Cumulative net inflows into US-traded spot Bitcoin ETFs have reached approximately $59.7 billion, with BlackRock’s IBIT alone holding $66.7 billion in assets.

Morgan Stanley and Charles Schwab are now pushing direct crypto trading to mainstream brokerage accounts. The motivation is that both companies can already see demand within their own customer base, while customers transact elsewhere.

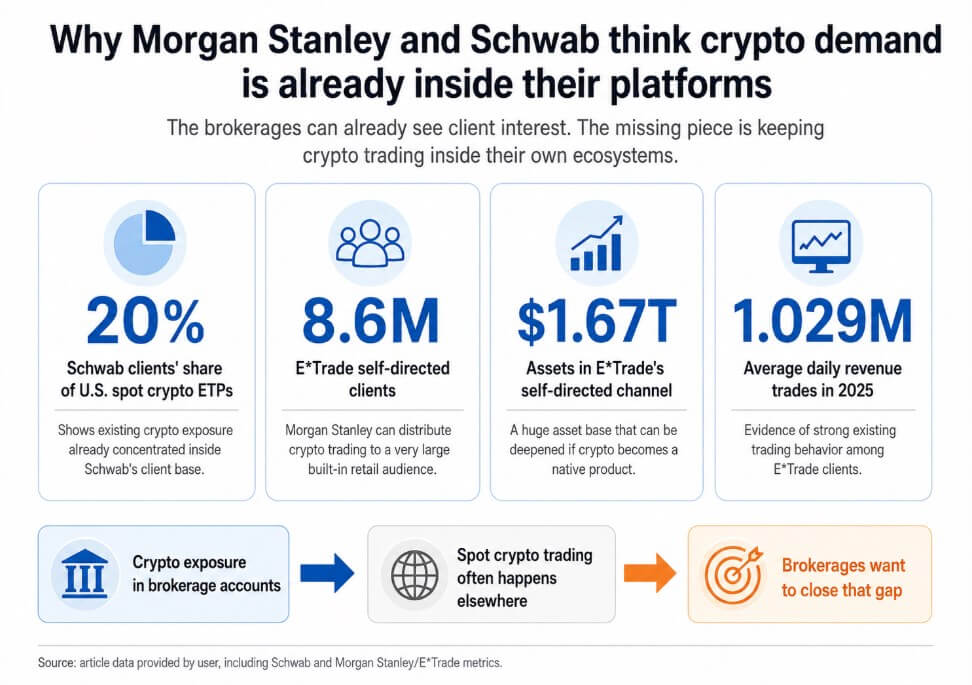

Charles Schwab’s clients own about 20% of US spot crypto-listed products, which helps explain the timing. Demand is already concentrated within Schwab’s franchise, and every trade these customers make on Coinbase or Robinhood is revenue and behavioral data leaving the brokerage.

Morgan Stanley faces the same math as E*Trade’s 8.6 million self-directed customers, who generated 1.029 million average daily sales transactions in 2025 across a channel with $1.67 trillion in assets.

The ETF era created a specific problem for both companies, as the products gave clients Bitcoin exposure within known accounts, while spot trading, execution, and account stickiness went elsewhere.

A Schwab customer who owns IBIT and then trades Bitcoin on Coinbase is splitting his financial life in half. Schwab will have assets under management and Coinbase will have the trading relationship.

Why attack now?

Both companies chose to move while the pure crypto model is under threat.

Robinhood’s first-quarter results show app crypto notional volume fell 48% year over year to $24 billion, while crypto revenue fell 47%.

The infrastructure costs of building a crypto product are fixed regardless of market conditions, but hitting a lull gives compliance, pricing, and service teams time to resolve the friction before retail enthusiasm returns in a big way.

Established players rarely attack pure-play competitors at the height of a cycle and move when the window is open.

The regulatory environment gave them the runway to build. The FDIC in March 2025 repealed the pre-approval requirement for permitted crypto activities, while the OCC clarified in May 2025 that national banks may buy and sell customer-held cryptocurrencies and outsource their execution with proper risk management.

In April 2026, SEC staff followed up with an interim statement regarding broker-dealer registration issues for certain crypto interfaces.

The change in direction created enough friction to arise, even though Congress has work to do on the CLARITY Act.

