Bitcoin’s latest dip below $80,000 shows how quickly the bond market has regained control of crypto trading, even after lawmakers introduced one of the most closely watched regulatory bills in the industry.

Data from CryptoSlate showed the top asset trading at $79,083 at the time of writing, down more than 3% after another failed attempt to stay above $82,000.

Blockchain analytics company Santiment attributed the reversal of a “buy the rumor, sell the news” market reaction to the passage of the CLARITY Act by the Senate Banking Committee. This was a policy milestone that would typically improve sentiment on digital assets by moving market structure legislation closer to a full vote in the Senate.

However, the rally attempt faded as traders shifted their focus back to government bonds.

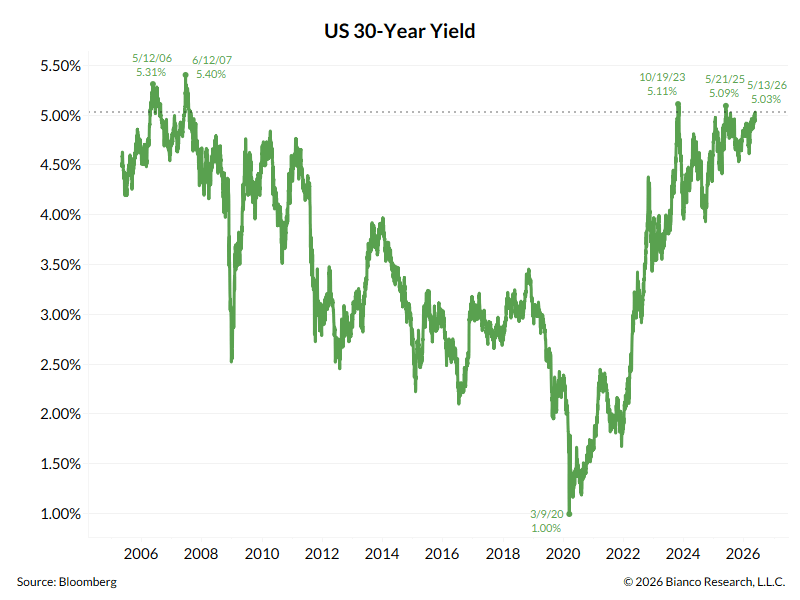

Ten-year government bond yields rose above 4.5% for the first time since June 2025, while 30-year yields rose to 5.1%. Jim Bianco of Bianco Research said the long bond was just 8 basis points away from a new 19-year high.

This move has increased the return threshold for Bitcoin exposure. Higher rates make cash, bills and longer-term government bonds more competitive, as BTC tries to recover an important technical level.

Nicolai Sondergaard, a research analyst at Nansen, told us CryptoSlate that rising returns reduce the compensation investors receive for holding assets like Bitcoin.

According to him:

“Ten-year Treasury yields pushing toward multi-month highs are squeezing the risk premium available for assets like BTC, which remain structurally sensitive to the real interest rate environment. At current levels, the cost of holding zero-interest assets increases significantly when alternatives offer 4.5% risk-free.”

The result is a market where crypto-specific advances are no longer enough to drive price action on their own. Washington has improved the policy outlook for the sector, but the interest rate market is driving the allocation decision in the short term.

ETF outflows show where interest rate pressure is ending up

The Treasury Department’s pressure is now manifesting in one of Bitcoin’s main demand channels: US spot Bitcoin exchange-traded funds.

SoSoValue data shows the funds were on track for weekly outflows of more than $700 million, the biggest weekly withdrawal since late January. The pullback removes a key source of spot demand as Bitcoin tries to reclaim the $82,000 area and get back above its 200-day moving average.

The ETF channel has become central to Bitcoin’s market structure since the funds began trading, giving institutions a regulated, liquid way to increase their exposure. When these flows weaken, the spot market loses one of its clearest sources of marginal demand.

Lacie Zhang, a research analyst at Bitget Wallet, shared CryptoSlate that higher interest rates have made institutional buyers more selective, as government bonds now offer a stronger return profile.

She said:

“Rising US Treasury yields pose a clear macro headwind for Bitcoin. As yields rise, the relative attractiveness of Treasuries improves, increasing the opportunity cost of holding a volatile, non-yielding asset like BTC.”

