A group of Republican senators are warning U.S. banking regulators that a little-known capital rule could effectively keep banks out of Bitcoin, even as Congress moves to give traditional financial firms a bigger role in digital asset markets.

In a May 27 letter to Federal Reserve Vice Chairman for Oversight Michelle Bowman, FDIC Chairman Travis Hill, and Comptroller of the Currency Jonathan Gould, six senators urged the agencies to build a new capital framework for on-balance sheet digital asset activities.

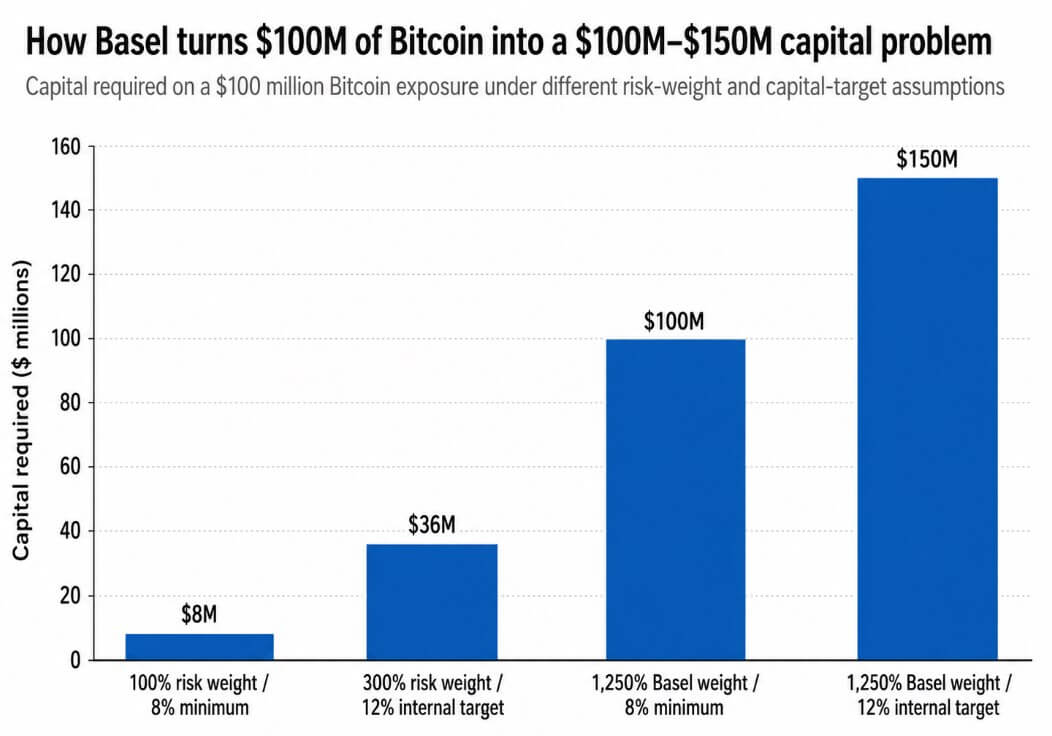

Their target is Basel’s risk weight of 1,250% for assets like Bitcoin, which they say acts as a de facto ban on banks owning crypto.

A risk weight of 1,250% multiplied by the minimum capital requirement of 8% corresponds to a capital allocation of 100%, meaning that a bank holding $100 million in Bitcoin would need at least $100 million in capital to do so.

For banks that succeed in achieving internal CET1 targets above the legal threshold, the costs will increase further. A bank with an internal capital target of 12% would need $150 million in capital for that same $100 million exposure, which would require roughly $18 million in annual net profit to overcome a 12% ROE hurdle.

Normal custody, trading, or customer service economies rarely generate returns at that threshold, leaving a bank legally entitled to hold Bitcoin but unable to financially justify it.

Why this lands now

The Senate Banking Committee advanced the CLARITY Act on a 15-9 vote on May 14, sending it to the Senate.

If passed, the bill would give banks a clearer regulatory role in digital asset markets, but senators argue that regulatory clearance without capital efficiency leaves banks with a consent slip they can’t afford to use. A bank can be legally authorized to hold Bitcoin and yet be structurally prevented from doing so by a capital requirement that makes the position uneconomic before the first transaction.

The three regulators who have the postal addresses have each moved toward crypto tolerance since the beginning of 2025.

The OCC reaffirmed in March 2025 that national banks may engage in crypto custody, stablecoin-related activities, and distributed ledger payment functions, while removing the regulator’s prior no-objection requirement.

The FDIC followed suit that same month, rescinding the reporting requirement and allowing FDIC-supervised institutions to conduct permitted crypto activities without prior approval.