What looks like an aggressive push for 2026 is the visible end of a multi-quarter infrastructure project. Morgan Stanley’s E*Trade crypto plan began in September 2025 and targeted a launch in the first half of 2026 via Zerohash.

| Date | Event | Why it mattered |

|---|---|---|

| March 2025 | The FDIC has rescinded the pre-approval requirement for permitted crypto activities | Lowered an important procedural barrier for banks exploring crypto services |

| May 2025 | OCC clarified that national banks can buy and sell customer-held cryptocurrencies and outsource their execution with proper risk management | Gave banks a clearer legal-operational basis to build crypto products |

| July 2025 | Standard Chartered launched institutional spot trading in Bitcoin and Ethereum | It showed that major financial institutions were moving from the wrapper to direct trading |

| September 2025 | Morgan Stanley’s E*Trade crypto plan kicked off, targeting a launch in the first half of 2026 via Zerohash | Indicates that the 2026 push was planned well in advance, and not a sudden reaction |

| December 2025 | JPMorgan began exploring institutional crypto trading | Reinforces the broader industry shift towards building out crypto infrastructure |

| February 2026 | Fidelity received OCC approval for the custody and execution of cryptocurrencies by banks | Evidence has been added that regulated financial firms were building integrated crypto rails |

| April 2026 | SEC staff has issued an interim statement regarding registration issues between brokers and dealers for certain crypto interfaces | Added more regulatory clarity for brokerage-style crypto access |

| Rollout 2026 | Schwab launched with custody at Charles Schwab Premier Bank, execution via Paxos, educational tools and phased access starting with Bitcoin and Ethereum | Shows a full rollout focused on mainstream brokerage integration |

Schwab arrived with a full institutional stack, including custody at Charles Schwab Premier Bank, execution through Paxos, educational tools, and a phased rollout starting with Bitcoin and Ethereum.

The pattern extends beyond two brokerage firms, as Standard Chartered launched institutional spot trading in Bitcoin and Ethereum in July 2025, and Goldman Sachs filed for its first Bitcoin ETF in April 2026.

JPMorgan began exploring institutional crypto trading in December 2025, and Fidelity received approval from the OCC for bank custody and execution of crypto in February 2026.

Across these individual decisions, the shared conclusion is that the custody, execution, and access of cryptocurrencies should be part of the same infrastructure that handles every other asset class.

What decides the battle

If ETF inflows continue to recover, as Bitcoin ETFs recorded inflows of over $1.6 billion in May, and brokerage clients begin to treat crypto as a routine item alongside stocks, both firms are collecting trading revenue while deepening the client relationship.

Schwab has said it plans to expand beyond Bitcoin and Ethereum and will add transfer capabilities over time. Citi’s 12-month Bitcoin target sits at $112,000with a bull case of $165,000.

A direct access brokerage is already capturing demand as it broadens.

The bear case is that Schwab’s launch will be limited to just Bitcoin and Ethereum, with transfers delayed and unavailable in New York and Louisiana.

If Congress fails to enforce the CLARITY Act, the Fed remains restrictive, and retail involvement remains limited, direct cryptocurrency trading will become a table-stakes function.

Citi’s bear case values Bitcoin at $58,000, and Standard Chartered has indicated a potential drop to $50,000, and Bitcoin is already down about 7% year to date.

In that environment, the product retains existing crypto-interested customers and adds little new account growth.

| Scenario | Market conditions | BTC reference level | What it means for Schwab and Morgan Stanley |

|---|---|---|---|

| Demand is increasing / upside potential | ETF inflows continue to recover, brokerage clients are starting to view crypto as a routine commodity, and platform features are expanding over time | Citi 12-month target: $112,000; Citi bull case: $165,000 | Instant crypto trading becomes a meaningful tool for income and retention; brokers are capturing more trading activity within their own ecosystems |

| Muted adoption/downside case | CLARITY The law is stalling, the Fed remains restrictive, transfers remain limited, and retail involvement remains limited | Citi beer case: $58,000; Standard chartered disadvantage: $50,000 | Crypto remains a table-stakes feature that helps retain existing crypto-curious customers but does not materially drive new account growth |

Schwab and Morgan Stanley are responding to customer behavior they can already observe by building a distribution infrastructure in advance of a surge in demand that they cannot predict or miss.

The ETF era gave brokers a clear signal that their own clients wanted crypto, while keeping the actual trading relationship on someone else’s platform.

The companies that will own the next phase of retail cryptocurrency demand will be the ones that had direct, live access before the retail industry demanded it.