Bitcoin’s break below $80,000 has pushed traders toward a crowded leverage zone, where a further decline could force around $1 billion in long positions out of the market.

According to CryptoSlate Data shows the largest cryptocurrency fell to $78,725 after US inflation figures came in higher than expected, weakening expectations that the Federal Reserve could cut interest rates later this year.

At the time of writing, Bitcoin has recovered to $79,500, down about 2% on the day and about 37% below October’s high above $126,000.

This price performance leaves Bitcoin sandwiched between two closely watched liquidation levels. CoinGlass data from May 14 shows that an estimated $1 billion in long positions on major exchanges could be liquidated if Bitcoin falls below $78,000. A recovery to around $80,458 would put around $640 million in short positions at risk.

That narrow range has become the market’s immediate battleground after inflation data interrupted Bitcoin’s recovery from April’s lows.

Notably, the current sell-off also coincides with softer US demand signals, an outflow from Bitcoin exchange-traded funds and renewed profit-taking by investors whose investments have regained value during the rally.

Leverage builds up around $78,000

In a note shared with CryptoSlateCryptoQuant noted that BTC’s rally above $80,000 was driven by speculative demand.

As a result, the $78,000 level is now more heavily weighted as leveraged long positions are concentrated below it.

This concentration level indicates where forced selling or buying may intensify if the price reaches that threshold. A large cluster means the market could move faster once that zone is hit, as exchanges close positions that no longer meet margin requirements.

Coinglass’ liquidation chart shows the greater immediate downside risk. If Bitcoin falls below $78,000, forced closures of long positions could increase selling pressure, while spot market demand is already weakening.

That could turn an ordinary downturn into a sharper move to deleverage.

Meanwhile, the upside risk is smaller, but still relevant. A move back to $80,458 would put pressure on roughly $640 million in short positions, raising the possibility of forced buying if bears are caught leaning too heavily on the inflation-driven decline.

That tension leaves Bitcoin in a compressed range. A lower decline would test whether the April recovery had sufficient market demand behind it. A recovery above $80,000 would show that the inflation shock has not completely reversed the recovery.

Find out that Bitcoin demand decreases as ETF outflows increase

Meanwhile, the Bitcoin derivatives setup is becoming increasingly vulnerable as recent signals in the spot market have weakened.