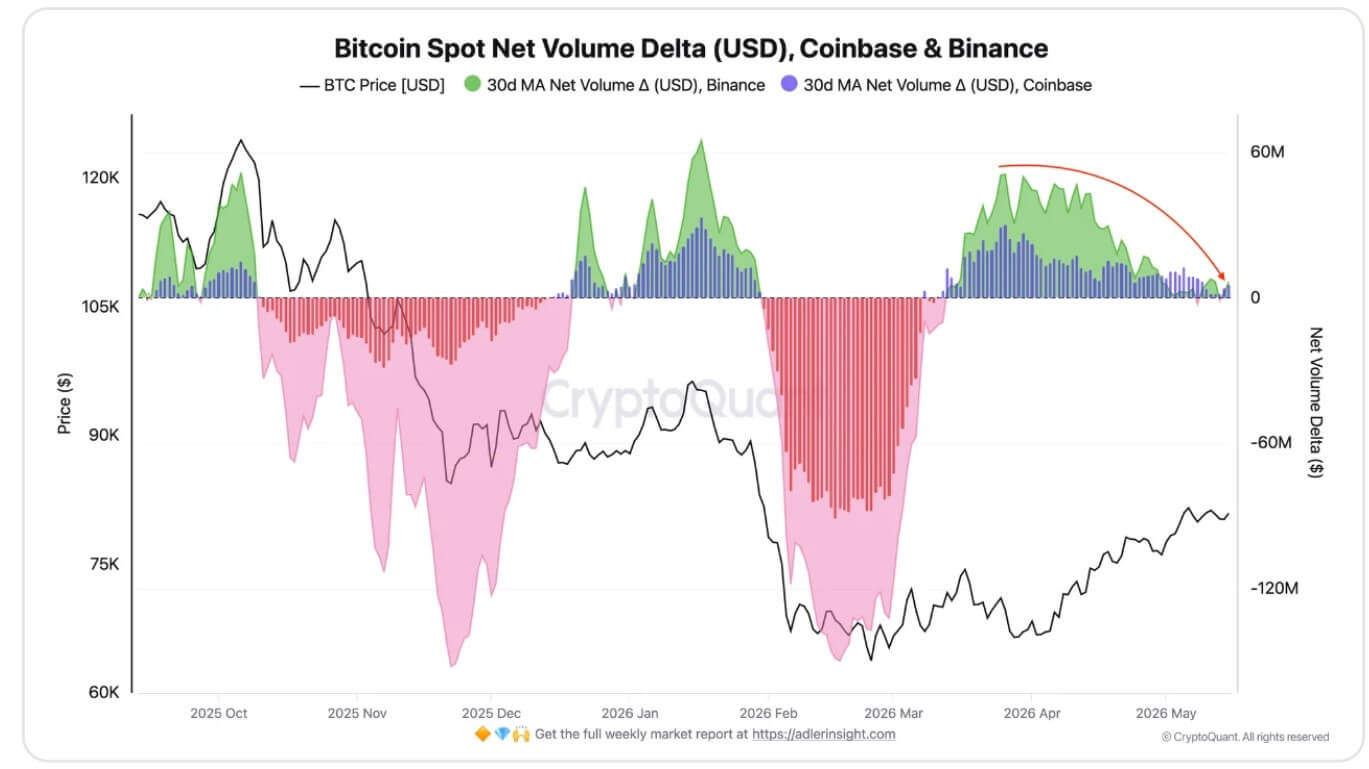

Additionally, the weaker ETF picture is reinforced by on-chain spot flow data.

Data from CryptoQuant shows that the Cumulative Volume Delta at major locations has deteriorated after stronger readings in March. According to the company, monthly averages of $50 million on Binance and $30 million on Coinbase have fallen to about $6.5 million and $5.7 million, respectively.

The indicator also briefly turned negative on May 8, indicating a weaker balance between buyers and sellers. That leaves Bitcoin trading around a key pivot zone, with spot support thinner than during the earlier phase of the rally.

Moreover, the macroeconomic backdrop has also become less supportive of risky investments. The unresolved conflict between Iran and the US has increased uncertainty around growth and inflation, even after President Donald Trump initially suggested the conflict would last only a few weeks.

Bitcoin’s hedge case remains in the longer term

Despite this current market situation, the broader investment case for Bitcoin has not disappeared.

Analysts at Bitunix report this CryptoSlate that while higher government bond yields may put pressure on BTC in the short term by draining liquidity and reducing speculative appetite, the same forces could strengthen the case for scarce, non-government assets.

According to the company, as investors demand greater compensation for U.S. deficits, debt issuance and inflation risk, Bitcoin’s steady supply could continue to attract buyers looking for assets outside the sovereign credit system.

However, this argument is more likely to influence long-term strategic allocation than short-term positioning.

For now, Bitcoin appears to be dependent on two catalysts: a decline in government bond yields or a recovery of ETF inflows strong enough to absorb the interest rate shock.

Without both, price action could remain in the middle between support in the upper $70,000 and resistance around $82,000.

Stablecoins and tokenized Treasurys are cautiously attracting capital

In light of the current interest rate environment, crypto traders are repositioning their capital in the market.

Nansen’s Sondergaard said smart-money wallets have been incrementally moving toward stablecoins over the past two weeks, showing a preference for flexibility over directional exposure.

This shift signals caution rather than a complete exit from the market as traders look for new market catalysts for their trades.

Moreover, US government bonds also benefit from the higher interest rates.

