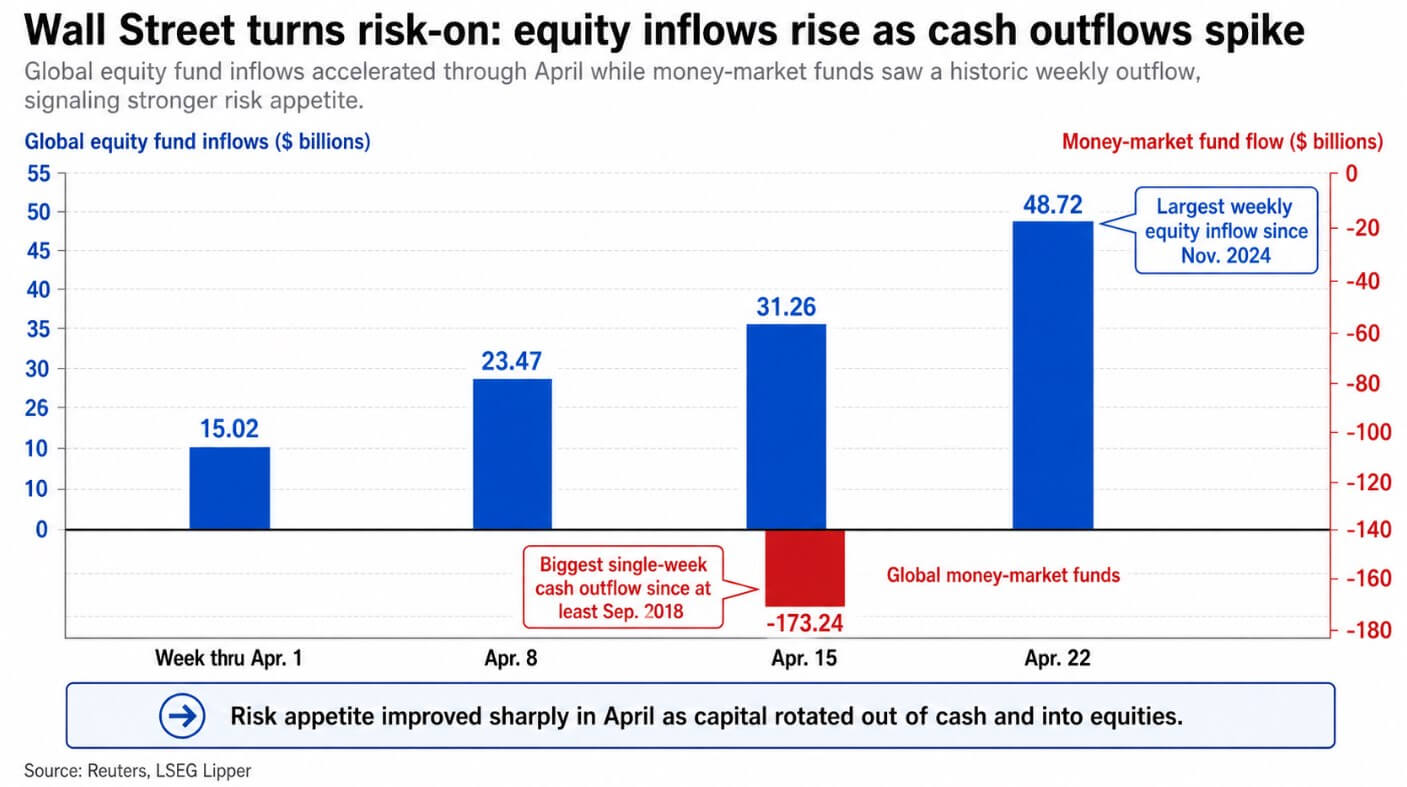

Global equity funds raised more than $15 billion in the week to April 1, then $23.47 billion, $31.26 billion and finally $48.72 billion in the week to April 22.

