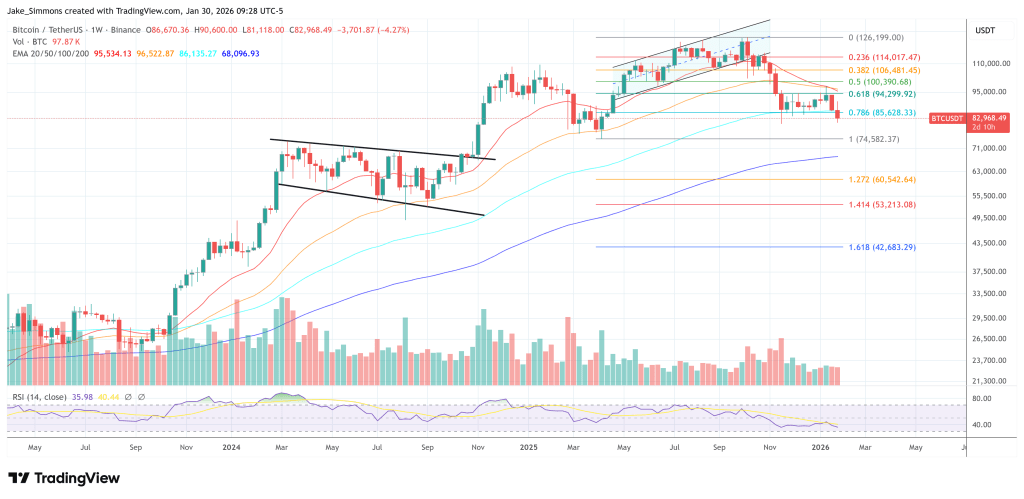

Bitcoin’s sharp drop to $81,119 on January 30 came with a blow to the derivatives market: forced long closes reached extreme levels, but perpetual funding remained decisively positive. This mix complicates the overall interpretation of whether the market has already ‘cleaned up’ leverage or is still prepared for repeated waves of liquidation.

Is Bitcoin Deleveraging Over?

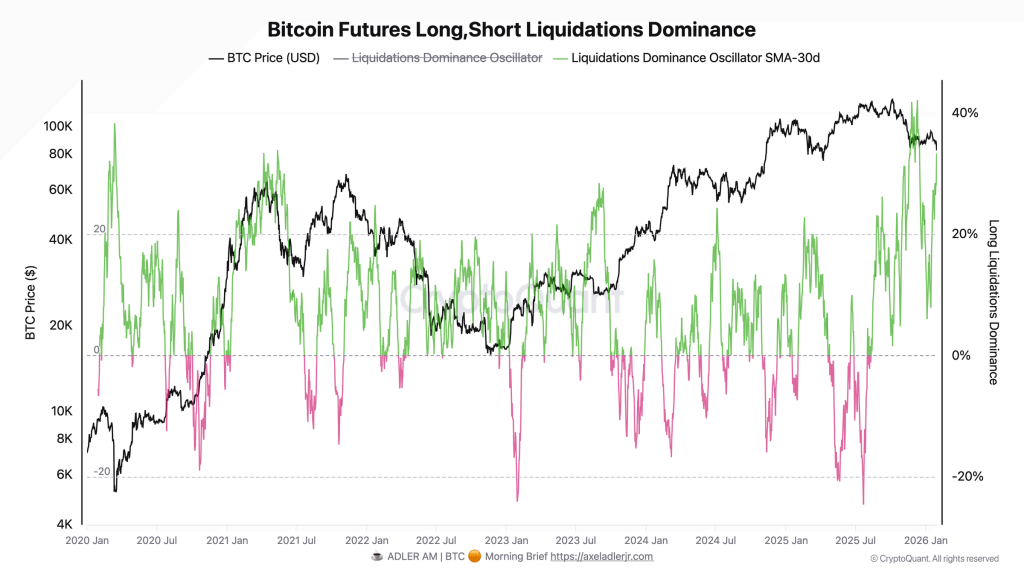

On-Chain analyst Axel Adler Jr., in his Morning Brief: be to a “cascade of forced closures” in the past 24 hours, with long liquidations playing the leading role. Its liquidation dominance oscillator tracking the balance between long and short liquidations printed around 97%, while the 30-day moving average rose to 31.4%. In simple market structure terms, this means that the deleveraging push has been very one-sided, not just on the day itself, but as a sustained pattern over the past month.

