On March 24, the Commodity Futures Trading Commission (CFTC) launched its Innovation Task Force, charged with developing frameworks for crypto assets, blockchain technologies, AI systems and prediction markets.

In addition to everything else Washington has done in the past three months, it reads like the moment when a provisional, enforcement-oriented stance toward crypto began to harden into something more permanent.

The asset class became too financially embedded, too politically controversial, and too legally entangled for the federal government to handle it on a case-by-case basis.

A timeline that speaks for itself

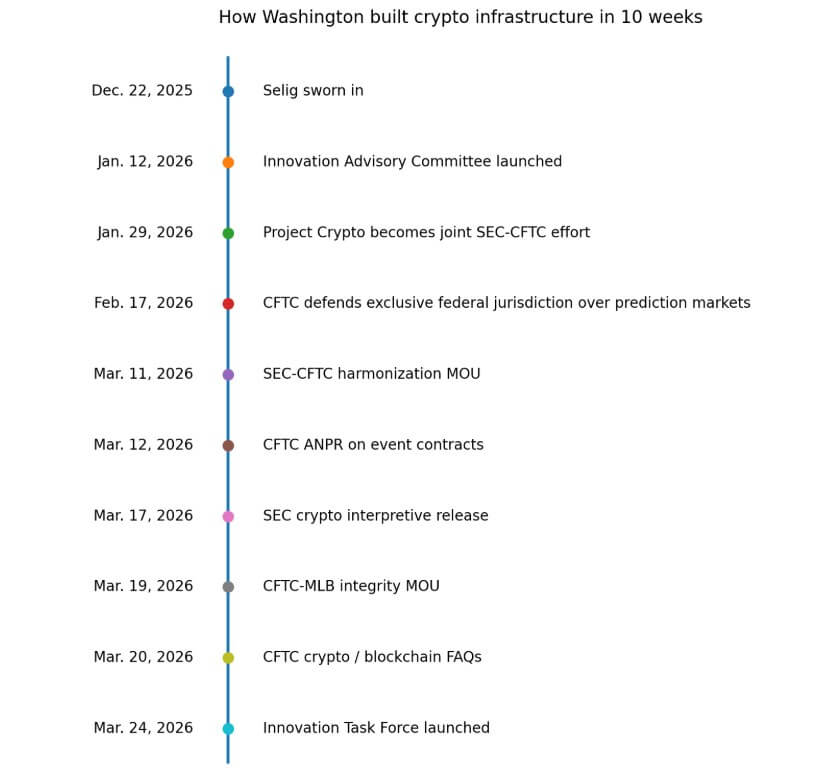

The pace since Chairman Michael Selig was sworn in in December 2025 is the clearest evidence available.

On January 12, the CFTC launched a 35-member Innovation Advisory Committee, including Coinbase, Uniswap, Ripple, Kraken, Gemini, Chainlink, Nasdaq, CME, Kalshi and Polymarket.

That grid reflects where crypto now sits: intertwined with the largest established exchanges and clearinghouses in the American market structure.

By January 29, Project Crypto had become a joint SEC-CFTC venture. On February 17, the CFTC filed to defend its exclusive federal jurisdiction over prediction markets against state challenges.

On March 11, the two agencies signed a harmonization MOU, establishing a public initiative in which staff coordinates to eliminate duplicative requirements, clarify jurisdictional boundaries and open streamlined pathways for new products.

On March 12, the CFTC opened an advance notice of proposed rules for event contracts.

On March 17, the SEC issued a crypto interpretation issue that formalizes a taxonomy covering digital commodities, digital collectibles, digital tools, stablecoins, and digital securities, explicitly treating them as a bridge as Congress continues to work on market structure legislation.

On March 19, the CFTC signed a unique MOU with Major League Baseball to coordinate the integrity of prediction markets. On March 20, the staff published frequently asked questions about crypto and blockchain. The task force started on March 24.