Global money market funds simultaneously posted outflows of $173.24 billion in the week to April 15, the largest single-week cash outflow since at least September 2018.

Together, the numbers create a risk signal of roughly $292 billion, combining $118 billion in four-week global equity fund inflows with separate weekly cash outflows of $173 billion.

Coinbase and Glassnode’s Q2 Institutional Outlook estimate BTC’s daily return correlation with the S&P 500 at 0.58 in Q4 2025, while its relationship with gold remains negligible.

When capital flows toward risk, it flows toward the asset class in which Bitcoin currently behaves.

The sharper details come from Coinbase’s survey of 91 global investors, comprising 29 institutions and 62 non-institutions, conducted between March 16 and April 7.

Among institutional respondents, 75% view Bitcoin as undervalued, while 61% of non-institutional crypto investors share the same view. Only 7% of institutions and 11% of non-institutions consider BTC overvalued.

These numbers describe a market where sizeable buyers still see room for upside. Capital turning into risk meets an asset still considered cheap by the most sophisticated holders and held by a market that has yet to repurpose itself for euphoria.

The image of the chain

Supply of BTC that had moved in the past three months fell 37% in the first quarter, while supply that hadn’t moved in more than a year rose 1%.

Speculative holders who bought at higher prices went through the drawdown, and long-term holders accumulated.

The Puell Multiple fell to 0.7 in the first quarter, implying that miners’ earnings were about 30% below the one-year baseline, a zone that has historically coincided with accumulation periods.

Long-term holders’ balances rose while currency balances fell, and stablecoin supply rose from $308 billion to $320 billion, meaning dry powder remained within the crypto market during the sell-off.

Options open interest grew 2.4%, and perpetual futures open interest recovered roughly 8.6%, creating a market that absorbed deleveraging and rebuilt it at a measured pace.

| Metric | Reading | Why it is important for the BTC setup |

|---|---|---|

| Institutional respondents view BTC as undervalued | 75% | Large investors still see upside from current levels |

| Non-institutional respondents view BTC as undervalued | 61% | A constructive vision extends beyond the institutions |

| Institutional respondents view BTC as overvalued | 7% | Little sign of institutional euphoria |

| Non-institutional respondents view BTC as overvalued | 11% | The foam still looks limited |

| Survey sample | 91 global investors | Provides context for how broad the sentiment snapshot is |

| Institutional part of the sample | 29 respondents | Indicates that the setting result is based on a defined subgroup |

| Non-institutional part of the sample | 62 respondents | Balances the institutional view with the broader sentiment of crypto investors |

| Survey field dates | March 16 to April 7, 2026 | Positions the research in the run-up to the second quarter |

| BTC correlation with S&P 500 (4Q25) | 0.58 | Supports the idea that BTC still trades as a risky asset |

| BTC correlation with gold | Negligible | Suggests that BTC is not behaving as a defensive hedge in this regime |

| Read through for Q2 | Undervalued + risk sensitive | Macro risk flows could support BTC without the need for euphoria |

