Ripple is pursuing a coordinated expansion of its stablecoin infrastructure in Europe and Africa, combining a strategic investment in payments company Flutterwave with preliminary regulatory approval in the European Union to expand the reach of its digital asset services.

The two-pronged strategy focuses on large-scale cross-border payment and remittance corridors in sub-Saharan Africa, while giving Ripple a potential regulatory base in the 30-nation European Economic Area.

By placing its dollar-pegged RLUSD stablecoin within Flutterwave’s regional payments network, the San Francisco-based company seeks to transcend its role as a provider of cross-border payments and liquidity technology and become part of the infrastructure that supports regulated commercial stablecoin flows.

The plan combines two assets that stablecoin issuers increasingly need to compete: permission to serve financial institutions in major markets and access to payment networks capable of generating regular transaction volume.

Ripple’s proposed license for crypto asset service providers in Luxembourg would provide the regulatory reach. Flutterwave, which processes payments for businesses across Africa, would provide local collection methods, payout channels and remittance customers.

The approach shows how competition in the stablecoin market is moving beyond just token issuance. The largest providers have built up significant liquidity on exchanges, but the next phase of growth increasingly depends on whether stablecoins can be integrated into payroll, trading, cash management and cross-border payments without requiring customers to interact with the underlying technology.

Flutterwave gives RLUSD a route to African payments

Ripple participated in Flutterwave’s Series E funding round, which valued the African payments company at $3.2 billion. The companies did not disclose the size of Ripple’s investment.

The partnership calls on Flutterwave to integrate RLUSD, Ripple Payments and the XRP Ledger (XRPL) into the infrastructure that already connects businesses to cards, bank transfers, mobile wallets and other domestic payment methods.

Flutterwave revealed plans to use RLUSD as a settlement agent within its payment network and the Send App money transfer service. It also plans to use the XRPL blockchain network to settle transactions and connect its regional infrastructure to Ripple’s international payout network through a common application programming interface.

The arrangement could allow a company to accept or send money through trusted local methods while RLUSD moves in the background among financial intermediaries. That would reduce the need for merchants and consumers to hold cryptocurrency directly.

Flutterwave said its broader stablecoin infrastructure is already commercially active and being tested within the Send App. The integration of RLUSD and Ripple’s other products represents the next phase of that buildout and is not evidence that the entire system is already processing transactions at scale.

Reece Merrick, Ripple’s managing director for the Middle East and Africa, said the investment would place RLUSD within Flutterwave’s infrastructure and direct stablecoin flows through the XRP Ledger. Ripple also plans to make its payments network available for more cross-border transactions in the region.

The companies did not provide a launch schedule, expected transaction volume or expected customer savings. They also have not identified the first payment corridors that will use RLUSD, or explained how they will manage the conversion between the stablecoin and local currencies.

These details will determine whether blockchain settlement delivers lower costs for businesses. Moving tokens through a ledger can take a few seconds, but the entire transaction can still depend on banks, currency dealers, compliance reviews, and sufficient liquidity at the point where digital dollars are converted into local money.

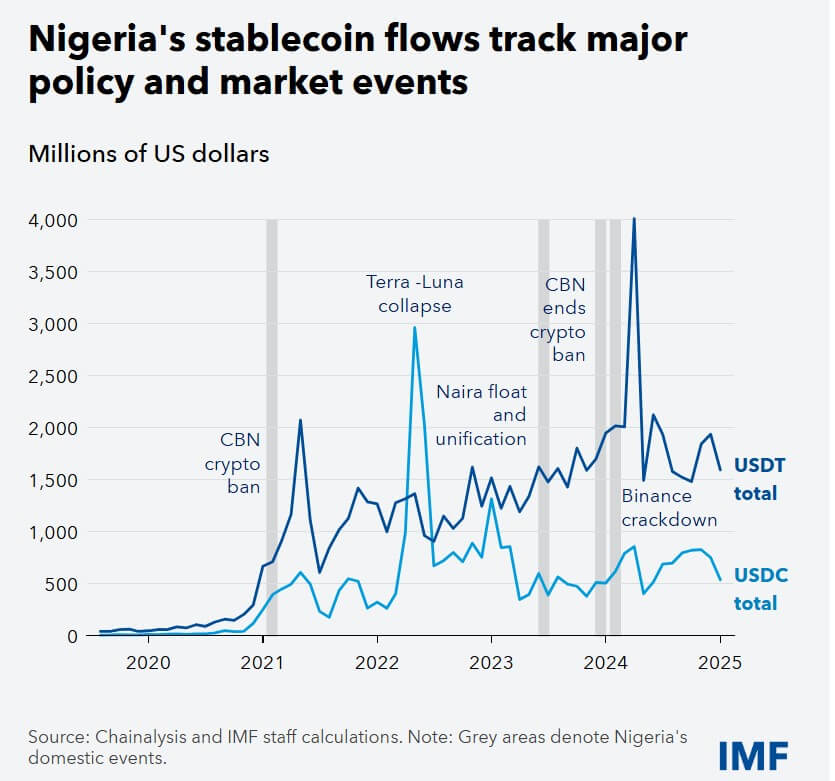

Nigeria shows the demand that Ripple is chasing

Ripple’s investment gives it a route into markets where stablecoins are already being used for purposes beyond speculation.