Scheme per institution

Advisory committees, formal MOUs, harmonization portals requesting written input from industry, joint interpretive publications, regulatory documents, and dedicated task forces leave a lasting infrastructure.

The CFTC now has them all, and the SEC operates in parallel. The Harmonization Initiative is an operational channel through which companies can request joint meetings and submit written input for staff review.

The SEC’s March 17 interpretation draws explicit taxonomic lines, determining which products fall under securities law, which fall under commodity law, and which occupy a newly defined middle ground.

The CFTC’s decision not to take action against Phantom, a provider of self-custody wallets, signals that regulators are now rethinking how on-chain software interacts with registered derivatives markets.

Congress has not created comprehensive market structure legislation.

Talks in the Senate reached an impasse in early March and the Banking Committee did not approve a bill. Meanwhile, agencies are putting together a de facto operating system based on the tools at their disposal: interpretations, staff guidance, MOUs, regulatory notices, and ongoing interagency processes.

These form the basis of a scaffolding that is more difficult to dismantle than a single guideline.

| Tool | Recent example | Why it matters |

|---|---|---|

| Advisory committee | Innovation Advisory Committee was launched on January 12 with 35 members from crypto companies, exchanges and market infrastructure groups | Creates a permanent channel for industry input and signals that crypto is treated as a permanent policy area rather than a one-off enforcement issue |

| Interagency agreement | SEC-CFTC harmonization MOU signed on March 11 | Builds a formal process for reducing duplication of requirements, coordinating personnel, and clarifying jurisdictional boundaries |

| Harmonization portal | Public SEC-CFTC initiative that allows companies to request joint meetings and submit written input | Turns coordination into an operational process that companies can actually use, not just a press release |

| Interpretive guidance | SEC crypto interpretive release on March 17 | Draws taxonomic lines through digital commodities, digital securities, stablecoins, collectibles, and other crypto assets, shaping how products are classified under federal law |

| Guidance for staff | Frequently asked questions about CFTC crypto and blockchain published on March 20 | Provides practical guidance to help companies navigate live compliance questions, even without a full statute |

| Staff assistance / no action | CFTC no-action position involving Phantom | Shows that regulators are now concerned with how self-custodial wallets and on-chain software connect to registered derivatives markets |

| Regulatory role | CFTC ANPR on event contracts opened March 12 | Moves prediction markets from ad hoc treatment to formal regulation with notice and comment |

| Jurisdictional claim | CFTC filing defending exclusive federal jurisdiction over prediction markets on February 17 | Signals that the agency is actively seeking to define and defend the limits of federal authority in a rapidly growing market |

| Integrity partnership | CFTC-MLB MOU signed on March 19 | It shows that prediction markets have become mainstream enough to involve oversight of the integrity of sports leagues and broader public scrutiny |

| Dedicated task force | Innovation Task Force launched on March 24 | Allocates permanent staff capacity to crypto, blockchain, AI and prediction markets, making it harder to expand regulation |

Where crypto no longer seems abstract

In prediction markets, it becomes impossible to treat the regulatory reckoning as a niche technical debate.

Since the 2024 US election, the sector has grown rapidly, winning contracts related to sports results, political events and economic data.

The CFTC, ANPR, and MLB integrity MOU’s exclusive jurisdiction filings reveal one agency trying to maintain the perimeter of a rapidly growing market.

On March 24, Senators Adam Schiff and John Curtis introduced the bipartisan Prediction Markets are Gambling Act, targeting sports contracts on prediction market platforms.

The bill’s existence confirms the political pressure: Washington is debating what federal attention the prediction markets deserve.

Those same pressures apply to crypto more broadly, as the industry now has to deal with derivatives sheds, tokenized collateral, wallet access to regulated venues, sports integrity monitoring, election forecasting, and jurisdictional boundaries between the federal states.

At that scale, ad hoc regulation becomes untenable as the complexity of the asset class outgrows the tools designed to monitor it remotely.

