Coinbase, the largest US-based exchange, capped a tough first quarter with another test of investor confidence after the cryptocurrency exchange missed Wall Street estimates by reporting another quarterly loss and later suffered a service disruption due to an Amazon Web Services (AWS) outage.

The series was a stark reminder to investors of the company’s two competing stories. Coinbase remains heavily exposed to crypto trading cycles, which weakened in the first three months of the year as Bitcoin and other digital assets retreated from recent highs.

At the same time, the company is asking the market to value it less as a simple token exchange and more as the infrastructure layer for stablecoins, derivatives, prediction markets, and AI-powered payments.

The trading slowdown will impact first-quarter results

Coin base reported revenue of $1.41 billion for the quarter ended March 31, lower than Wall Street expectations of about $1.52 billion. The company posted a loss of $1.49 per share, versus earnings estimates, as weaker trading weighed on its largest revenue stream.

The company reported a net loss of $394.1 million, its second consecutive quarterly loss after a $667 million loss in the fourth quarter of 2025. A year earlier, Coinbase had posted a profit of $65.6 million.

The weakness was most evident in transaction revenue, which remains closely tied to clients’ trading activities. Coinbase generated $755.8 million in transaction revenue, below analyst estimates of about $805 million.

Consumer transaction revenue fell 23% from the previous quarter to $567 million, driven by a 35% decline in consumer spot trading volume. Institutional transaction revenues fell 27% to $136 million, while other transaction revenues fell 17% to $53 million.

The decline could be linked to a weaker quarter for the crypto markets. Facts from CoinGlass showed that Bitcoin ended the first quarter down more than 20%, reducing the kind of speculative activity that typically supports stock market revenues.

Notably, lower prices and reduced trading activity also put pressure on other crypto companies during the period, as traders moved away from riskier positions in digital assets.

Coinbase leans on the ‘everything exchange’

At X, CEO Brian Armstrong took advantage of the earnings call argue that the crypto infrastructure is entering a new phase.

He said the on-chain economy has reached “breakout velocity” and that Coinbase’s full-stack platform is positioned to capture the next wave of financial activity, including AI agents transacting with stablecoins.

In his argument, the company is already becoming more diversified, as evidenced by the fact that the subscription and services segment has become a larger part of its business, supported by stablecoins, staking, custody and other products less directly linked to daily trading volumes.

For context, the exchange’s stablecoin revenue was $305 million in the quarter, up from $274 million a year earlier. Coinbase said the increase was driven by growth in the market value of USDC and record average USDC balances in Coinbase products.

At the same time, the company said it has gained market share in both spot and derivatives trading globally, reaching an all-time high of 8.6% in crypto trading volume market share.

