Franklin Templeton, the $1.78 trillion asset management firm, is trying to push cryptocurrency deeper into conventional investment portfolios with a new proposal that would automatically redirect stock dividends to Bitcoin exposure.

The asset manager filed a report on June 18 paperwork with the U.S. Securities and Exchange Commission (SEC) to launch two exchange-traded funds that would hold U.S. stocks while filtering corporate payouts on digital asset investments.

The proposed funds, the Franklin US Equity Bitcoin DRIP Index ETF and the Franklin US Innovation Bitcoin DRIP Index ETF, would combine one of Wall Street’s most established practices, dividend reinvestment, with exposure to the world’s largest cryptocurrency.

The structure would give investors a primary footing in major US stocks while using the income generated by those companies to slowly accumulate Bitcoin-linked assets. That design avoids the need for investors to make a direct allocation to crypto up front, but instead build the position over time through a rules-based mechanism.

This filing reflects how major financial institutions are looking beyond standard Bitcoin funds and into more complex portfolio products.

After the first wave of US spot Bitcoin ETFs solved the fundamental entry problem, issuers are now experimenting with strategies that package the assets into income, options and allocation frameworks familiar to financial advisors and brokerage investors.

Notably, Franklin is already active in the digital asset market through the Franklin Bitcoin ETF, which trades under the ticker EZBC. The fund has attracted about $330 million in cumulative net inflows and manages roughly $360 million in assets, giving the company a foothold in a category dominated by larger rivals.

The new filing suggests Franklin is looking for a more specialized job. Rather than just competing through a spot Bitcoin wrapper, the company is proposing a product that could appeal to investors who are comfortable with stock ETFs but less willing to buy Bitcoin directly.

Dividends are becoming the entry point for Bitcoin

The two proposed ETFs would function as passive index trackers built around VettaFi benchmarks.

The Franklin US Equity Bitcoin DRIP Index ETF would attempt to mirror the VettaFi US Large-Cap 500 Bitcoin DRIP Index. The stock portfolio would be linked to the 500 largest American companies based on market capitalization.

The Franklin US Innovation Bitcoin DRIP Index ETF would track the VettaFi US Innovation 100 Bitcoin DRIP Index and focus on the 100 largest non-financial companies listed on the Nasdaq Stock Market.

Both funds would invest at least 80% of their net assets in the securities that make up their respective indexes, and in Bitcoin-related instruments corresponding to the crypto allocation of each index. At launch, each index would start with a 95% allocation to stocks and a 5% allocation to Bitcoin.

The reinvestment mechanism is the defining feature. When the underlying stock pays regular or special dividends, these payouts are automatically reinvested in Bitcoin-related assets in the market open on the day after the dividend ex-date.

That makes corporate income the source of funding for cryptocurrency exposure. For investors, the goal is not simply Bitcoin price appreciation, but automated accumulation through the dividend stream of US companies.

Franklin has built limits into the design to prevent Bitcoin from overtaking the stock base. If the Bitcoin allocation has fallen above 5%, it will be reduced to 4.5% at each quarterly review. If the allocation remains at or below 5%, no downward adjustment will occur.

The indexes also include an emergency cap. If a sharp rally pushes Bitcoin exposure above 20% between scheduled assessments, the allocation would be reduced to 4.5% by the end of the second business day after the threshold is crossed.

Meanwhile, the equities portion has its own concentration limits. Individual shares are limited to 20%, while the combined weight of companies above 5% cannot exceed 40%. These rules are intended to prevent the funds from becoming too dependent on a small group of mega-cap stocks or on Bitcoin itself.

Franklin did not disclose the funds’ tickers, listing exchanges, fees or expense ratios. The prospectus also states that the securities cannot be sold until the registration statement becomes effective.

Franklin Advisory Services LLC would serve as investment manager, while Franklin Templeton Institutional LLC would serve as sub-adviser. The listed portfolio managers are Dina Ting, Hailey Harris, Joe Diederich and Basit Amin.

Franklin gives himself several routes to cryptocurrency exposure

The SEC filing gives Franklin flexibility in how the funds gain Bitcoin exposure.

The funds may use Bitcoin-backed exchange-traded products, including products sponsored by Franklin affiliates.

They may also invest through other investment companies that offer exposure to Bitcoin, futures contracts, options, certificates of ownership in Bitcoin, or investments held through a wholly owned subsidiary in the Cayman Islands.

That subsidiary is central to the tax architecture of the proposal. Each fund may invest up to 25% of total assets through a Cayman-based entity designed to help income or gains from certain Bitcoin-related investments qualify as “good income” under the US Internal Revenue Code.

Maintaining regulated investment company status is critical to the tax efficiency expected of ETF products. Franklin says it plans to limit investments in subsidiaries to stay within diversification requirements at the end of each quarter.

The structure also introduces vulnerability. The filing warns that future guidance from the Internal Revenue Service, congressional legislation or changes in tax treatment could disrupt the strategy.

If that happens, the funds may need to change their investment approach. In certain circumstances the board may approve a change in strategy or liquidation.