The reason traders look at these types of extremes is the tendency for liquidation flows to cluster and then fade, leaving room for short-term stabilization. Adler was careful to frame that dynamic, emphasizing that an “extreme” reading is not the same as confirmation that salespeople are ready.

Related reading

“Extremes of the oscillator often coincide with the peak of forced selling and can lead to short-term stabilization. However, this is not a reversal signal without confirmations – for a sustainable ‘local bottom’ scenario it is important to see at least a normalization of the oscillator towards zero or a decline from the 30-day average.”

This is the first condition for the deleveraging cycle to be called “over”: the liquidation imbalance must cool down, rather than simply reach a peak.

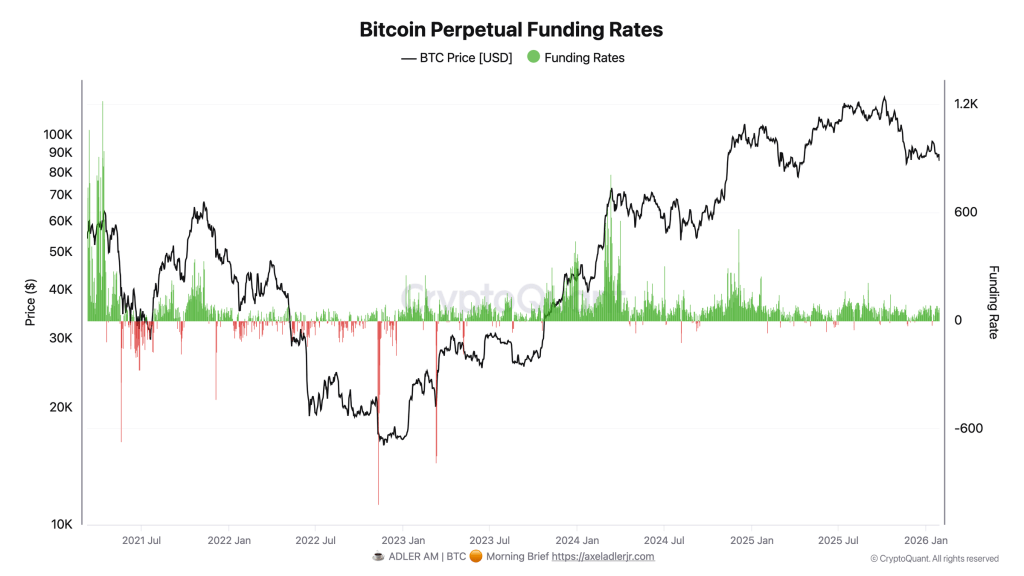

The bigger tension in Adler’s talk is that even after the price drop and liquidation cascade, funding remained positive: 43.2% annualized on that day, according to his numbers. While that’s well below the 100%+ annualized level seen during the October to November peaks, it still implies the market is paying to stay long rather than being short-paid.

Funding doesn’t just reflect sentiment; it reflects positioning pressure. If funding refuses to turn around despite a sell-off, it could mean longs are quickly rebuilding exposure, or the market never fully unwound bullish leverage in the first place. Adler’s conclusion is that this last risk is still on the table.

“Positive financing amid massive liquidations increases the risk of repeated deleveraging: this means that the market is recovering from the long position quickly enough or is not yet ready to unwind it completely. Complete ‘capitulation of derivatives’ is often accompanied by a transition of financing into neutral or negative territory – this has not happened yet.”

Related reading

In other words, the liquidation may have been violent, but the incentives embedded in the perpetrators still tend toward a long demand. That matters because it perpetuates the same vulnerability: another downward push can turn newly loaded longs back into liquidation fuel.

Adler summarized the combined signal of the two charts as a washout that may be intense, but not necessarily definitive.

“Together, the two charts paint a picture of likely incomplete deleveraging: liquidations are hitting longs extremely hard, but overall positioning remains bullish. The liquidation cascade (long dominance ~97%) is a symptom of market overload with long positions, but not necessarily a final cleanse. Continued positive funding (43% annualized) may indicate that demand for long positions is not being broken and that the deleveraging process has not yet been completed.”

Until these confirmations emerge, the base case in his briefing is less “final capitulation” and more “incomplete deleveraging,” a market that has already flushed leverage once, but that may not happen if the long appetite remains intact through drawdowns.

At the time of writing, BTC was trading at $82,968.

Featured image created with DALL.E, chart from TradingView.com