Nigeria received about $59 billion in crypto asset inflows between July 2023 and June 2024 and has accounted for about 60% of stablecoin inflows in sub-Saharan Africa since 2019, according to the International Monetary Fund (IMF) said.

Dollar-pegged tokens have become an alternative for households and businesses dealing with the depreciation of the naira, inflation and limited access to foreign exchange. They allow users to store value in dollars, pay foreign suppliers and receive money from abroad via smartphones and digital wallets.

Stablecoins can also compete with conventional money transfer services. Sending $200 to sub-Saharan Africa costs about 9% of the transaction on average, compared to a global average of about 6%, the IMF said, citing World Bank data.

The gap creates an opening for companies that can connect blockchain settlement to local payout networks. A stablecoin transfer can occur quickly between digital wallets, but becomes more useful for trading when recipients can reliably convert it into bank deposits or domestic currency.

That conversion layer is where Flutterwave could be valuable to Ripple. The existing relationships with banks, merchants and payment providers can give RLUSD a distribution channel that would be difficult for Ripple to build independently in every African market.

Meanwhile, this possibility also poses regulatory risks.

The IMF has warned that the widespread use of dollar stablecoins could resemble digital dollarization, reducing demand for domestic currencies and weakening the transmission of monetary policy. Transactions made through wallets and offshore platforms can also be more difficult for authorities to monitor than payments made through banks.

Ripple and Flutterwave are betting that placing stablecoin transactions within a regulated business infrastructure can alleviate some of these concerns.

Still, businesses across the continent will have to comply with different rules around foreign exchange, payments and digital assets, rather than relying on a single African regulatory framework.

Luxembourg opens the European side

Ripple’s preliminary approval in Luxembourg concerns the institutional end of the proposed network.

On June 23, the Brad Garlinghouse-led company announced that the Commission de Surveillance du Secteur Financier had issued Ripple a “Green Light Letter” for a crypto asset service provider license under the European Union’s Markets in Crypto-Assets (MiCA) regulations. The decision remains subject to final conditions and does not yet constitute full authorization.

Once completed, the license would allow Ripple to offer covered crypto services across the European Economic Area, including the 27 member states of the EU, as well as Iceland, Liechtenstein and Norway.

Ripple plans to combine the license with its existing Luxembourg electronic money institution license. The company said the two approvals would allow banks, financial technology firms and corporations to collect, exchange and distribute fiat money, stablecoins and other crypto assets through a single integration.

That combination is central to Ripple’s strategy. The electronic money license covers parts of the conventional payment system, while the MiCA authorization would govern the provision of crypto asset services.

Together, they could enable Ripple to connect European institutional clients to payment and settlement channels outside the region.

Cassie Craddock, Ripple’s managing director for the UK and Europe, said demand from banks and fintech companies is increasing as financial institutions explore blockchain-based payments, collateral management and tokenized assets.

Ripple says its payments platform has processed more than $100 billion and operates in more than 60 markets. It also says it holds more than 75 regulatory licenses worldwide.

The Luxembourg filing comes as Europe nears the end of the maximum transition period for companies operating under previous national crypto registrations. MiCA requires service providers to obtain permission from one member state, after which they can use the license to serve customers across the bloc.

The deadline has increased the commercial value of obtaining approval. Binance faces the prospect of losing permission to serve EU customers after its application in Greece was expected to be rejected, Reuters reported, citing people familiar with the process.

Binance said Greek regulators had not formally notified the company of a rejection and that it would inform users before the June 30 deadline.

Ripple’s preliminary approval does not guarantee that the final license will arrive by a certain date. Nevertheless, it puts the company closer to authorization at a time when some larger crypto companies are struggling to secure a European regulatory base.

RLUSD distribution has yet to translate into volume

Although RLUSD has shown significant growth since its launch in 2024, it remains much smaller than the stablecoins that dominate global crypto trading.

According to DeFiLlama, the market value was approximately $1.62 billion, with tokens issued on Ethereum and the XRP Ledger. By comparison, Tether’s USDT, the largest stablecoin by market capitalization, had about $186 billion in circulation, while Circle’s USDC had about $74.5 billion.

That difference explains why payment distribution is important to Ripple. RLUSD is unlikely to challenge the leading stablecoins due to the currency’s liquidity alone.

Embedding it into Flutterwave’s enterprise payments and money transfer infrastructure could thus create transactional demand that is more related to commerce than commerce. At the same time, the Luxembourg license could support the other end of those flows by providing European institutions with a regulated way to access Ripple’s payment and stablecoin services.

In theory, a European company could send value through Ripple’s infrastructure, while Flutterwave manages the collection, conversion or payout in an African market.

In practice, Ripple still needs to demonstrate that customers will prefer RLUSD over bank deposits, USDT, USDC or conventional payment networks. It must also ensure that sufficient liquidity exists to convert RLUSD into local currency without widening currency gaps and erasing the savings promised by faster settlement.