Euro-denominated stablecoin consortium Qivalis has received backing from 37 banks in 15 countries, and the asset is scheduled to launch in the second half of the year.

ING noted that stablecoins already enable large-scale cross-border payments and blockchain-based bond settlement, but most of that activity is denominated in US dollars, creating currency exposure for European companies whose payroll, taxes and accounting are denominated in euros.

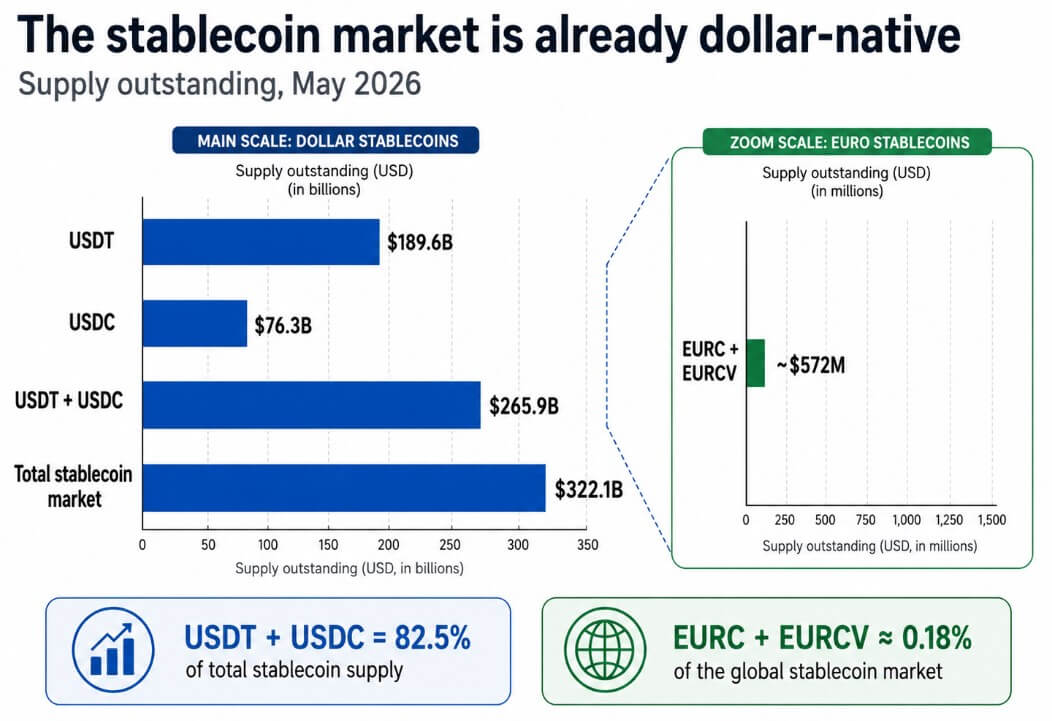

DeFiLlama estimates the global stablecoin market at $322.1 billion, with USDT at $189.6 billion and USDC at $76.3 billion, accounting for 82.5% of the total supply.

Circle reports €387.9 million EURC in circulation as of May 18, while SG-FORGE’s EURCV is €105.6 million.

These two leading euro coins are together worth about $572 million, about 0.18% of the global stablecoin market, and now the European distribution game must close a period of roughly 450 to 1 before it can challenge the rails.

Why the dollar’s lead is structural

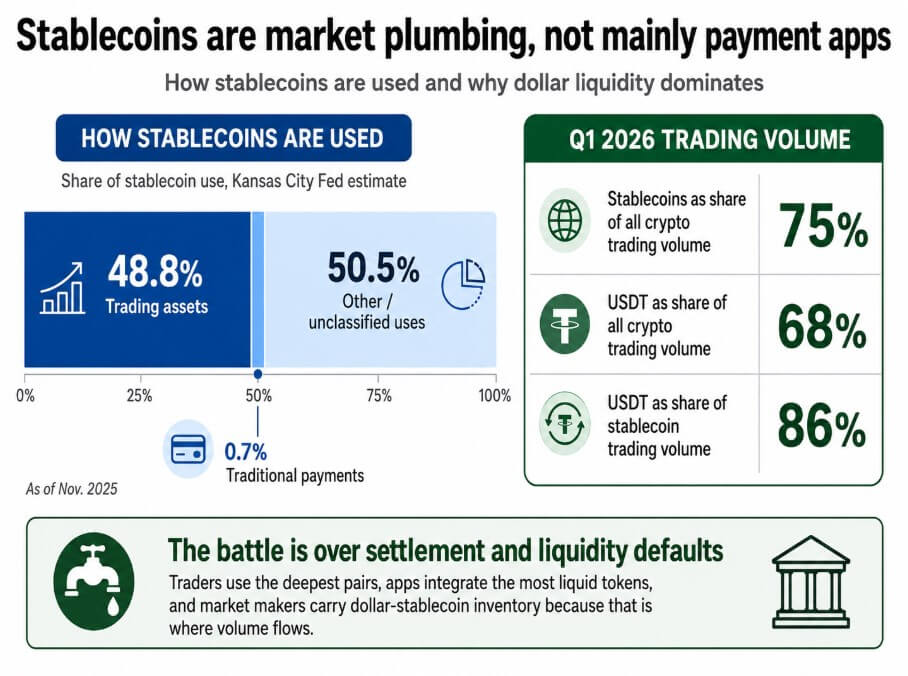

The Kansas City Fed estimated that as of November 2025, 48.8% of stablecoins existed were used as trading assets on exchanges, financial protocols and infrastructure, while traditional payments accounted for them only 0.7% of stablecoin usage.

