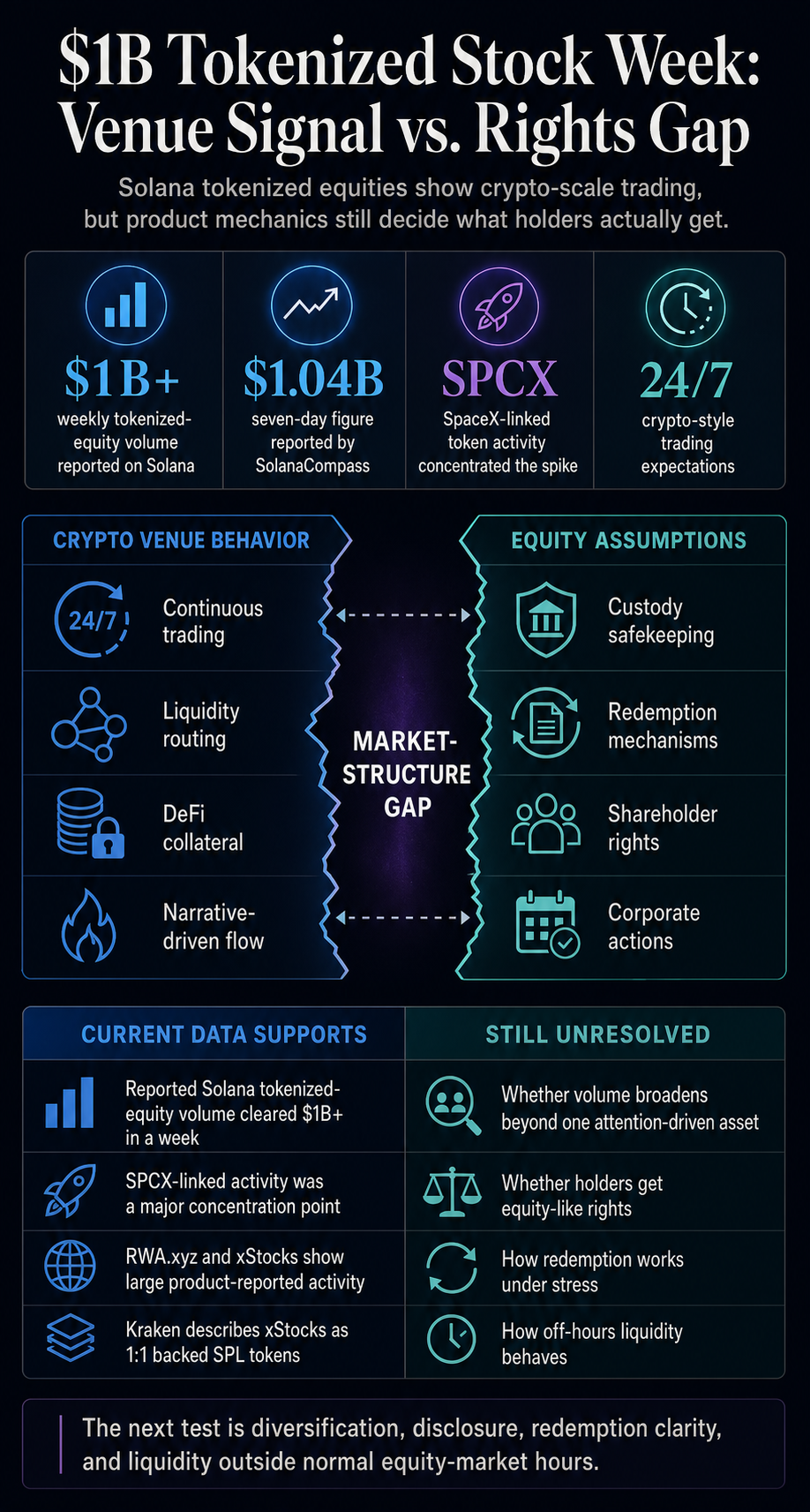

Solana tokenized shares have crossed a threshold: over $1 billion in reported weekly volume and a market that now acts like a live crypto venue.

Solana ecosystem messages said tokenized shares on the network cleared more than $1 billion in weekly volume as of June 20. This shows that equity-like tokens are now generating crypto-scale flows before their ownership, redemption, and liquidity assumptions are anything like public equities.

The shift extends beyond a single chain or token. Tokenized stocks are starting to act like a 24/7 crypto trading platform. Users can pursue exposure, liquidity providers can route flow, and platforms can market continuous access around assets still tied to off-chain companies, broker relationships, market hours, and legal terms.

Therein lies the risk, as trading centers around SpaceX-linked SPCX activity rather than a broad basket of tokenized stocks. SolanaCompass strongly linked the increase to SPCX, with the strongest support around the Backpack/SPCX concentration.

That may be an indication of demand, but it limits what even a total figure like $1 billion can say about the adoption of diversified tokenized stocks. One attention-intensive proxy for the private market can make a new location seem deeper than it is.

The location signal

The most obvious change is behavioral. Tokenized stocks have gone beyond the promise of allowing traditional assets to move on-chain. They look like instruments traded with crypto habits: rapid turnover, story-driven demand, routing between locations, and expectations of entry outside the normal rhythm of the stock market.