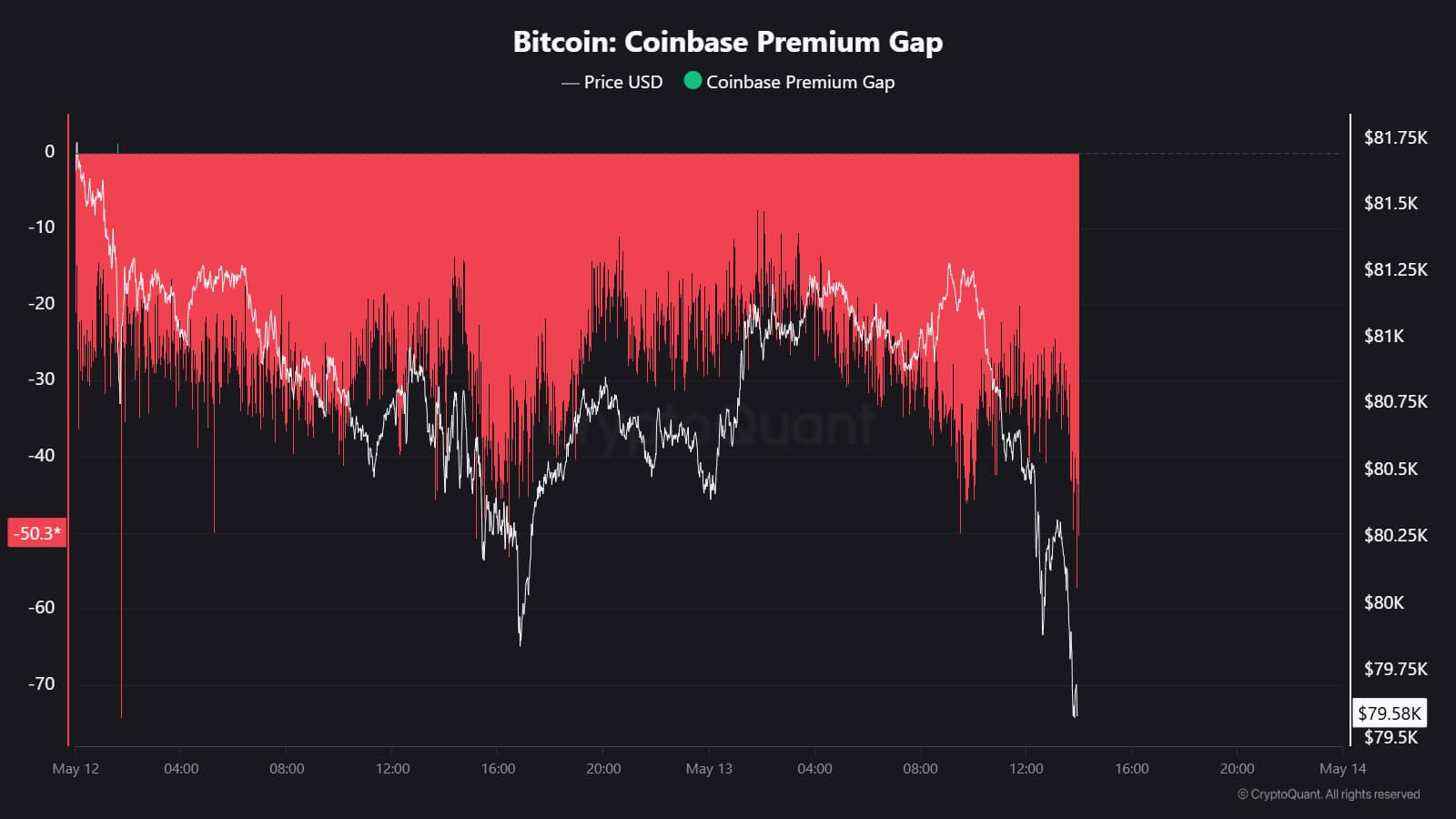

According to data from CryptoQuant, the Coinbase Bitcoin Premium Index has been declining since late April. The index tracks the price difference between Coinbase and Binance and is often used as a benchmark for US demand.

A persistent negative reading suggests that buying pressure from US-linked investors has waned as Bitcoin nears $80,000.

In this case, CryptoQuant analyst JA Maarturn explained that the signal means that “US institutional (major players) [are] Sell Bitcoin.”

