Bitcoin’s plunge to $60,000 last week highlighted how quickly a shift in investor appetite can turn into forced selling as leverage is rebuilt beneath the surface of the crypto market.

The largest cryptocurrency by market value fell nearly 14% last week, leading to nearly $10 billion in liquidations of long futures as traders who had bet on higher prices were driven out of the market.

Bitcoin later recovered to around $63,000, but the recovery did little to settle the debate over what caused one of the sharpest selloffs of the year.

Market commentary from Charles Schwab and NYDIG points to a broader explanation. Capital has begun to focus on artificial intelligence, private technology deals and other high-growth transactions, while Bitcoin futures positioning has become more crowded.

AI will become the rival trading to Bitcoin

Bitcoin’s latest weakness has unfolded as investors reassess where the strongest speculative returns come from.

In a note shared with CryptoSlateJim Ferraioli, head of crypto research and strategy at Charles Schwab, said crypto investors have repeatedly turned to the market’s dominant momentum trade.

That pattern has played out in precious metals, oil futures during the Iran conflict, memory stocks and private investment vehicles tied to future IPOs.

In recent months, artificial intelligence has taken on that role.

The scale of spending related to AI has attracted capital through publicly traded equities, data center infrastructure and private markets. For investors who once used Bitcoin as a primary way to express a view on fast-growing technology, AI has become a direct competitor for attention and liquidity.

Strategy executive chairman Michael Saylor pointed to that pressure last week after Bitcoin’s decline. He said about $400 billion had flowed into AI infrastructure over the past six months, while US-listed spot Bitcoin ETFs had seen about $4 billion in outflows since mid-May.

The contrast underscored the challenge Bitcoin faces. The top crypto no longer competes only with gold, other digital assets or macro transactions. It is measured against an AI cycle that has become the main growth story in the financial markets.

Greg Cipolaro, global head of research at NYDIG, also identified AI as one of the many forces weighing on Bitcoin and the broader crypto market.

His argument focused on the overlap between the two investor bases. According to him, both sectors are attractive to investors looking for exposure to emerging technologies, large markets and high return potential.

As AI-linked stocks have continued to outperform, capital has shifted to the stronger trades.

This shift is also visible in private markets. Investors are already positioning themselves for a potential wave of major tech listings, with companies like SpaceX, OpenAI and Anthropic seen as eventual public market contenders.

These large offers could prompt institutions to raise cash or reduce existing positions before taking on new allocations.

For Bitcoin, the result is weaker marginal demand at a tough point in the cycle. The network’s adoption story hasn’t broken down clearly, but the price action has softened as investors compare crypto to a technology trade that currently offers stronger momentum.

The leverage effect turns rotation into liquidation

Meanwhile, the pullback from Bitcoin became more severe as traders rebuilt risk in the derivatives markets before the sell-off began.