The infrastructure survives the moment

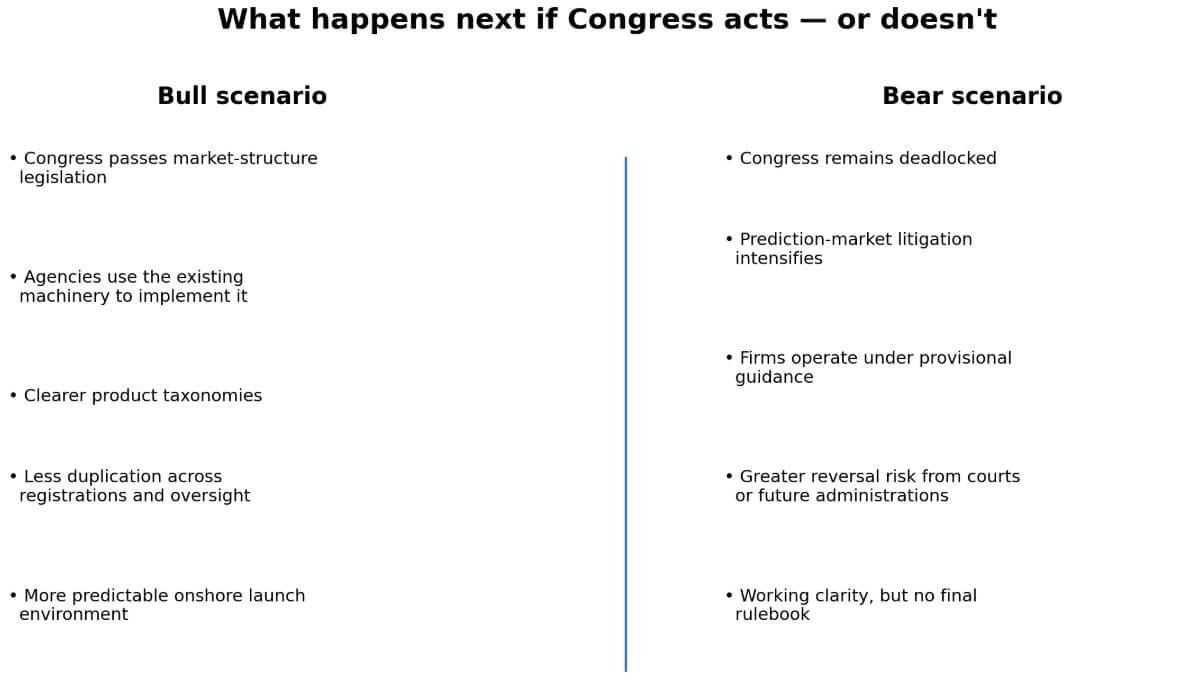

In the bull scenario, Congress ultimately passes market structure legislation, and agencies use existing harmonization machinery to implement it efficiently.

The task force, the MOU, the interpretive releases, and the advisory committee become the scaffolding for a cleaner, more sustainable US crypto framework. The new structure reduces duplicate registrations, provides clearer product taxonomies and creates a more predictable onshore launch environment for new financial products.

In the bear scenario, Congress remains deadlocked, litigation over the prediction markets intensifies, and guidance from the SEC and CFTC is still partially provisional.

Companies operate under a working clarity that is not sufficient to serve as a definitive rulebook. The machinery Washington has built runs on interpretive authority, making it more vulnerable to undoing by future administrations or adverse judicial decisions.

Neither scenario changes the observation that federal agencies are reorganizing around crypto, regardless of what Congress does next. The structures that have been built up in recent weeks do not disappear if a regulation stalls or a bill is not voted on by committee.

Crypto’s growing presence in Washington is measured by the formation of committees, the signing of interagency agreements, the opening of regulatory documents, and the deployment of staff to work on nothing else.

This is what it looks like when a financial market goes from a recurring compliance problem to a permanent part of the regulatory landscape.