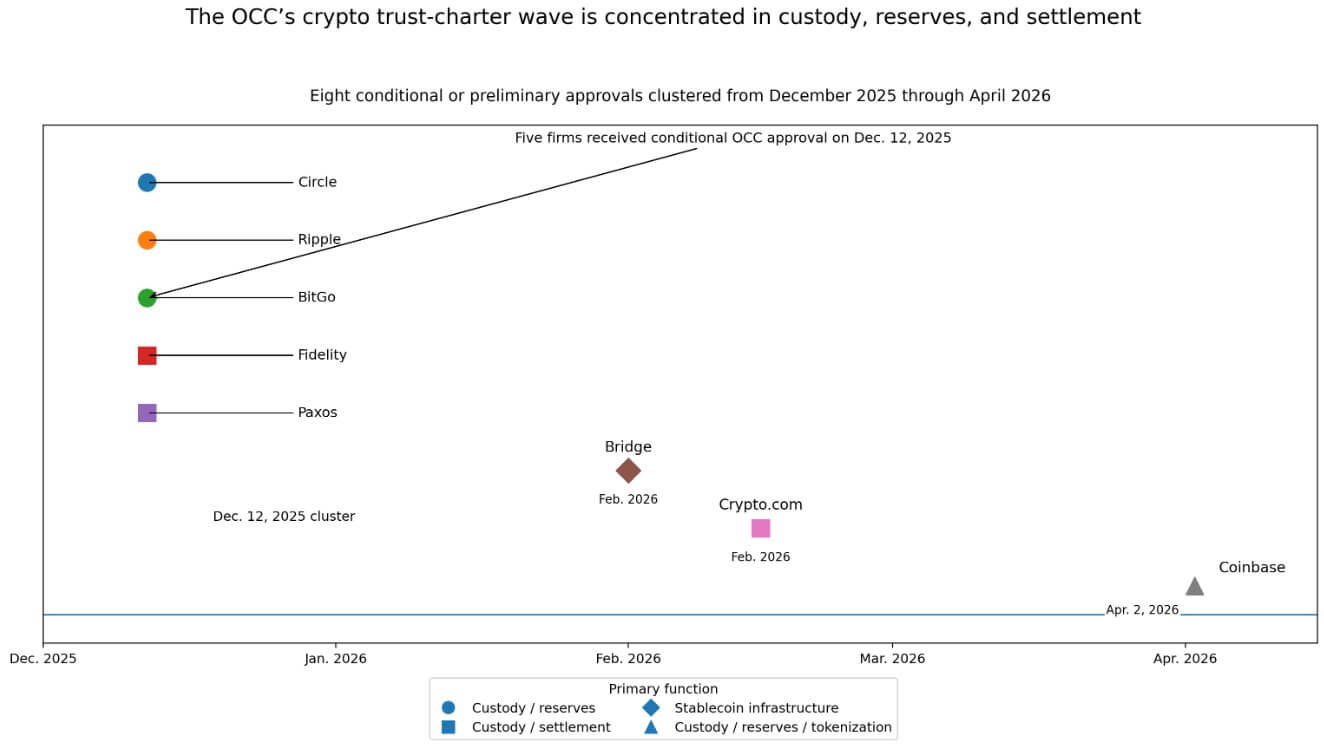

On April 2, Coinbase received conditional approval from the Office of the Comptroller of the Coin for a national trust charter.

Coinbase joined a cluster of at least eight companies that the OCC has been moving toward federal trust charter status since December 2025, and the cluster reveals a deliberate federal decision about which parts of crypto belong within the controlled system.

Why this is important: The US is shifting from regulating crypto to selecting which parts of the stack are within the bank’s perimeter. That decision determines who can scale up nationally, who absorbs institutional flows and who remains outside the system.

The OCC conditionally approved Circle, Ripple, BitGo, Fidelity and Paxos on December 12, 2025. Bridge followed in February, Crypto.com in February and Coinbase in April.

Eight approvals in about four months, all clustered around custody, reserve management, stablecoin infrastructure and settlement. That density reframes Coinbase’s headline as a data point in a federal draft decision.

A national trust charter gives companies federal reach under one OCC regulator, allowing them to operate in all fifty states without having to collect a patchwork of state approvals.

National trust banks hold client assets and facilitate settlement under a fiduciary mandate, operating within a purpose-built custody and settlement structure. The practical value of this route lies in the scope and clarity of supervision: firms can hold client assets and handle settlement functions within a single federal framework.

Paxos has explicitly framed its national trust drive as a step beyond New York State’s trust structure, and that framing reveals an architectural logic.

The functions Washington likes to oversee

The approvals are centered around custody, reserves and settlement because that is the OCC’s comfort level currently.

Reports noted that Crypto.com’s charter would cover client asset management and trade settlement, keeping the company within custody and settlement functions. Bridge’s approval covered the issuance and orchestration of stablecoins, as well as reserve management.

The OCC’s Circle decision described digital asset custody and reserve management services related to its fiduciary activities. Coinbase said full approval could support tokenized securities and stablecoins.

Washington is drawing a line around the functions that have the most token financial needs, such as custody of assets, supporting stablecoin reserves and settlement infrastructure, and expanding supervisory authority over companies that provide them.

The companies best positioned in this environment are custodians, reserve managers, and stablecoin infrastructure operators.

Adjacent regulatory initiatives reinforce this reading. In March 2026, US banking regulators said that tokenized securities would not face additional capital requirements merely because they are tokenized, calling the framework technology-neutral.

The SEC allowed intraday trading in tokenized shares of the WisdomTree money market fund, approved Nasdaq’s tokenized trading proposal, and approved NYSE’s tokenized securities partnership with Securitize.

