BlackRock CEO Larry Fink told shareholders this year that digital assets, in addition to private markets, insurance and active ETFs, could each become $500 million in revenue for the company within five years.

According to him:

“From private markets to insurance, from private markets to wealth, digital assets and active ETFs, we think all of this could generate $500 million in revenue over the next five years.”

For at least one of these categories, the runway may be shorter than the timeline suggests.

BlackRock’s crypto ETF business has already generated enough fee income in its first two years that Fink’s five-year target appears conservative on a cumulative basis.

BlackRock’s most profitable fund in a 1,000-unit lineup

The iShares Bitcoin Trust ETF, which trades as IBIT, tops BlackRock’s rankings in terms of fees and income.

Of the more than 1,000 exchange-traded funds the firm operates worldwide, IBIT generates more sponsorship fees per dollar of assets than all comparable funds, fund filings show.

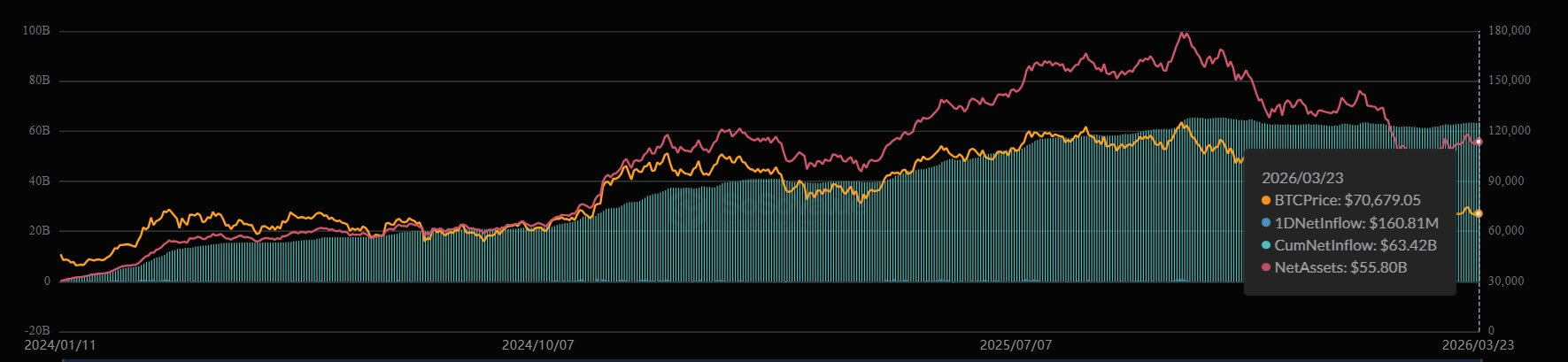

The fund surpassed $100 billion in assets at a pace roughly five times faster than any ETF, attracting capital from both institutional investors and retail buyers.

Of the 20 largest ETFs based in the United States, IBIT is the clear outlier in terms of age. Every other fund on that list spent years building the asset base that IBIT achieved in less than two years.

That rise was helped by Bitcoin’s meteoric rise following Donald Trump’s 2024 election victory, peaking at an all-time high above $126,000 last October.

Since then, prices have fallen and IBIT’s net asset value is down 18.82% on a total return basis through March 23.

Still, the decline has reduced equity without interrupting the reimbursement engine.

BlackRock’s filings show that IBIT collected about $47.5 million in net sponsorship revenue during its 2024 launch year and about $174.6 million in 2025. The iShares Ethereum Trust ETF, or ETHA, added about $0.9 million in 2024 and about $18.4 million in 2025.

Together, the two funds have generated approximately $241.4 million in cumulative net sponsorship revenue in the first two calendar years.

How BlackRock can make $500 million a year from crypto ETFs

Reaching $500 million in one year, rather than over several years, requires a different scale.

At a 0.25% sponsorship fee, every $1 billion in assets generates $2.5 million in annual revenue. Based on that, BlackRock’s crypto ETF complex would need about $200 billion in fees to generate $500 million in one calendar year.

