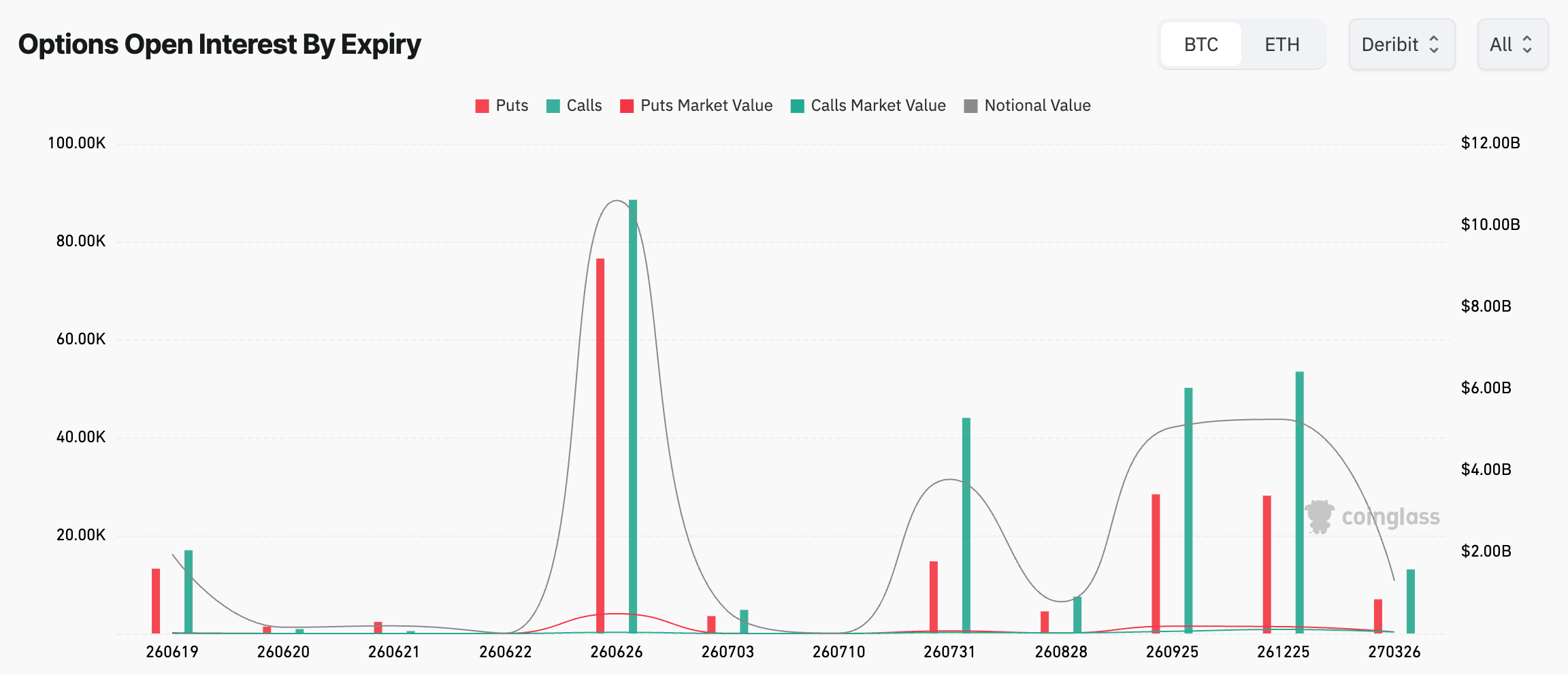

Bitcoin fell below $60,000 in mid-June after a tough start to the month, but the figure drawing the most attention on trading desks is the June 26 Bitcoin options expiration, with more than $10 billion worth of contracts set to expire and around 80% currently out of money.

On the stock markets, zero-day-to-expiry options now represent more than half of the daily supply S&P 500 index option volume, up from about 5% in 2020.

These two numbers come from very different corners of the financial world, but they describe the same underlying development: an options trading boom that has pushed contracts about what assets might do next into the most active part of modern markets, while ownership of those assets has come to play a supporting role.

The financial sector as we know it is evolving from an economy built on ownership to an economy built on ownership optionalwhere investors place an increasing premium on flexibility, asymmetric payouts and exposure to probability itself.

Options, perpetual futures, prediction contracts and tokenized derivatives are now the tools by which markets discover prices and route capital.

