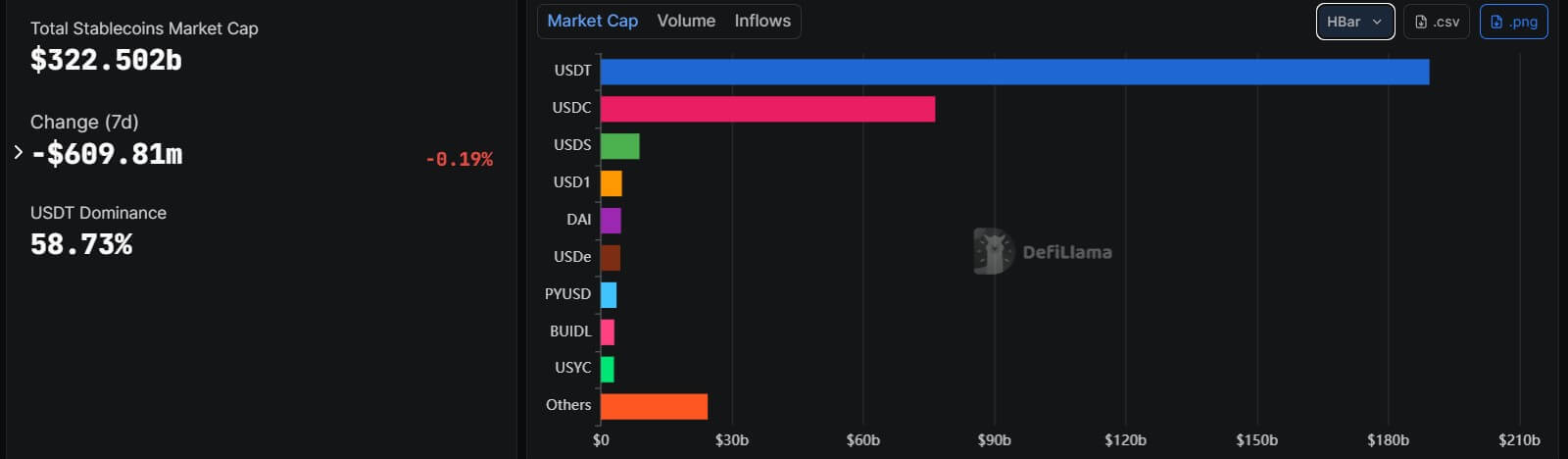

The global stablecoin market has climbed to a record $322 billion valuation, cementing the rise of digital dollars as one of the cryptocurrency sector’s most viable commercial products.

The milestone reflects an accelerating demand for real-time settlement, borderless cross-border transfers, and reliable dollar access on blockchain rails.

However, this expansion is also intensifying anxieties within the traditional banking sector, where these privately issued tokens are increasingly viewed as a direct threat to core deposits, payment relationships, and the legacy plumbing of global commerce.

As a result, the friction is driving a fundamental restructuring of digital finance. As stablecoin issuers expand under newly established federal frameworks, a parallel defensive-offensive is unfolding: global banks are quietly deploying tokenized deposit systems that already route trillions of dollars annually through blockchain-based infrastructure.

Stablecoin market moves deeper into finance

Over the years, stablecoins have evolved from a niche crypto-trading refuge into a settlement layer that threatens to disintermediate traditional banks.

While dollar-pegged tokens originally gained traction as a volatility hedge for digital asset traders, they are now gaining a foothold in global remittances, merchant settlements, and cross-border corporate flows.

Despite this commercial expansion, the market remains heavily top-heavy. Tether (USDT) and Circle (USDC) maintain a powerful duopoly, controlling more than 80% of the circulating supply, with USDT alone accounting for nearly 59%.

Meanwhile, a similar chokepoint exists at the network level, where Ethereum and Tron process the vast majority of outstanding token balances.

Yet that structural concentration is not deterring major traditional financial players from building on alternative, high-throughput rails to capture market share.

