Since 2011, the cryptocurrency market has relied on on-chain metrics to assess investor behavior and market sentiment. However, the introduction of US Spot Bitcoin ETFs changed the way investors can now be exposed to Bitcoin.

ETFs can now bring billions of dollars to the market with minimal impact on on-chain data and without interacting with the blockchain.

As a result, conventional on-chain indicators have become less effective, as strong demand and price movements may no longer be reflected in network activity.

This change raises an important question: Can traditional on-chain metrics still effectively reflect market sentiment in an era driven by ETFs?

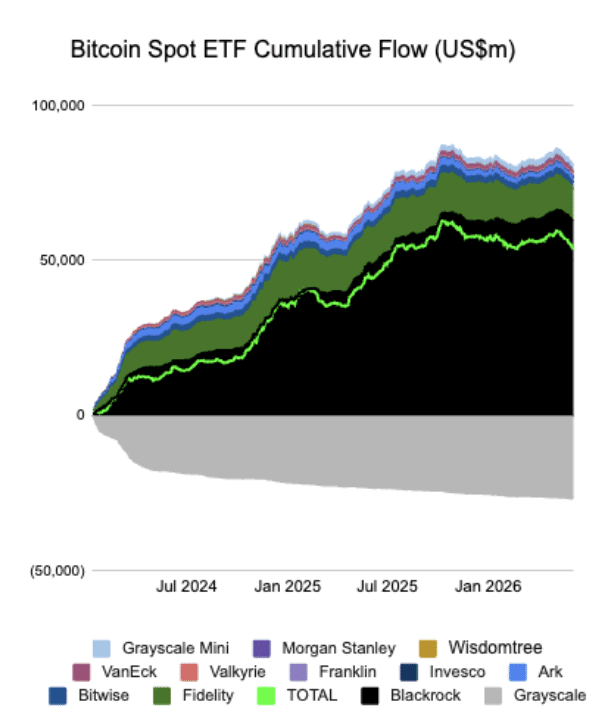

The rise of the ETF market

After the introduction of US Spot Bitcoin ETFs in January 2024, the dynamics have changed.

While institutional custodians held the underlying Bitcoin, investors could gain exposure to the cryptocurrency through investment accounts without setting up a wallet.

Strong inflows into ETFs could therefore boost Bitcoin’s price without causing an increase in on-chain activity. For example, in early 2024, Bitcoin rose above $70,000 even though active addresses were still well below their 2021 peak.

This led to a discrepancy between real investor demand and statistics within the chain. Needless to say, this has now become a common pattern across all cryptocurrencies that have ETFs.

The shift from layer 1 to layer 2

Before 2015, there was only one blockchain per ecosystem. Analysts had to track transactions, active addresses and gas prices on just one blockchain to determine demand and adoption for the entire ecosystem.

However, when Layer 2s were introduced, a lot of activity shifted away from the main chain, for example Ethereum [ETH]to L2 networks such as Arbitrum, Optimism, Base and zkSync.

These networks aggregate thousands of transactions into a single transaction that is handled on the main chain. Consequently, the overall activity of the network is no longer reflected in L1 statistics.

An example: the number of L1 transactions in Ethereum appears to have decreased since 2023. However, this does not mean that use has decreased. Instead, a significant portion of user activity has moved to L2s, where transaction volumes often exceed those on the main Ethereum chain.

Thus, analysts who focus solely on L1 data risk underestimating the true volume of activity in the Ethereum ecosystem.