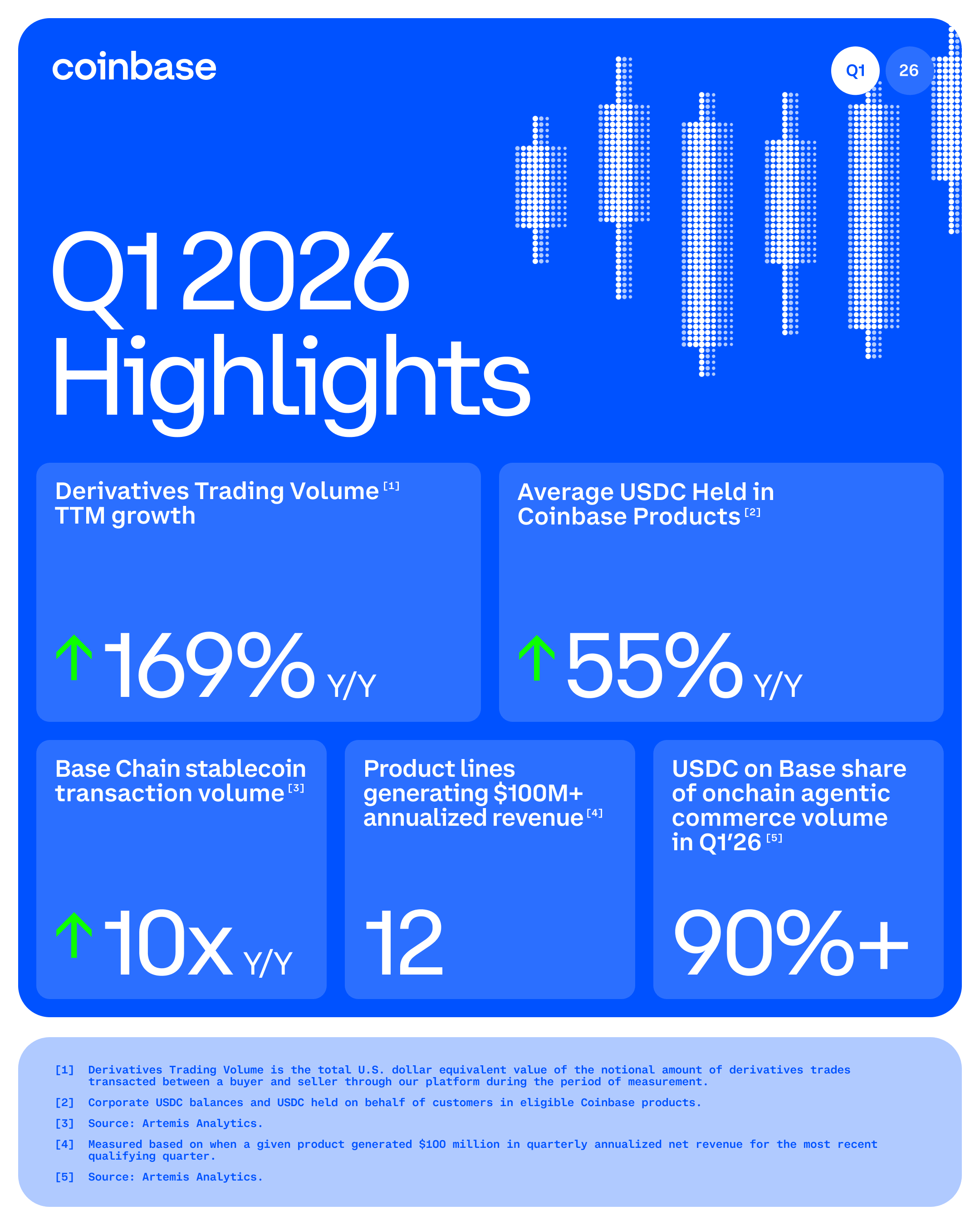

The company also recorded approximately $4.2 billion in derivatives trading volume in the first quarter, up 169% from the same period a year earlier.

That growth supports Armstrong’s “all exchange” plan, which aims to make Coinbase a platform not only for buying and selling Bitcoin, Ethereum and other tokens, but also for derivatives, real assets, prediction markets and eventually other forms of financial exposure.

Chief Financial Officer Alesia Haas argued that Coinbase’s underlying business remained strong to support this statement, while noting that the company has 12 product lines that generate more than $100 million in revenue annually.

This view was also confirmed by Armstrong, who added:

“Our thesis is simple: crypto is the best form of money, and the infrastructure will overhaul the existing financial system. When it comes to money, it will be about crypto. Coinbase is uniquely positioned to benefit from this transformation.”

Outage testing infrastructure pitch

That message was complicated by the service disruption that followed the earnings release.

Coin base said some users were unable to transact on Coinbase Exchange after AWS reported issues in the US-EAST-1 region.

The issue was related to elevated temperatures in a Northern Virginia data center, where a thermal event caused power loss and damaged hardware associated with EC2 instances and EBS volumes.

On X, Coinbase declared:

“Coinbase systems are designed to withstand an outage in one zone, and are designed to recover quickly if this happens. In this case, we observed outages affecting multiple AWS zones, causing a prolonged outage of key trading services. Coinbase users experienced a prolonged outage while the AWS team worked to restore temperature controls and other Amazon Managed Services.”

At the time of writing, the company said the primary issue had been fully resolved and all markets were trading again.

For a conventional exchange, a cloud-connected outage is a technical incident. For Coinbase, the timing created more consequences.

The company is trying to position itself as a core platform for trading, payments, stablecoins, derivatives, prediction markets and on-chain financial applications. A disruption lasting just hours after a revenue miss gave skeptics another reason to question whether the infrastructure can scale with its broader ambitions.

The issue also revived familiar concerns about crypto platforms’ dependence on centralized technology providers. Coinbase operates in an industry built around decentralization, but its retail and institutional access points still rely on conventional cloud infrastructure.

That in itself does not undermine Coinbase’s business. Major financial and technology companies rely on AWS and other cloud providers. But it gives investors another metric to watch as Coinbase expands into more markets where uptime, settlement reliability and institutional trust carry greater weight.

Bulls are eyeing a $300 billion scenario

Yet the most aggressive bull case now rests on Coinbase becoming a major platform for AI-native financing.