For context, Western Union recently launched USDPT, a US dollar-denominated payment stablecoin issued by Anchorage Digital Bank on the Solana network. Fully backed by bank deposits and short-dated Treasury bills, the token represents a deliberate push to route global money transfers through digital-asset infrastructure rather than legacy correspondent banking systems.

This pivot places Western Union alongside a growing cohort of payments companies, such as Payoneer, that treat stablecoins as essential commercial plumbing rather than speculative instruments.

For remittance firms and fintechs, the appeal is undeniable: blockchain rails offer round-the-clock settlement, bypass sluggish legacy intermediaries, and provide immediate dollar liquidity to markets struggling with unreliable local currencies.

This utility has transformed stablecoins into one of the most concrete commercial successes in the digital asset sector.

While the current market size remains a fraction of global commercial banking, aggressive forecasts project that stablecoin adoption could scale into a multitrillion-dollar sector by the end of the decade if fintechs fully integrate digital dollars into everyday financial flows.

Even at their current scale, hundreds of billions of dollars in tokenized balances are already large enough to influence US Treasury demand, dictate exchange liquidity, and force a defensive rethink across Wall Street.

As stablecoins move deeper into mainstream finance, their impact is no longer contained within the cryptocurrency ecosystem; they are now the center of a high-stakes policy fight over who will control the future of global digital money.

Regulation turns stablecoin growth into a bank threat

This rapid growth has revived a historic critique within economic policy circles: privately issued money expands aggressively during market upturns but risks triggering systemic crises if collective confidence fractures.

A recent Wall Street Journal analysis framed the stablecoin boom through this precise historical lens, warning that these tokens could replicate the vulnerabilities of 1800s-era “private money,” where unregulated issuers chased yield at the expense of depositor safety.

The underlying concern is that private issuers are inherently incentivized to maximize circulating supply and optimize reserve returns, potentially creating liquidity mismatches during periods of severe market contraction.

The digital asset sector is pushing back strongly against this characterization. Faryar Shirzad, Chief Policy Officer at Coinbase, points out that private money already underpins the modern US financial system, noting that commercial bank deposits and money market fund shares comprise roughly 90% of the M2 money supply.

From this perspective, the relevant regulatory question is not whether an asset is publicly or privately issued, but whether its structural guardrails accurately match its unique risk profile.

This argument has gained significant legal footing under the federal GENIUS Act framework. The legislation introduces a purpose-built architecture for payment stablecoins, while mandating strict reserve segregation, monthly independent attestations, and direct federal oversight.

The legislation also requires issuers to back circulating tokens 1:1 with exceptionally safe, liquid assets such as cash, short-dated US Treasuries, and Federal Reserve-eligible repurchase agreements.

This statutory framework has created a sharp operational divide between stablecoin issuers and commercial banks, with the latter allowed to accept deposits to extend credit, manage complex maturity transformations, use leverage, and generate fractional-reserve money.

On the other hand, the regulated stablecoin issuers function strictly as full-reserve transaction vehicles, prohibited from lending or leveraging reserve assets and structurally mitigating the “reach for yield” that historically triggered money-market disruptions.

Despite these legal separations, commercial banks view the expansion of stablecoins as an existential balance-sheet threat.

When an enterprise or retail client exchanges fiat currency for a third-party stablecoin, that liquidity is effectively drained from the traditional banking system.

This shifts the financial relationship from a heavily regulated deposit institution to a non-bank digital issuer, costing the bank access to vital payment data, transaction fees, and, most critically, low-cost funding.

As a result, Wall Street has increasingly mounted a direct technological counteroffensive against the emerging industry.

