Singapore-based crypto trading desk QCP Capital has warned that Bitcoin may not benefit from the US-Iran deal. According to QCP analysts, Strategy had limited coverage for dividend payments. As such, it could be forced to sell more of its BTC holdings to meet this obligation.

Strategy has extended the term to roughly 7.5 months before running out of money for dividend payments. In the short term, we think this overhang may continue to hold Bitcoin back from fully participating in the broader macro optimism.

The dividends are linked to the preferred shares, led by Stretch [STRC]which have played an important role in attracting capital for BTC purchases.

STRC is designed to maintain a price of $100 per share. However, at the time of writing, it was trading at a huge discount of $89. This underlined once again STRC emergency and muffled question.

For longtime Bitcoin and strategy critic Peter Schiff, investors in Strategy’s flagship stock, MSTR, will be the ones to bear the brunt of the stock dilution.

STRC closed at $89. Investors who paid $100 last month are down 11%. The current yield for new buyers is 12.92%. If Saylor increases the yield to 13%, he will have to sell even more MSTR at deeper discounts to finance it. If he doesn’t increase yields, the STRC price will continue to fall.

The strategy dismisses dividend coverage concerns

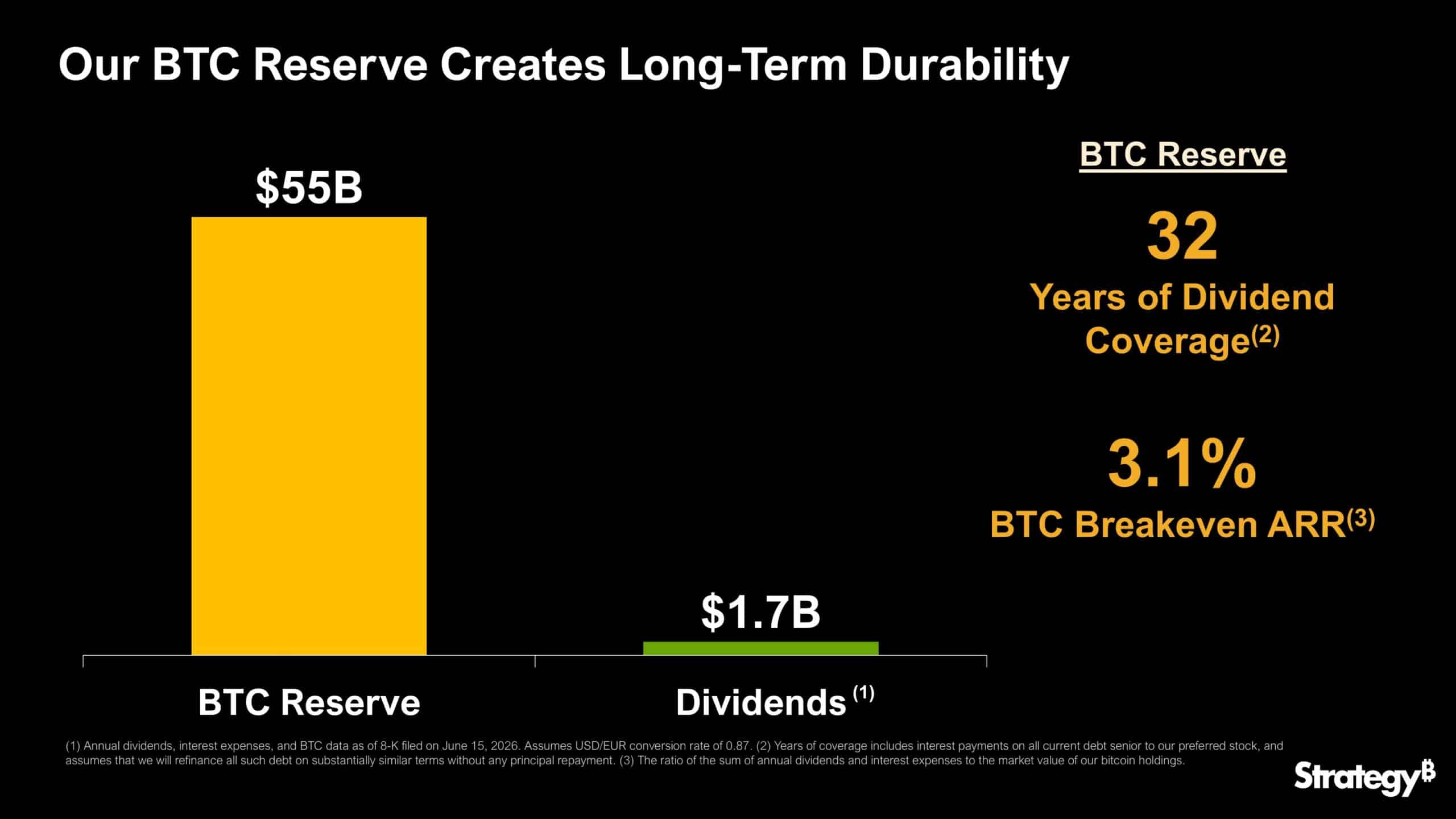