At the time of writing, BlackRock’s crypto ETF complex held approximately $61.6 billion in assets. IBIT accounted for $54.64 billion, ETHA for $6.70 billion, and the iShares Staked Ethereum Trust ETF, or ETHB, for $261.8 million.

Launched on March 12, ETHB provides exposure to the price of Ethereum and staking rewards from a portion of the fund’s investments. At that combined asset level, annualized revenue was approximately $153.7 million.

So about $138.4 billion still needs to be added before the company reaches the $200 billion threshold.

The route from here depends on two variables. Higher crypto prices would increase the value of existing assets, while new inflows would add new capital. In practice, a path to $500 million per year likely requires both.

Price increases in themselves do not appear to be sufficient according to most sales forecasts.

Standard Chartered’s base case called for Bitcoin at $100,000 and ETH at $4,000 by the end of 2026. Repricing BlackRock’s current shares to that level, without new inflows, would lift the complex to around $91.8 billion, still less than half the target.

A more bullish setup, using Bernstein’s repeated Bitcoin forecast of $150,000 alongside $4,000 ETH, narrows the gap but does not close it. In that scenario, BlackRock would still be short about $68.9 billion.

On that basis, the remaining distance must come from new investor money.

Facts of SoSoValue show cumulative net inflows of approximately $63.4 billion in IBIT, $11.87 billion in ETHA and $163 million in ETHB.

Since IBIT’s launch, the three funds have attracted combined creations at a rate of approximately $34 billion per year. If those rates were maintained and prices remained the same, BlackRock could close the remaining asset gap in just over four years.

$500 million in cumulative fees point to a 2027 crossover

On the other hand, BlackRock’s crypto ETF complex could reach $500 million in cumulative fees as soon as next year.

IBIT holds approximately $55.6 billion in net assets, while ETHA holds approximately $6.85 billion. Each fund charges an annual sponsorship fee of 0.25%, bringing their combined annualized revenue to approximately $156 million.

Add that run rate to the $241.4 million the funds have already generated, and the path to $500 million becomes largely a matter of time.

If combined assets remain at current levels, annual fee flow would remain close to $156 million, and BlackRock would pass $500 million in total sponsorship revenue around mid-2027. If assets rise 40% to 50%, that crossover could happen in early 2027.

| Scenario | Assumption of assets | Approximate Annual Compensation Rate | Estimated timing to reach $500 million in cumulative fees |

|---|---|---|---|

| Basic case | Assets remain near current levels of approximately $62.5 billion | About $156 million | Around mid-2027 |

| Higher power case | Assets increase by 40% to 50% | About $218 million to $234 million | Early 2027 |

| Moderate downturn | Assets drop by about 30% | About $109 million | Late 2027 to early 2028 |

| Serious downturn | Assets are halved and remain there for a longer period of time | About $78 million | Materially later than early 2028 |

A weaker market would slow the pace, but not by much. With an asset base decline of around 30%, BlackRock would still be on track to reach the milestone in late 2027 or early 2028.

To meaningfully slow down the timeline, assets would likely need to be cut in half and held at that level for an extended period of time.

Putting the number into proportion

BlackRock’s plan to earn $500 million in fees from crypto ETFs should be compared to established ETF fee pools to gauge scale.

SPDR Gold Shares, the largest U.S. gold ETF, held about $151.1 billion and charges an expense ratio of 0.40%, which equates to about $604 million in fees per year.

For BlackRock’s crypto ETF complex to produce $500 million annually at a 0.25% fee, it would have to grow to about 132% of GLD’s current size.

Inside BlackRock financial affairsrevenues at such margins would also make sense, although still far from central.

The company ended 2025 with total assets under management of $14 trillion. It reported $24.216 billion in revenue and $19.179 billion in investment advisory, administrative fees and securities lending income. A $500 million crypto ETF fee stream would amount to approximately 2.1% of total revenue and 2.6% of the fee-based line.

That would not shift the company’s financial center of gravity. However, it would place crypto ETFs more firmly among the established revenue streams within BlackRock’s fund business.

Viewed this way, the endpoint is less about a single prediction than about scale. The path is not based on one price target, one week of inflows or one product launch. It rests on reaching approximately $200 billion in assets.