Banks build a $4 trillion on-chain counterweight

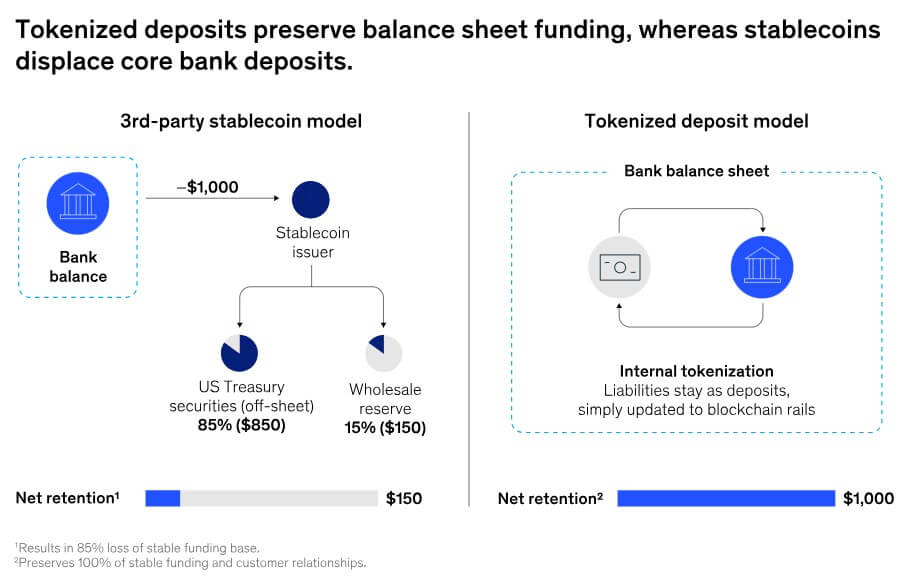

To protect their balance sheets from this nonbank disintermediation, traditional financial institutions are moving aggressively onto the blockchain with their own alternative: tokenized deposits.

A tokenized deposit updates the technical form factor of a traditional bank account by placing deposit liabilities directly onto blockchain rails.

Instead of a corporate treasury department offloading cash to a third-party crypto wrapper like USDT or USDC, the customer retains their deposit relationship with a regulated commercial bank.

The client captures the fundamental operational advantages of blockchain technology, such as smart-contract programmability, near-instant settlement finality, and automated reconciliation, while keeping their capital securely inside the established banking perimeter.

This structural architecture provides commercial banks with a powerful competitive advantage. Because tokenized deposits are simply traditional bank liabilities represented on a ledger, they automatically inherit existing legal, regulatory, and clearing frameworks.

Furthermore, they circumvent a major commercial limitation of stablecoins: while licensed stablecoin issuers are largely prohibited from paying yield to token holders under global regulatory frameworks, commercial banks can leverage their traditional fractional-reserve lending operations to pay competitive interest rates on tokenized balances.

While stablecoins dominate public media coverage, bank-led tokenization networks have quietly achieved an order-of-magnitude higher transaction volume.

Total stablecoin payment activity is estimated to reach $400 billion in 2025; by contrast, institutional tokenized deposit networks are currently on track to facilitate more than $4 trillion in annual transaction volume, McKinsey noted.

Much of this immense volume is driven by proprietary wall-garden infrastructure such as JPMorgan Chase’s Kinexys, which is estimated to process more than $1 trillion annually for internal corporate treasury movements, cross-border intercompany settlements, and wholesale liquidity positioning.

These massive financial flows occur deep within permissioned, institutional ledger environments rather than on public, retail-facing blockchains, making them less visible to the public but deeply disruptive to global corporate banking.

However, the primary vulnerability of the banking sector’s strategy is severe network fragmentation.

While stablecoins enjoy massive network effects due to their native interoperability across public blockchains, tokenized deposits are currently confined to closed, single-bank permissioned networks.

A tokenized dollar minted on one bank’s proprietary blockchain cannot naturally interact with a smart contract running on a competitor’s ledger, threatening to replace legacy correspondent banking friction with a new network of isolated digital islands.

Overcoming this obstacle requires extensive legal and operational coordination rather than purely technical fixes.

To achieve true interbank fungibility, international banking coalitions are actively testing shared orchestration networks and unified ledger initiatives, including the Bank for International Settlements’ Project Agorá, the Swift orchestration layer, Partior, and Chainlink’s CCIP.

Digital dollars move toward a layered system

The unfolding battle between crypto-native firms and Wall Street giants suggests that the future of digital money will not be dominated by a single token or platform.