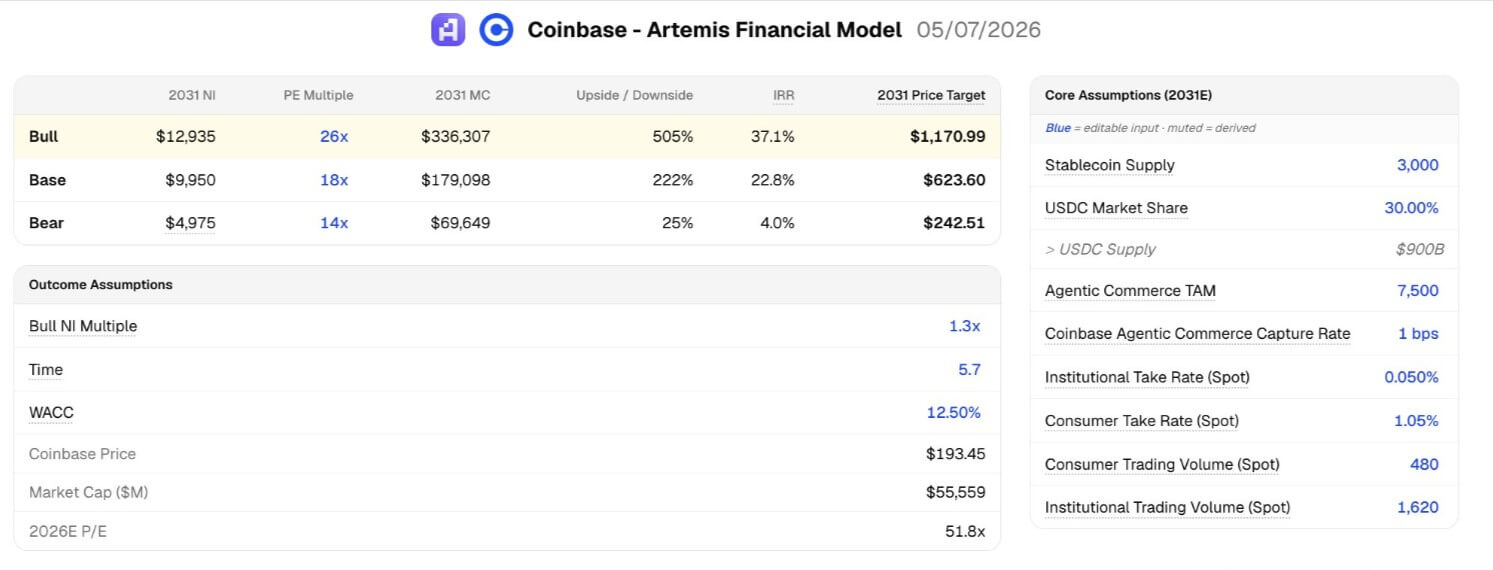

Blockchain analytics firm Artemis has argued that Coinbase could be worth more than $300 billion by 2031, about six times its current market value.

The projection depends on several assumptions: stablecoin supply reaches about $3 trillion, USDC captures 30% of that market, agentic commerce reaches $7.5 trillion in annual spending, and Coinbase captures one basis point of that activity.

The model also assumes that Coinbase’s net transaction revenue grows at a compound annual rate of 11% and that subscription and service revenue increases from approximately 40% of total revenue to 65% by 2031.

In that scenario, Coinbase would generate approximately $23 billion in revenue and $10 billion in net income by 2031.

That projection is far from guaranteed. It requires that stablecoins become a much larger part of global finance, that USDC maintain or expand its market position, that Base remains relevant, and that AI agents become meaningful economic actors rather than a speculative technology theme.

It also requires Coinbase to manage the risks exposed during the last quarter. Trading revenues still fell sharply as crypto prices weakened.

The company remained exposed to market cycles. Shares reacted negatively to the earnings miss. A cloud-related outage interrupted service at a time when the company was trying to emphasize reliability and scale.

Still, the quarter also showed why Coinbase remains difficult to value via a simple exchange multiple.

The company purchased $88 million worth of Bitcoin during the quarter, bringing its holdings to 16,492 BTC. It expanded stablecoin revenues, gained trading share, grew derivatives volume and continued to build new businesses that could be less tied to retail spot speculation over time.

Coinbase’s short-term story continues to be driven by crypto prices, trading appetite, and operational execution. The longer-term valuation depends on whether stablecoins, Base, derivatives, prediction markets and AI-driven trading can grow big enough to change the company’s earnings base.

The first quarter provided evidence for both sides. Bears saw lower earnings, another loss, weaker trading and an outage.

Bulls saw a company still adding users’ own units, expanding beyond spot markets and building a financial platform that could become much bigger if the next phase of crypto is driven by payments and automated trading rather than a new retail boom.