The tokenized shares of RWA.xyz dashboard and Solana Network dashboard provide the anchor for that shift. They exhibit sufficient activity to make the question of market structure unavoidable, while the origins of trade, product differences, and long-term sustainability remain unresolved.

Once an equity-linked token can trade at crypto-like speed, users can start to expect crypto-style entry and exit, even if the underlying reference asset follows a completely different rulebook.

The xStocks ecosystem reports total transaction volume of more than $25 billion across its tokenized equities network, and RWA.xyz platform data showed that Solana had hundreds of millions of dollars in xStocks distributed asset value as of June 25.

These numbers are product and dashboard data, the maturity of which is still unresolved. They are also large enough to make the category more difficult to dismiss as a demo market.

That’s the functional change behind the $1 billion week. A small or experimental RWA product may rely on education, disclaimers, and limited user expectations. A high-volume trading platform must be able to withstand users treating the instrument as something they can continually enter, exit, borrow against, and set a price on.

| What current data supports | Open restriction |

|---|---|

| Solana and SolanaCompass reported weekly volume of over $1 billion in tokenized equity. | The distribution across a broad basket of tokenized shares remains unresolved. |

| SPCX-linked activity was a major focus in the reported week. | SpaceX remains separate from the tokens; When trading on the secondary market, the status of the issuer remains unchanged. |

| RWA.xyz and xStocks data show high product reporting activity. | Each product still needs its own legal, economic and amortization analysis. |

| Kraken describes xStocks as 1:1 supported and issued as SPL tokens onchain. | Holders still need clear product-specific explanations about shareholder rights. |

SPCX turns the question into a concentration test

SPCX shows both sides of the market at the same time. The SpaceX-linked token gives traders access to a private company story that would otherwise be difficult for many crypto users to access.

That’s the demand side. It also focuses activity on a single asset that requires significant attention: the market structure problem.

CryptoSlate’s previous coverage of SPCX tokenized stock risk already showed why the details matter. A token tied to SpaceX exposure is a different instrument than SpaceX stock, and the practical outcome depends on how the product is issued, supported, redeemed, allocated and transferred.

That distinction becomes more important as volume increases, because more users are likely to view the instrument as stocks, even if the rights package differs.

There is also a problem with the quality of the location. Recent CryptoSlate coverage of Solana trade flow incentives framed the chain’s push for professional order flow as a test of whether liquidity will last once incentives and attention shift elsewhere.

Tokenized shares are now subject to the same test. A week dominated by one means of redress can prove that users will act. It leaves unanswered whether liquidity is broad and resilient, or can be easily redeemed under stress.

That difference is important for trading outside office hours. Crypto markets are constantly traded. Stock markets, corporate actions, broker-dealer processes, custody arrangements and transfer agent systems still move on different clocks.

If tokenized stocks are heavily traded while the underlying stock market is closed or while a benchmark asset in the private market has limited price movement, the token market can create its own expectations before the off-chain machines can meet them.

The same mismatch can be reflected in spreads, collateral rules and market maker behavior. If the token price moves while the reference market is closed, traders can treat the token as price discovery, while issuers and brokers still need traditional processes to handle backing, redemption, or corporate actions.

That is manageable if the volume is small. With more than $1 billion in reported weekly activity, it becomes a site-level design problem.

Rights and redemption determine what the volume means

The next phase of the tokenized stock market will be determined less by whether users want the products and more by whether users understand what they are buying.

Kraken’s support documentation says xShares are supported 1:1 by the underlying shares and issued as on-chain SPL tokens. That’s a meaningful product claim, and it’s different from pure synthetic exposure.

But the same category still requires careful language, as tokenized exposure can give users economic tracking, while ordinary shareholder rights, direct claims or simple redemption expectations remain dependent on product terms. CryptoSlate previously addressed the broader point in the context of crypto stock tokens and shareholder status.

The $1 billion week is both a disclosure test and a volume headline. If tokenized stocks start trading like crypto, users will need clear answers about who has the underlying exposure, what happens to dividends or corporate actions, who can redeem, how redemption works, which jurisdictions are eligible, and what happens if liquidity disappears outside of traditional market hours.

Once tokenized stocks are used as collateral, the question expands from whether a token can track a stock to whether lending markets, liquidation systems, oracles, and users can survive the mismatch between 24/7 crypto liquidation logic and stock market benchmark assets.

CryptoSlate’s reporting on tokenized stocks entering the DeFi collateral markets shows why this issue is quickly moving from product design to risk management.

For Solana, the opportunities are clear. The chain has become a platform where tokenized stocks can find visible volume, and the low-cost, high-throughput design fits the trading behavior these products invite.

The question is whether tokenized stock markets can support this activity once traders look beyond a single SpaceX-linked proxy and start asking stock-like questions.

The next signal is diversification. If volume expands across a larger set of tokenized stocks, if disclosures become standardized, and if redemption and custody mechanisms are easily understood before users trade, the $1 billion week will look like an early sign of a sustainable market structure.

If activity remains concentrated around one narrative asset, it will look more like a demand for a platform before the market agrees on what tokenized equity ownership should mean.