliquid provides a taste of how big the derivatives platforms in the chain can be judged as they become easier to find and use for retail users.

The technical claim of permissionless infrastructure remains important. Regulators can also focus on what users are led to believe about licensing, local protections and who is behind the interface if an app starts to resemble regulated market entry.

Possible next signals

Singapore has shown this distinction before. In its 2022 statement after FTX’s collapse, MAS said Binance was not banned in Singapore, while also pointing out licensing and solicitation concerns.

That precedent concerns a different fact pattern, but it shows that MAS can separate a technical or practical access question from a licensing and warning list question.

For DeFi derivatives, that separation will likely become more important. A venue can defend self-custody and on-chain settlement while still needing a more mature response in terms of jurisdictional availability, consumer alerts, front-end design and regulator involvement.

The signals we need to look for now are changes in the way Hyperliquid and other major on-chain trading platforms engage users in specific markets. Possible responses could include clearer disclosures regarding Singapore, revised terms, access notices, geofencing decisions or direct structures dealing with regulators.

Either of these would show that the center of pressure has moved from the chain itself to the user-facing layer surrounding it.

Until then, the MAS warning leaves DeFi with a more uncomfortable message than a formal ban would have done. Unauthorized infrastructure can continue to operate, while consumer protection systems can still shape how that infrastructure is presented, understood, and trusted.