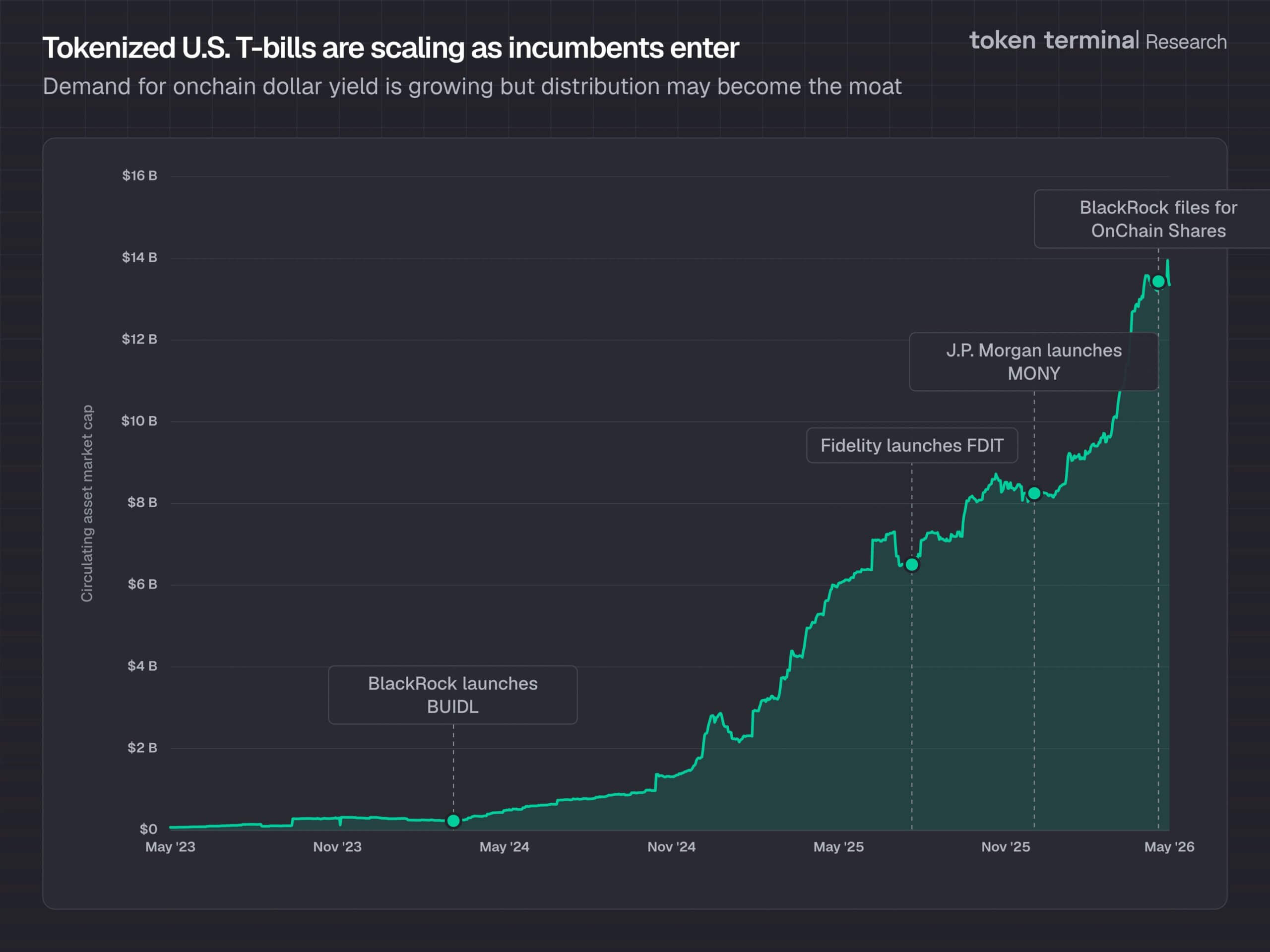

Marcin Kazmierczak, co-founder of RedStone, explains CryptoSlate that risk-free returns above 4% have become a direct competitor to non-yielding assets, while driving demand for tokenized real-world assets.

Data from Token Terminal shows that tokenized US Treasuries have reached a record high of $15.35 billion in value, up from around $8.9 billion at the start of the year. This means a growth of 70% in less than five months.

According to Kazmierczak, this growth shows that capital is still moving along blockchain rails, but with a stronger preference for products tied to short-term sovereign debt. He added:

“BlackRock BUIDL, VanEck VBILL, Apollo ACRED, Hamilton Lane SCOPE, Franklin Templeton BENJI are all live in production today. Institutions get 4%+ returns with 24/7 settlement, programmable collateral and ability to compound with DeFi.”

This shift gives the current market cycle a different shape than previous interest rate shocks.

Now Bitcoin is absorbing the pressure of a stronger bond market, while another corner of the crypto industry is expanding because that same bond market now offers returns worth tokenizing.