The tax part shows the complexity behind what seems like a simple, consumer-oriented idea. The headline pitch is easy to understand: stocks generate dividends, and the dividends increase exposure to Bitcoin.

The implementation requires a layered structure with ETPs, derivatives, index rules and offshore subsidiaries.

Risks follow Bitcoin in the package

Franklin’s prospectus makes it clear that placing Bitcoin in an equity ETF structure does not eliminate the asset’s volatility.

The filing describes Bitcoin as having a limited history compared to stocks, bonds and currency instruments. It also characterizes the digital asset market as highly speculative and warns that Bitcoin’s price could fall sharply due to regulatory changes, declining trust, technological failures, network disruptions, or competition from other digital assets.

The document also identifies concerns about market structure. Many digital asset trading platforms operate with less oversight than traditional stock exchanges, creating risks associated with manipulation, fraud, theft and limited recourse for investors.

The concentration of Bitcoin ownership is another well-known problem. A significant amount of Bitcoin is owned by a relatively small number of large holders, known as whales. Large sales or transfers by these investors could have an outsized effect on market prices.

Custody adds another layer of risk. Digital assets rely on private keys and specialized security systems, making them vulnerable to hacking, malware, operational failures and loss. Franklin also warns that the treatment of digital assets in bankruptcy may remain uncertain, adding to legal complexity if a custodian or service provider fails.

The funds would face further risks due to the tools used to track Bitcoin exposure. Spot Bitcoin ETPs are not registered under the Investment Company Act of 1940 and do not offer the same protections as traditional registered funds. Futures, options and swaps may result in leverage, counterparty exposure, tracking error and losses greater than the initial investment.

These revelations are important because the proposed products are designed to make Bitcoin more accessible to traditional investors. The familiar packaging does not change the underlying risk profile of the digital asset.

The Bitcoin ETF race is shifting from access to design

Franklin’s filing comes as the Bitcoin ETF market enters a more complicated phase, with issuers trying to build new products around an asset class that has quickly entered mainstream portfolios.

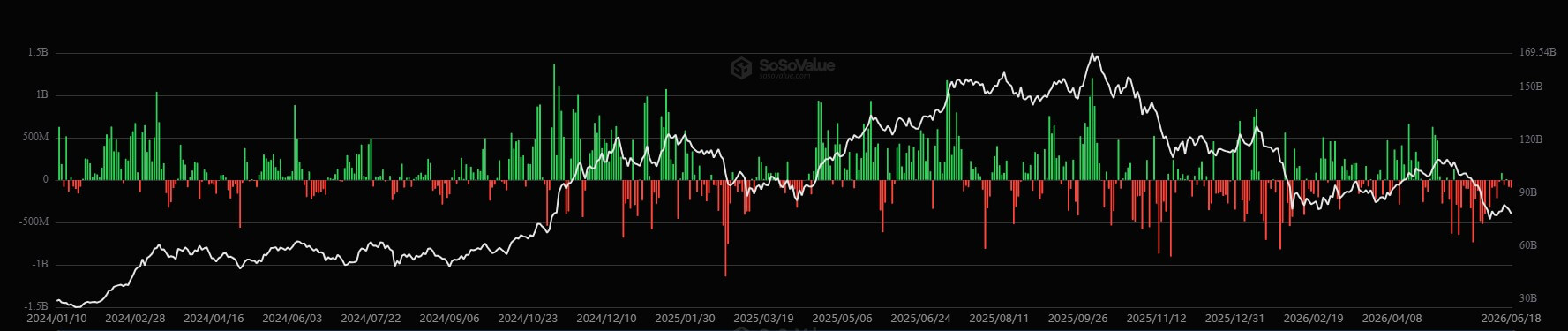

Since their launch in 2024, US spot Bitcoin ETFs have attracted $53.40 billion in net inflows since launch and hold $78.32 billion in assets, SoSoValue data shows.

These numbers reflect how quickly the products attracted Bitcoin into investment accounts, model portfolios, and institutional allocation strategies.

Still, the recent flow pattern has weakened. The funds have lost about $6 billion over the past six weeks during a period of sustained outflows.

That mix of scale and renewed pressure is pushing issuers beyond basic exposure. The first wave of Bitcoin ETFs gave investors regulated access to the assets. The next wave is focused on shaping how Bitcoin fits within broader portfolios.

BlackRock has already moved in that direction with the iShares Bitcoin Premium Income ETF, which trades under the ticker BITA. The actively managed fund seeks exposure to Bitcoin while generating monthly option premiums by writing call options on IBIT, BlackRock’s spot Bitcoin ETF, on approximately 25% to 35% of the portfolio.

That strategy is aimed at investors looking for cash flow from Bitcoin’s volatility, rather than just targeted exposure to its price. Franklin’s proposed DRIP funds would take a different route, using stock dividends to build a capped Bitcoin allocation over time.

Together, the products point to a new phase in the Bitcoin ETF market, where issuers are now competing to determine whether the asset belongs in income strategies, stock portfolios, accumulation products or other parts of traditional asset management.