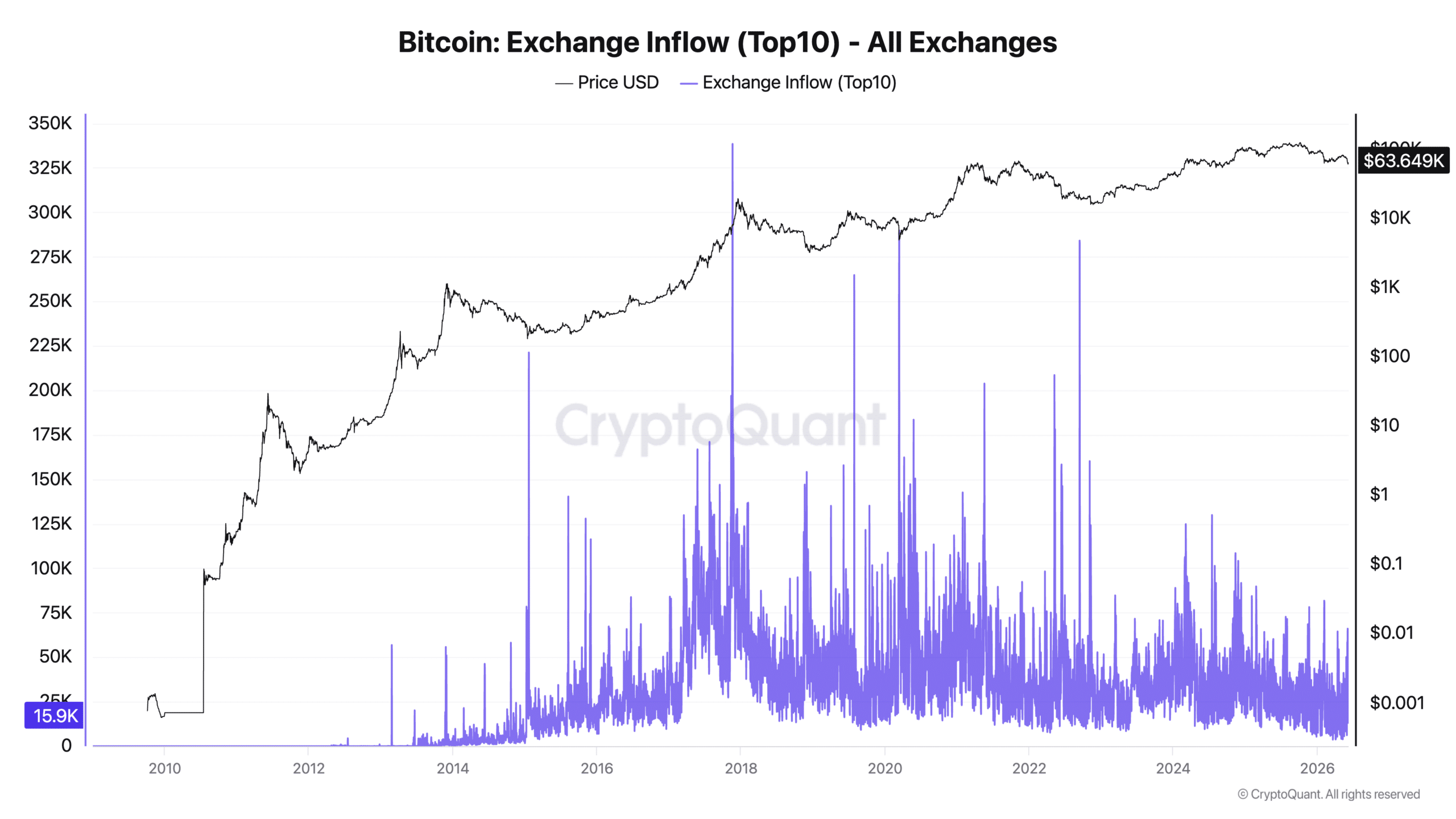

Is the inflow of foreign exchange losing its momentum?

Foreign exchange inflows were thought to be a consistent bearish indicator for many years. The logic was simple: Investors often got ready to sell when they transferred their coins from their personal wallets to exchanges.

In 2018 and 2021, large inflows often preceded significant market tops.

However, the way to interpret these movements has changed as institutional participation has increased. Exchanges now act as repositories and centers of collateral for trading firms, asset managers and hedge funds.

Rather than being sold right away, coins can be moved to exchanges for custody management, portfolio rebalancing, or collateral for derivatives. As a result, foreign exchange inflows no longer always indicate pressure to sell.

What has changed?