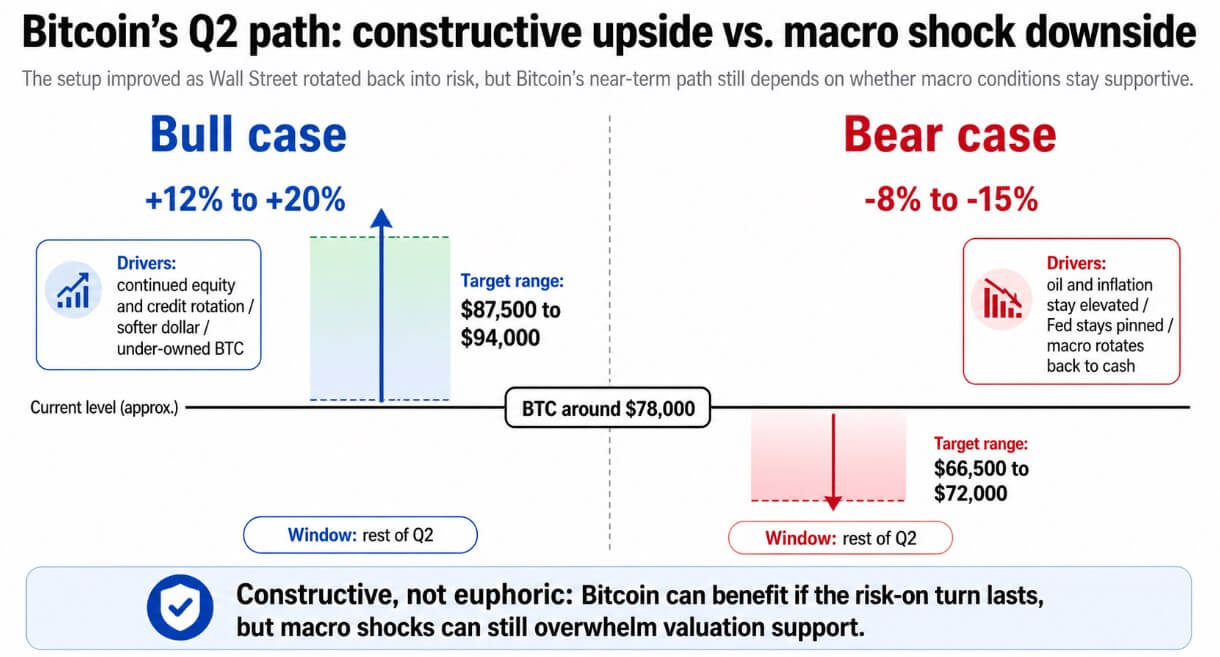

The bull case

If April’s equity rotation continues to expand into high-yield, retail, and emerging market risks, Bitcoin will get in the way of that capital.

EPFR described a “clear increase in risk appetite”, with high-yield bond funds recording their first inflows since mid-February and private credit flows reaching an eight-week high.

In that scenario, institutional beliefs in undervaluation and a cleaner positioning in the chain create a repricing process with real room for maneuver. Coinbase survey respondents are positioned for caution, meaning an improving macro environment leaves them underutilized.

A 12% to 20% gain from current levels through the remainder of the second quarter would put BTC in the $87,500 to $94,000 range and could be driven solely by continued institutional rotation.

The weakening of the dollar, already visible in last week’s intervention-driven move that saw the dollar index fall 0.8%, is providing a secondary tailwind.

Bitcoin tends to closely follow global dollar liquidity, and softer financial conditions favor risky assets on the margin.

The bear case

Coinbase’s formal stance for the second quarter remains neutral, and the conditions it needs to see before it becomes more constructive, such as a definitive end to the Middle East conflict, the withdrawal of oil, and an easing of inflation, are still to come.

If oil prices remain high and the Fed remains in the grip of ongoing inflation, Bitcoin’s stock correlation would turn from a tailwind to a headwind. When the macro desks move towards cash again, as they did in early March, BTC will trade as a liquidity beta on the way down.

In that case, macro dominance transcends the conviction of institutional undervaluation. Survey respondents may believe BTC is cheap and are still on the sidelines as geopolitical uncertainty shapes their positioning.

The on-chain accumulation data would be constructive in the longer term, but a renewed macroshock would overwhelm these measurements in the short term.

An 8% to 15% decline from current levels, to roughly $66,500 to $72,000, matches the magnitude of previous macro-driven BTC corrections and would only require a return to March’s defensive flow pattern.

The rest of the quarter revolves around whether April’s equity and credit rotation proves sustainable or bounces back on the next geopolitical headline, and whether Bitcoin’s correlation to equities remains elevated or drifts toward a more independent path as crypto-specific flows begin to dominate price action.

The constructive arguments rest on broader markets taking on more risk again, while Bitcoin’s best-informed holders remain underserved for a clean recovery.