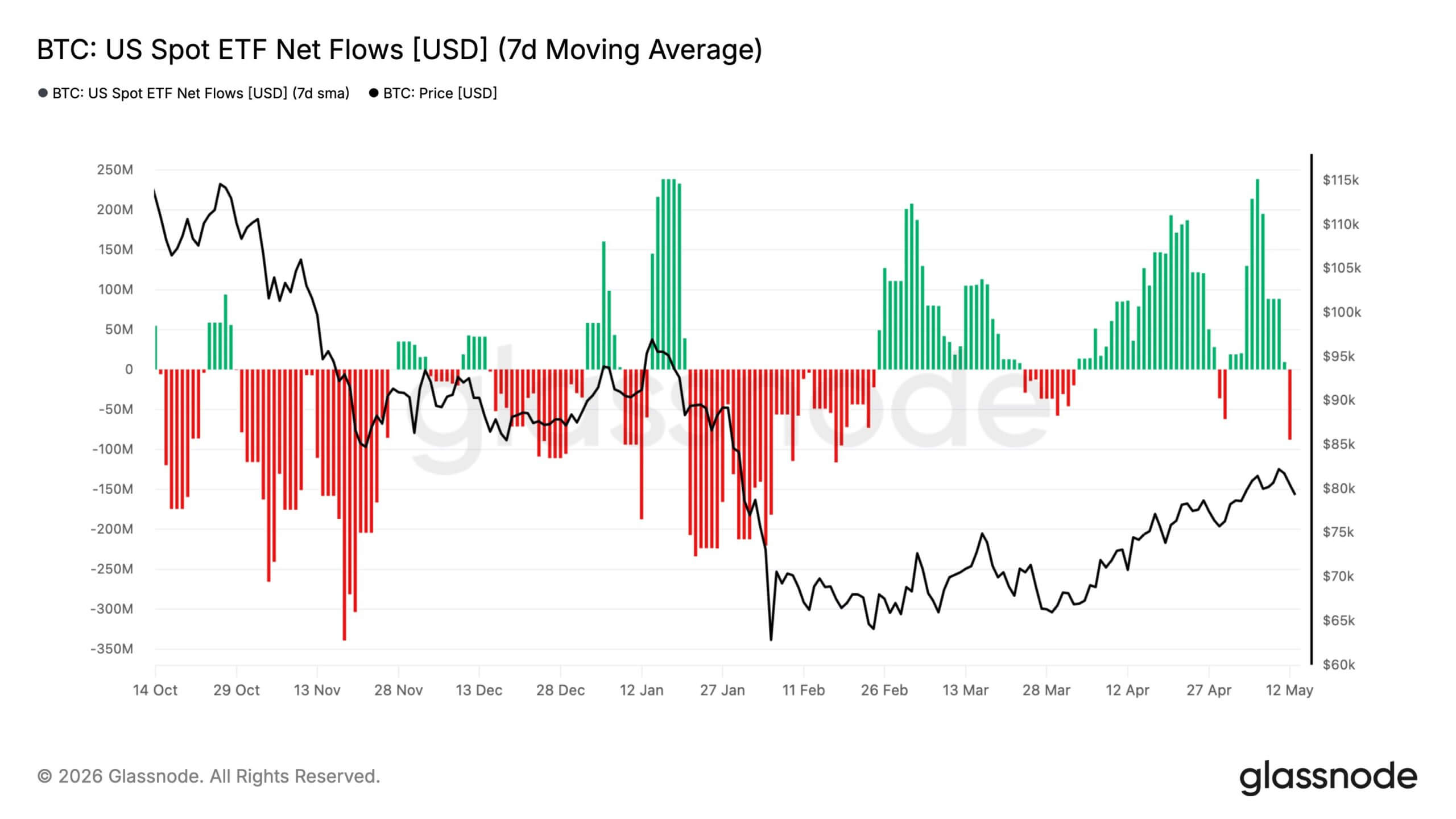

This is borne out by ETF flows, which have also become less supportive this week with outflows of over $800 million.

Facts from SoSoValue shows that the poor performance was mainly driven by the net outflow of $630.38 million on May 13. This was the second consecutive day of recordings and the largest single-day outflow in three months.

Additional data from Glassnode also shows that the seven-day moving average of net inflows into US spot ETFs fell to -$88 million per day, the largest outflows since mid-February.

Market analysts noted that these flows indicated that some institutional investors were using BTC’s recovery from $80,000 to reduce exposure rather than increase risk.

The picture is not one-sided, however, as spot Bitcoin ETFs still had net inflows of more than $400 million year to date, a sign that investor interest has not waned.

However, the recent turnaround shows that demand has become more selective as the rally faces macro pressures and technical resistance.

The 200-day average will be the upside test

Against this backdrop, Bitcoin’s immediate downside test is $78,000, the early May low that preceded the rally towards $82,000. A break below that level would bring the liquidation cluster into play and increase the risk of a move towards the capitulation zone at the end of April.

Still, BTC’s primary resistance level is near $82,400, the 200-day moving average. Data from CryptoQuant shows that Bitcoin reached that level after rallying 37% from the April low.