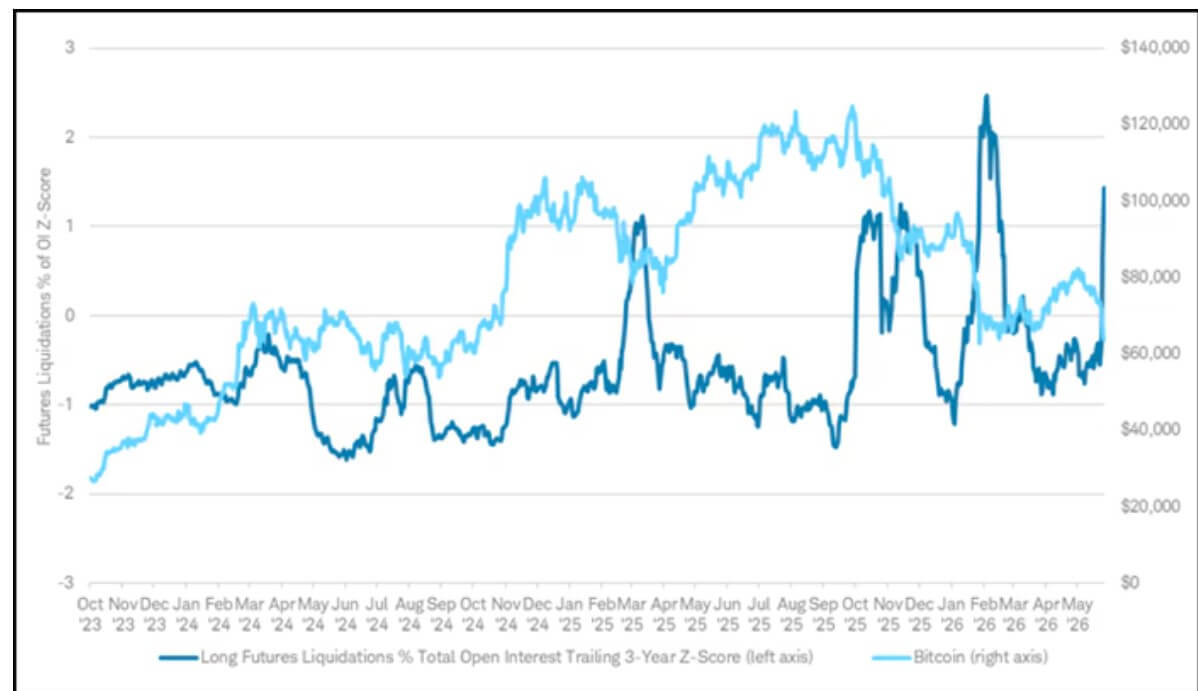

Ferraioli said the move reflected a market where debt burdens had returned, even if positioning was still below the excesses seen in previous periods. He noted that open interest on futures fell to about $31 billion in February, after hitting a high of about $70 billion. By May, the recovery had rebounded to about $51 billion.

That recovery showed that traders had turned back to leverage exposure as Bitcoin regained ground. Once the market fell, these positions became a source of pressure.

He said nearly $10 billion in long futures positions were liquidated last week as prices fell, forcing traders who had bet on further profits to close. The drop in open interest during the sell-off suggested that exposure was being removed from the market rather than being replaced with new positions.

Financing rates also returned to negative territory, showing that the long-term trend that had built up during the recovery was beginning to diminish. Ferraioli said liquidations relative to overall open interest indicated a moderate forced reduction in positioning.

That helped explain why Bitcoin’s decline accelerated. The rotation into AI-linked assets, ETF outflows and hedge fund sales weakened demand. Then, BTC traders’ derivative positioning increased the pressure once prices started moving lower.

In a leveraged market, selling can become automatic. Traders facing margin pressure are being forced out of their positions regardless of whether they still believe in the longer-term Bitcoin thesis. That process could drive prices down until enough exposure is freed up.

The shift also showed how quickly Bitcoin’s support structure was changing. ETF inflows and improving sentiment had helped the market earlier this year. By late May, these flows had weakened while futures exposure had increased.

Ferraioli noted that hedge funds were the main source of selling after Bitcoin peaked in early May. This decline was also in line with the decline in open interest on futures.

As of May 31, hedge funds had cut their stake in BlackRock’s iShares Bitcoin Trust, or IBIT, from about 29% to about 19%. Investment advisors went the other way, increasing exposure during the decline, while brokerage accounts also reduced investments.

The split highlighted a market where long-term allocators were willing to buy weakness, while more tactical investors moved to reduce risk as momentum faded.

A flush, no bottom yet

In light of the above, Ferraioli said the latest price action points to a market clearing leverage rather than adding a new wave of speculative exposure.

According to him, the market signals are going in the same direction. Open interest has decreased, the number of liquidations has increased and the financing interest has become negative.

Together, these moves suggest traders have been cutting back on long positions after positioning came under pressure during Bitcoin’s recovery from February levels.

That still leaves the market yet to reach a confirmed low, as forced liquidations can occur towards the end of a sell-off, but they can also occur in the middle of a broader decline. However, they do not prove that the selling pressure itself has been exhausted.

Ferraioli said liquidations should be viewed alongside open interest and financing rates. A more constructive approach would require that open interest rates no longer fall, that financing stabilizes and that forced sales disappear.

If debt levels rise again before spot market demand recovers, the market could remain exposed to a new round of pressure.

Meanwhile, some technical and cost-based levels suggest that BTC’s decline may be approaching a depletion zone.

Ferraioli noted that Bitcoin has returned to areas around the February lows, miners’ efficient production costs, and the 200-week moving average. Traders often watch these levels for signs that distress selling is slowing and longer-term buyers are emerging again.

The question is whether these levels of support can compete with the broader rotation towards AI and private technology. Bitcoin’s recovery to around $63,000 showed demand had returned after the liquidation wave, but weaker ETF flows and hedge fund selling continue to weigh on the market.

The next phase will depend on whether new capital returns to crypto. If AI-linked stocks, infrastructure deals and expected tech listings continue to pull the marginal dollar, Bitcoin may struggle to regain momentum even after a major debt reset.