Crypto reached this point first, which is why the strongest evidence for options supremacy appears first in Bitcoin and Ethereum before emerging in traditional assets.

Is crypto the first market truly led by options?

The reason crypto came first in the options race comes down to the way these assets are valued.

Bitcoin doesn’t generate any income and Ethereum pays out anything resembling a conventional dividend, so their valuations rely almost exclusively on expectations about the future. In that environment, the derivatives market took over the work of price discovery.

By 2025, open interest in Bitcoin options had grown to rival and sometimes even exceed open interest in Bitcoin futures, a milestone that would have seemed strange just a few years earlier.

Most of that exposure is now in BlackRock’s IBIT options and Deribit, the venue that built the professional crypto options market. The expiration date at the end of 2025 was the largest on record, representing more than half of Deribit’s entire portfolio.

The market is wary of the size of this market because of the way options are reflected in spot prices. When traders buy and sell these contracts, the dealers on the other side hedge their exposure by trading the underlying assets, generating real buying and selling pressure.

Bitcoin remained stuck for weeks until the end of 2025 within narrow margins, when dealer positioning dips near one strike bought and sold rallies near another. We see the same process as we enter the June 26 quarterly expiration, with the maximum pain level near $74,000 well above the spot price of around $65,000.

Gamma effects amplify movements, large expirations change behavior around specific dates, and the derivatives market now sets the spot price rather than tracking it. IBIT’s $40 billion options book shows how big this market can become on regulated US exchanges.

Traditional markets develop the same characteristics. Volume in US listed options reached 15.2 billion contracts in 2025an increase of 26% from a year earlier, with an average daily notional value of approximately $4 trillion. Retail participation, which was modest just a few years ago, now accounts for more than 30% of contract volume and clusters heavily in short-term bets that offer cheap access to large potential upside.

Institutions rely on options to hedge everything from interest rate risk to equity exposure. Algorithmic strategies, which are typically formed by machine-generated predictions, require tools that express probability distributions, and options are just that. Each of these forces reinforces the other, and together they continue to pull activity toward optionality.

An economy that prices possible futures

We’ve seen the same pattern spread far beyond conventional derivatives. Prediction markets, which allow participants to purchase contracts that pay out based on real-world outcomes, saw one record $31.2 billion in trading volume in Maywith open interest from the industry approximately $1.3 billion.

In april, a federal appeals court ruled that the contracts for sporting events traded on the Kalshi stock exchange qualify as swaps under the Commodity Exchange Actthus confirming the CFTC’s jurisdiction over them and placing the prediction markets squarely in it the federal derivatives framework.

This classification reduces much of the distance between betting on an event and trading an option on it. Kalshi recently closed a $1 billion round led by Coatue at a Valuation of $22 billionwith a reported annualized trading volume of more than $170 billion, a sign that investors now view probability itself as an asset class worth owning.

The emerging tokenization market is also looking for options. Real-world tokenized assets, excluding stablecoins In May, the mark passed $32 billionroughly tripled in a year, and the broader market clears $300 billion once stablecoins are included.

The first wave of this technology symbolized money, and the second wave symbolized assets such as government bonds, which are now have more than $13 billion in the chain.

The third wave begins to directly tokenize optional capabilities, in the form of programmable derivatives that can trade tokenized stocks, commodities and credits 24 hours a day. Over time, the derivatives layer built on top of these assets could become larger than the assets below them.

All of this affects how everyone experiences markets. Institutions are now allocating through optionality because it improves capital efficiency, limits downside risk and makes hedging much easier, making ownership just one of many forms of exposure.

Retail investors, even those who never trade a single contract, find themselves in markets where price swings around major expirations and dealer positioning can outweigh fundamental news.

Some caution is needed here, as gross option volume is not the same as net dealer exposure, and much of the total RWA still reflects issuance rather than active secondary trading. However, the direction of travel is consistent across all these markets.

The defining financial innovation of the previous generation was the democratization of ownership through ETFs, online brokerages and digital assets that allowed almost anyone to own a piece of almost anything.

The defining innovation of the next generation looks like the democratization of exposure to probability, the ability to take a stance on what might happen without committing to what already exists.

Ownership has made modern finance possible, and the hunger for options shapes the chapter that follows, as the fastest growing thing investors buy becomes the right to be right about the future.