It is not that conventional indicators in themselves have become less accurate. It’s just that many of them were created for a market dominated by self-restraint, direct blockchain activity, and private investors.

Today, many other factors influence how activity takes place within the chain, including institutional investors, ETFs, custodians and L2 networks.

Therefore, many metrics are not necessarily incorrect, but they can be misleading if interpreted based on outdated assumptions.

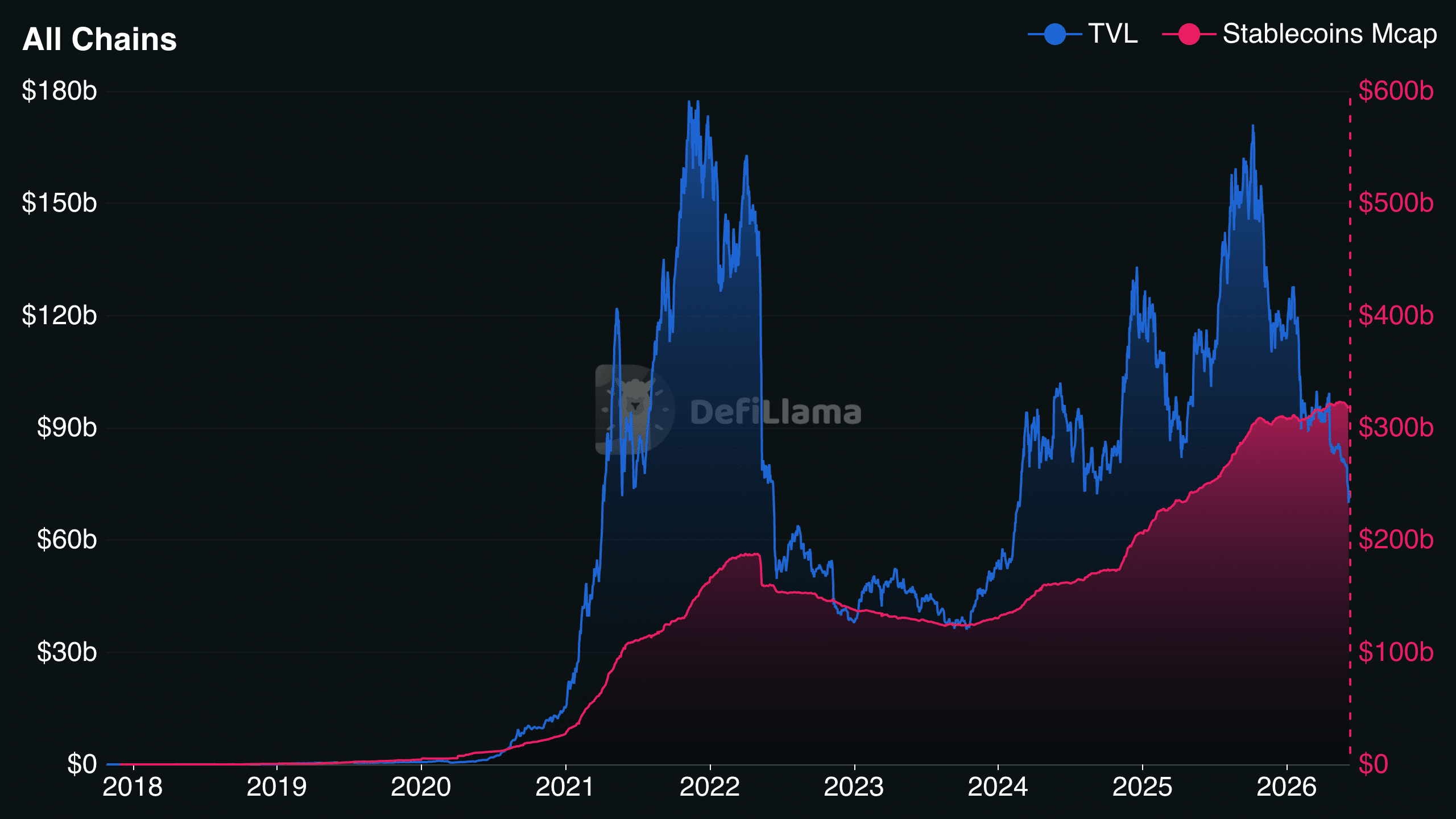

The new era of on-chain metrics

Total value locked (TVL), whale movements, and stablecoin analysis remain useful for sidestepping the drawbacks of other conventional on-chain metrics.