CEX.IO’s Q1 data shows that stablecoins account for 75% of all cryptocurrency trading volume, with USDT alone accounting for 68% of all crypto volume and 86% of stablecoin trading volume.

Traders use the deepest pairs, applications integrate the most liquid tokens, and market makers hold dollar stablecoin inventory because that’s where the volume flows.

The White House fact sheet on the GENIUS Act states that the law will strengthen the dollar’s status as a reserve currency and increase demand for U.S. Treasuries by requiring stablecoin issuers to back their assets with dollars and Treasuries.

ECB President Christine Lagarde responded in May 2026 by noting that every dollar stablecoin that scales also increases demand for dollar-backed assets, and cited a research finding that an inflow of $3.5 billion into dollar stablecoins could reduce three-month government bond yields by 2.5 to 3.5 basis points.

RWA.xyz shows $33.8 billion in distributed tokenized real-world asset value and $340 billion in represented asset value, with tokenized US Treasuries alone exceeding $15.4 billion. Every tokenized asset has a settlement portion, and most of these portions are currently settled in dollar stable coins.

If European bonds, real estate funds and trade receivables continue to settle in USDT or USDC, European companies will have moved their assets on-chain, becoming dollar-native by default.

Europe’s counterattack is through banking networks

Under EU regulation on crypto asset markets, euro-denominated stablecoins issued by regulated entities can operate in all member states without separate national licenses.

That gives Qivalis a compliance advantage that Tether, which doesn’t have a MiCA license, can’t easily replicate. The bank distribution layer is what separates Qivalis from EURC, which has not yet attracted the institutional liquidity needed to scale.

The architecture being formed includes corporate finance management, cross-border supplier payments and the settlement of blockchain-based bonds and fund shares. These are institutional workflows where the connectivity of banks and the support of counterparties determine adoption.

Qivalis is betting that 37 banks can make euro stablecoins available to corporate treasurers, who receive stablecoins through their banking partners.

Liquidity traps and regulatory overcorrection

JPMorgan predicts that the stablecoin market will reach approximately $500 billion by the end of 2028, which, compared to the current $322.1 billion, implies year-over-year growth of approximately 18.6%.

In that scenario, dollar stablecoins grow proportionately and the overall market fails to expand fast enough to give euro tokens room to build meaningful exchange depth.

Qivalis will be a compliance product suitable for select cross-border treasury pilots, but not capable of resetting DeFi collateral preferences or executing exchange defaults.

The IMF’s COFER data for the last quarter of 2025 shows the euro at 20.25% of global official currency reserves, compared to the dollar at 56.77%.

In a bearish case, Euro stablecoins replicate that disparity, and European tokenized assets continue to settle into digital dollars as USDT and USDC dominate exchange pairs, DeFi pool depth, and market maker inventories.

If the ECB or national regulators restrict the issuance of public chain stable euro coins in favor of tokenized deposits or a CBDC, Qivalis’ banking distribution network will become irrelevant.

Banks that have joined to offer a regulated stablecoin may end up offering another instrument that does not interoperate with DeFi protocols or non-EU exchanges under a different framework.

This fragmentation means dollar tokens remain the practical standard for any transaction crossing EU borders.

The bridgehead for the euro scheme

Standard Chartered predicts the stablecoin market will reach $2 trillion by the end of 2028, with net new demand for Treasuries up to $1 trillion.

Reaching $2 trillion from $322.1 billion would require roughly 102.8% annualized growth, or about $54 billion in net supply growth per month through the end of 2028.

| Scenario | 2028 stablecoin market | Euro stablecoin share | Liquidity result in euros | Strategic significance |

|---|---|---|---|---|

| Bear/dollar trap | ~$500 billion | <1% | <$5 billion | Euro tokens remain compliance products; dollar rails dominate the settlements. |

| Basic / double rail | ~$1T | 1–2% | $10 billion – $20 billion | Europe gets usable domestic rail lines, but global liquidity remains USD-led. |

| Bull/Euro bridgehead | ~$2T | 3–5% | $60 billion – $100 billion | Euro stablecoins become credible settlement assets for EU tokenized securities, funds and corporate cash flows. |

In that environment, euro stablecoins, capturing 3 to 5% of the market, would mean $60 billion to $100 billion in euro-denominated on-chain liquidity, enough to support real exchange depth, DeFi collateral use, and token fund settlement at an institutional scale.

Euro stablecoins can secure that position by becoming the default settlement vehicle for EU tokenized securities before those standards harden around the dollar rails, a price that carries its own logic independent of any movement of USDT in global crypto trading.

The RWA market is still in its early stages, meaning the window for setting up euro-denominated settlement rails is open. If Qivalis achieves sufficient liquidity before tokenized EU assets adopt dollar defaults, the European financial infrastructure will avoid becoming dollar-native at the plumbing layer.

That outcome would decide whether the next generation of European corporate finance runs on digital euros or digital dollars.

The fight is over settlement defaults

Europe’s goal is to make euro-denominated money available when the traditional financial sector moves into the chain and before defaults occur.

The 37-bank Qivalis consortium believes that institutional distribution can generate the liquidity, counterparty network and compliance stack integration that companies need before they can route treasury flows through a stable euro currency.

Whether that bet will pay off in late 2028 will depend on how quickly tokenized asset markets expand, how aggressively European banks activate their Qivalis relationships, and whether regulators treat public euro stablecoins as infrastructure worth protecting or as a risk to be mitigated.