Amid intense FUD, Strategy recently cleared the air and noted that it has had 32 years of dividend coverage. In doing so, it cited the current value of its BTC holdings.

However, critics were quick to point out that the asset would fall faster if Strategy started liquidating its BTC holdings. In short, coverage will shrink even further, similar to how recent this is 32 BTC sale The price of BTC was dragged sharply towards $60,000.

In fact, Strategy’s response raised more questions than the certainty of the market it was looking for. For example, one market observer said the statement confirms the company is a “permanent seller.”

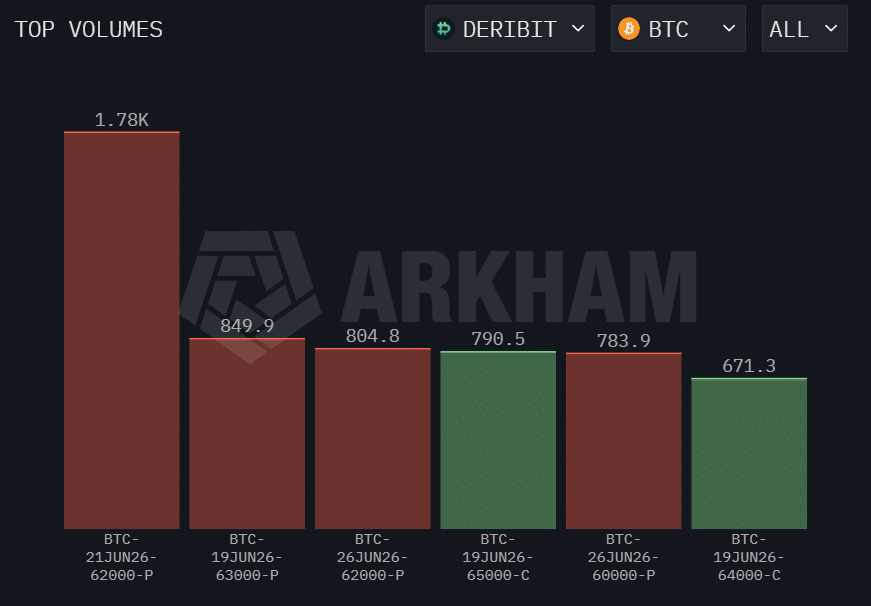

However, it is worth pointing out that BTC’s recent correction was accelerated by that of the Fed aggressive interest rate pause. In fact, as evidenced by Options data, advanced players have been actively hedging against a potential dip to $62,000 and $60,000.

This was underlined by high option volumes, especially puts (bearish bets) at these strike prices, as the second quarter comes to an end.

Overall, despite Strategy’s overhang, the market did not expect a sharp drop in BTC below $60,000. However, the market’s positioning could change if Strategy confirms another BTC sell-off.

Final summary

- QCP believes that Strategy could be forced to offload more BTC to fund dividend obligations.

- Strategy’s attempt to insure the market with “32 years of coverage” led to more fear and backlash.