For example, increasing TVL typically indicates increasing user engagement, liquidity, and trust in a blockchain ecosystem. It provides a better picture of whether capital is flowing into decentralized applications or just sitting on the blockchain.

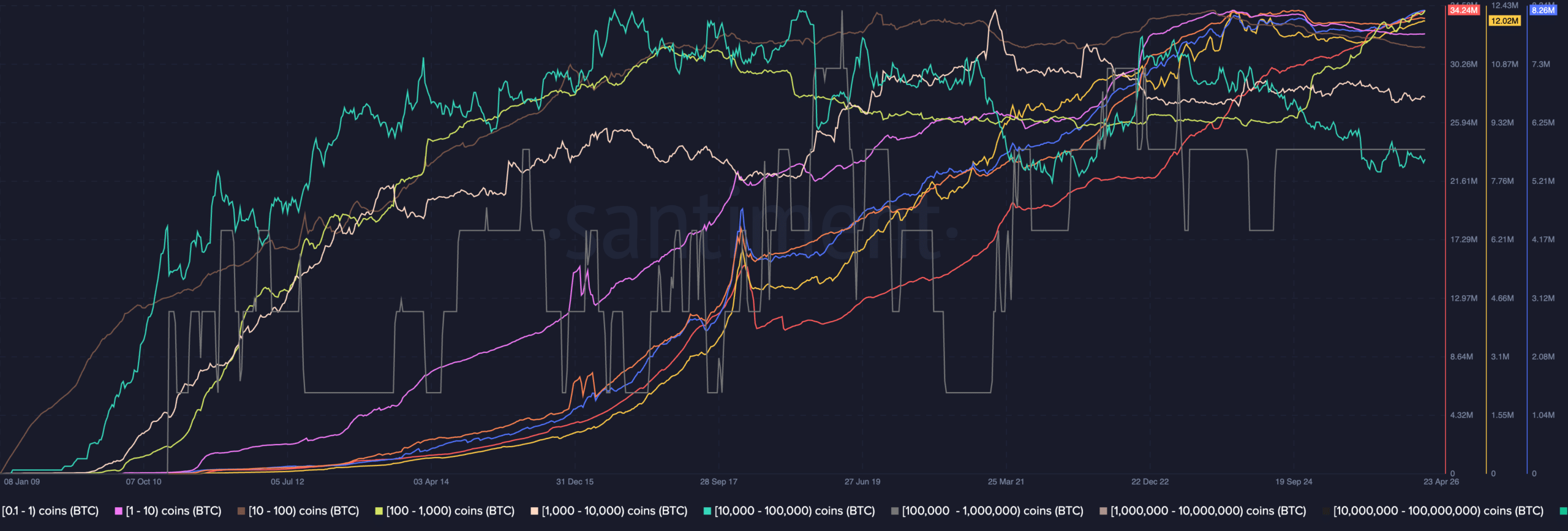

Whaling activities can also have a major impact on market sentiment and liquidity due to the size of their holdings. Occasionally, whale activity can be an early indication of new trends, as retail investors typically react after significant market movements have begun.

Within cryptocurrency markets, stablecoins often act as liquidity reserves.

By monitoring their supply, currency balances, and dominance, analysts can gain important insight into investor sentiment and liquidity conditions by determining whether capital is entering the market, staying out, or moving into riskier assets.

Overall, in the current crypto environment, no on-chain metric can adequately capture market sentiment in 2026.

Final summary

- The activities in the chain now look different thanks to Layer-2 networks, custodians, institutional investors and ETFs.

- Instead of relying on just one indicator, it is necessary to connect multiple data points to understand today’s cryptocurrency markets.