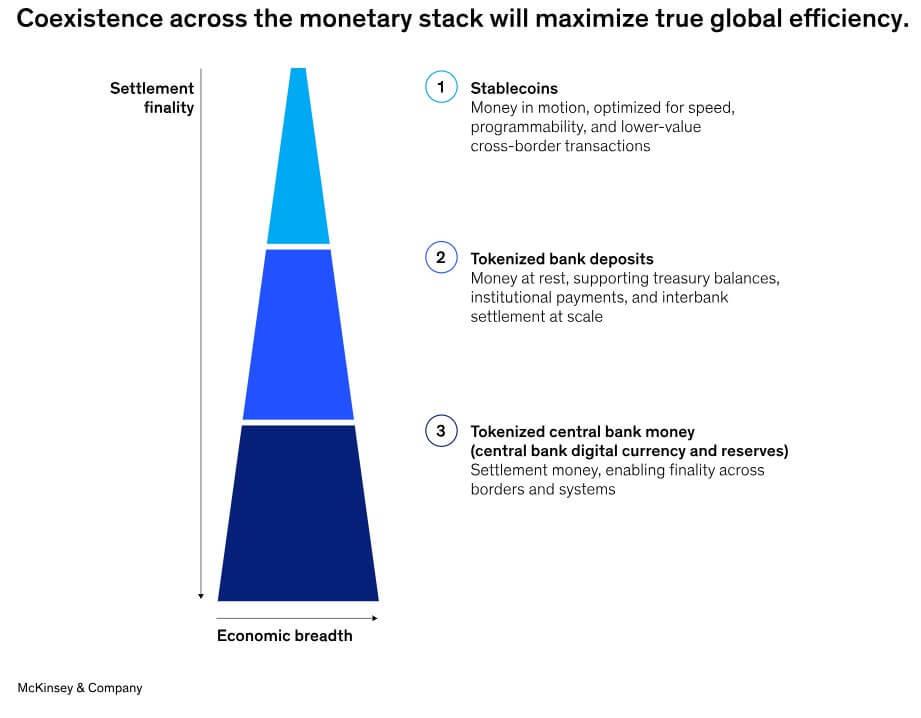

Instead, the global financial system is steadily organizing itself into a sophisticated, three-layer digital-dollar monetary stack, where distinct forms of tokenized value fulfill highly specialized economic roles:

- Stablecoins: “Money in Motion”

Positioned at the user-facing top layer of the stack, open-source stablecoins like USDC and USDT will likely maintain their dominance across public, permissionless networks.

Their deep exchange liquidity, borderless accessibility, and frictionless distribution make them the ideal instrument for retail digital asset trading, decentralized finance (DeFi) protocols, peer-to-peer global remittances, and cross-border commercial transactions in regions lacking stable local banking infrastructure.

- Tokenized Bank Deposits: “Money at Rest”

Occupying the institutional mid-layer, bank-led tokenized deposits are poised to become the default settlement asset for high-value corporate finance.

Because they preserve institutional bank balance sheets, offer regulatory alignment, permit interest accumulation, and integrate directly with legacy cash-management services, these instruments are structurally optimized for corporate treasury balances, wholesale enterprise payments, and large-scale commercial bank settlements.

- Tokenized Central Bank Money: “Settlement Money”

Forming the sovereign foundation of the entire system, wholesale central bank digital currencies (CBDCs) and tokenized central bank reserves will serve as the ultimate risk-mitigation layer.

Operating primarily behind the scenes, this sovereign asset will be used strictly to resolve imbalances and execute final, irrevocable settlements between disparate commercial bank networks, thereby eliminating institutional counterparty risk at the macro level.

Ultimately, the record-breaking $322 billion stablecoin market proves that the market demand for a modernized, real-time digital dollar is permanent.

At the same time, the $4 trillion scale of bank-led tokenization proves that traditional financial institutions have no intention of surrendering the future of payments to nonbank crypto enterprises.

As these ecosystems move toward inevitability, the definitive battleground will no longer be over the underlying technology itself, but over the regulatory perimeters, interoperability standards, and ultimate control of the customer relationship.