The setup is similar in one respect to that of March 2022: Bitcoin then rose about 43% before reaching its 200-day moving average and later resumed its decline.

According to the company, a clear break above $82,400 would ease pressure on bulls and force short sellers to reconsider their positions.

However, a failure near that zone would reinforce the view that Bitcoin’s recovery is encountering resistance just as ETF profit-taking and outflows increase.

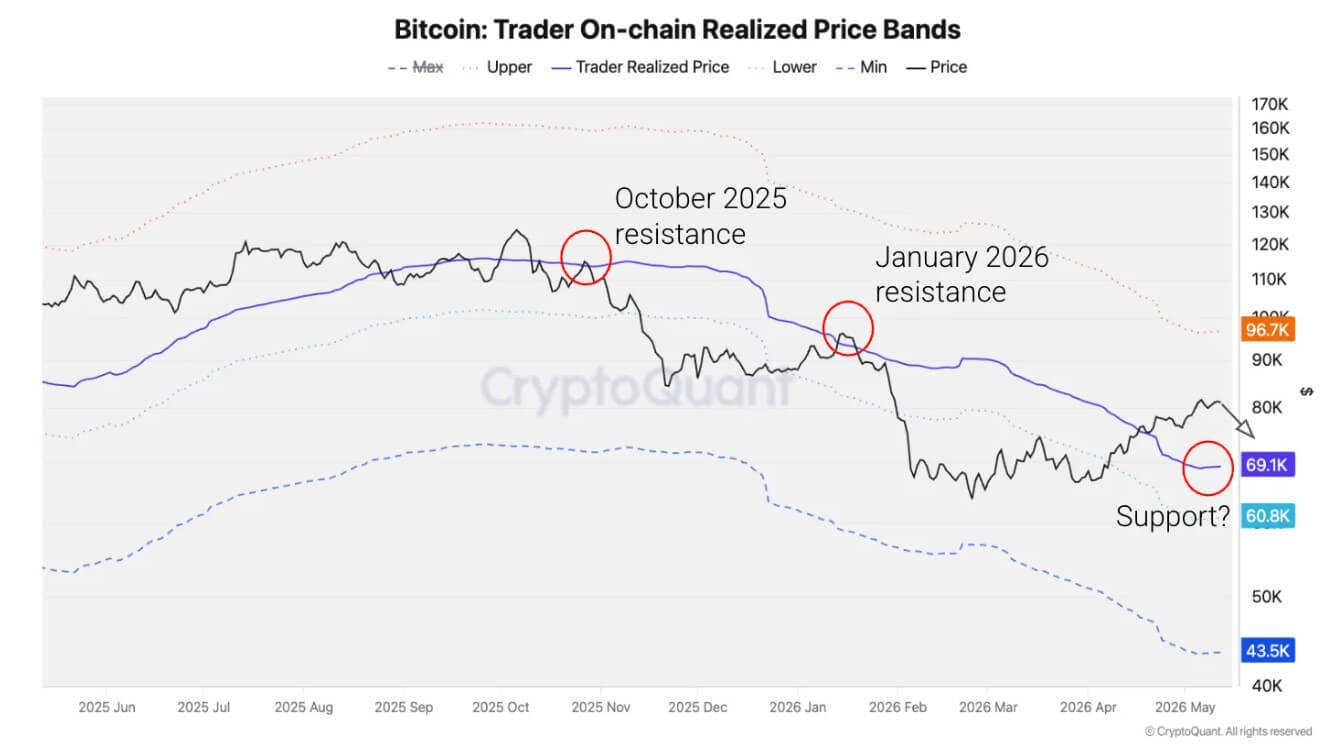

If Bitcoin falls below $78,000, the next major on-chain support will be closer to $70,000, which would be close to the on-chain price realized by traders.

That level represents the average cost basis of short-term traders and has historically acted as a support band when unrealized gains fall back toward zero.