The Fed withdrew its guidance on crypto assets and dollar tokens in April 2025, citing the move as support for innovation.

All three agencies opened the door to crypto activity and left the Bitcoin capital issue untouched.

The senators found their sharpest argumentative support in a March 2026 interagency FAQ on tokenized securities.

| Controller | Recent crypto-friendly move | Which allowed or relaxed it | What remains unresolved |

|---|---|---|---|

| OCC | Guidance for March 2025 | Crypto custody, stablecoin activity, DLT payments; the no-objection requirement removed | Capital treatment for Bitcoin held by banks |

| F.D.I.C | Guidance for March 2025 | Permitted crypto activities without prior approval from the FDIC | Capital treatment for direct exposure to cryptocurrencies |

| Fed | April 2025 withdrawal | Previous crypto/dollar token guidelines withdrawn | Capital treatment for Bitcoin on the balance sheet |

| Fed/FDIC/OCC | March 2026 FAQ | Tokenized securities are generally treated as underlying securities | Whether that logic applies to native cryptoassets |

The joint guidance from the Fed, FDIC and OCC opined that eligible tokenized securities should generally receive the same capital treatment as their non-tokenized equivalents, and that the technology used to record or transfer ownership should not determine capital allocation.

If a tokenized Treasury is treated as a Treasury because its underlying risk profile determines its treatment, the logic should extend to Bitcoin, and the asset’s volatility and operational risks are measurable and can support a calibrated framework.

The March 2026 guidelines cover eligible tokenized securities, and the senators urge regulators to extend the same technology-neutral logic to native digital assets.

The prudential argument for the rule

The 2023 Fed, FDIC, and OCC joint statement noted price volatility, legal uncertainty regarding custody and ownership rights, contagion from exchange and counterparty failures, weaknesses in the governance of crypto networks, and operational risks associated with open or decentralized infrastructure.

The Basel Standard was built around these risks after the 2022 cryptocurrency collapse exposed how quickly losses could spread to interconnected institutions.

A dollar-for-dollar capital requirement reflects an honest judgment that Bitcoin’s risk profile bears no resemblance to the assets that populate traditional bank balance sheets.

The senators argue that the risks of volatility, custody complexity, and operational exposure are quantifiable, and that a calibrated capital framework can address them without requiring capital equal to or greater than the exposure itself.

The Basel Committee agreed in November 2025 to expedite a targeted review of elements of its cryptoasset standard, and reported progress on that review in February 2026.

Basel Chairman Erik Thedéen has said global crypto rules for banks need to be reworked after the US and Britain both refused to implement the current framework.

A coalition of major financial industry groups wrote to Basel in August 2025, arguing that the standard would make meaningful bank participation uneconomic and calling for a pause and revisions.

The senators are urging US regulators to act at a time when the international architecture underlying the 1,250% treatment is under open review.

Two paths from here

If regulators respond by proposing a calibrated framework for liquid digital assets instead of the blanket Basel weight, the capital required for $100 million of Bitcoin exposure could drop from the current range of $100 million to $150 million to something closer to $8 million to $36 million under a 100%-300% risk weight range and standard capital targets.

| Scenario | Capital handling | Role of the bank in crypto | Probably market effect |

|---|---|---|---|

| Calibrated framework | 100%-300% risk weight range; Capital from $8 million to $36 million on $100 million exposure | Banks can hold inventories, support market making, custody, prime brokerage and structured products | More institutional liquidity; tighter spreads; banks become balance sheet participants |

| The Basel rule remains | 1,250% risk weight; Capital of $100 million to $150 million on exposure of $100 million | Banks usually provide custody, settlement and services, but avoid direct BTC exposure | Bitcoin access continues to be through ETFs, non-banks and offshore locations |

At that level, bank market making, custody, prime brokerage and structured crypto products become viable industries. Institutional liquidity is improving, spreads are narrowing and banks are shifting from service providers to balance sheet participants.

If regulators maintain a 1,250% treatment as the practical standard for native cryptocurrency exposure on the balance sheet, while continuing to open other avenues, banks would continue to offer custody and settlement, while direct exposure to Bitcoin remains with non-banks and ETF wrappers.

US-traded spot Bitcoin ETFs already saw roughly $4.4 billion in outflows between May 15 and June 3, showing that institutional access to Bitcoin has bypassed bank balance sheets.

That channel will deepen if the capital rule remains intact.

The letter raises the political costs of inaction, while Congress is actively writing the market structure rules that will govern banks’ participation in digital assets over the next decade, and regulatory permission to hold Bitcoin means little if the capital requirements required to do so make the position uneconomic from the first day it hits the balance sheet.