The OCC charter wave and the tokenization rules stack are moving together, with institutional infrastructure as a common thread.

VISUAL 2

The reintermediation arc

Crypto’s original commercial promise was to remove the regulated intermediaries that traditional financing required.

The practical outcome of the OCC cluster is reintermediation: the most commercially sustainable crypto companies are now competing to become a new class of regulated intermediaries. Tokenized finance needs custodians, reserve managers and settlement rails before it needs another trading platform with more listed assets.

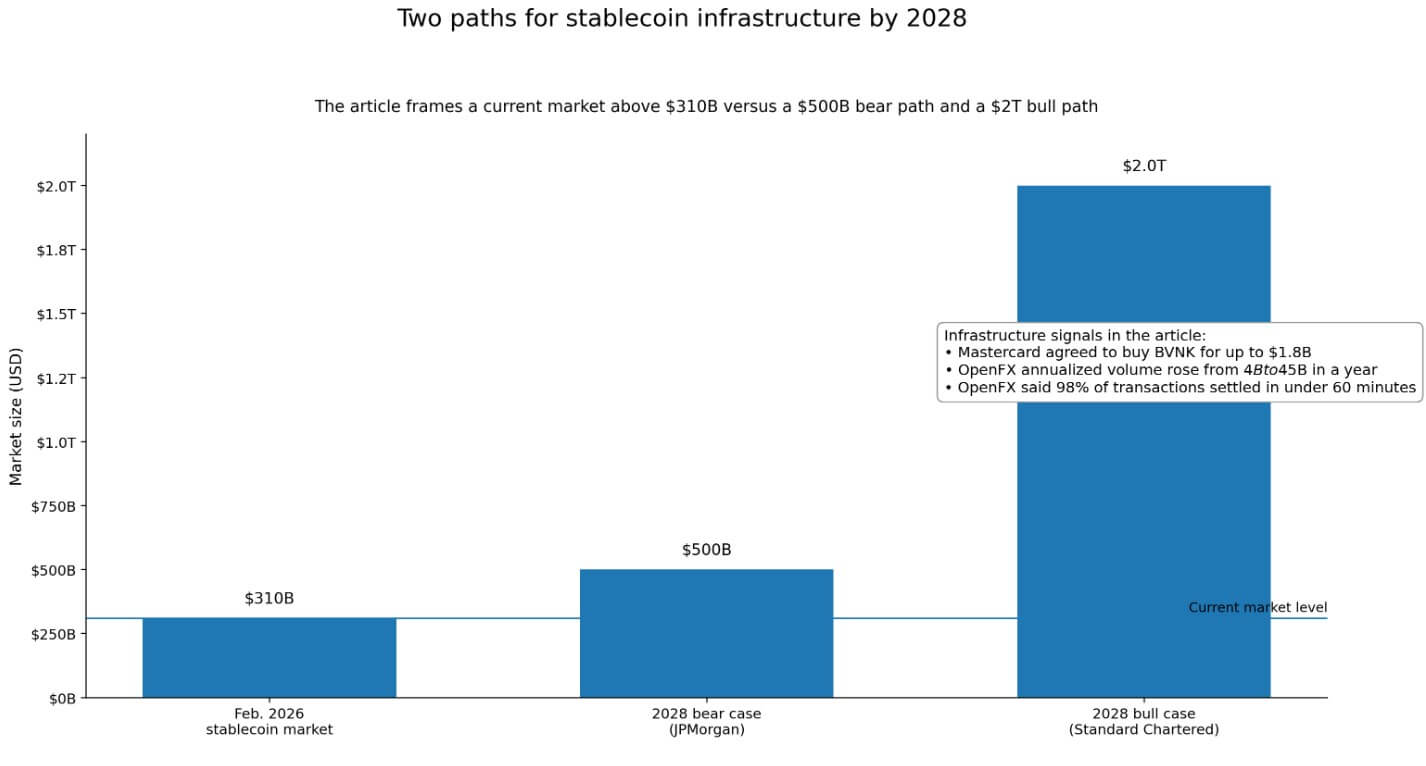

Capital is already pricing that reality. Mastercard agreed to buy BVNK, a stablecoin infrastructure company, for up to $1.8 billion. OpenFX raised $94 million and reported an annualized payment volume increase from $4 billion to $45 billion in one year, with more than 98% of transactions settled within 60 minutes.

The global stablecoin market was over $310 billion in February 2026. These are backend plumbing services, concentrated on custody, settlement and reserve management.

The competitive map is also getting smaller. Anchorage is currently the only digital asset company operating under a full national trust banking charter. The December cluster and subsequent approvals are conditional or provisional.

Achieving final operational status requires demonstrating capital adequacy, governance, and operational controls to OCC examiners. This bar will narrow the field to well-capitalized incumbents with an existing compliance infrastructure.

Two ways forward

In the bull case, the OCC finalizes stablecoin implementation in terms that institutions can operationalize.

Tokenized securities pilots on Nasdaq and NYSE are moving from proof-of-concept to live settlement infrastructure, while companies like Mastercard are accelerating the adoption of stablecoin rails across global payment corridors.

If stablecoins approach Standard Chartered’s $2 trillion forecast by 2028 and tokenized real world assets reach a similar size, federally-supervised crypto utilities will become digital finance’s scarce anchor.

The OCC’s chartered custodians and reserve managers collect margin on trillions of dollars of assets flowing through the infrastructure they control.

In the bear scenario, final approvals are slow as bank trade groups push their “lighter charter” objection, and the OCC responds by tightening terms on reserve buffers, liquidity stress tests, and operational controls.

The stablecoin market is closing in on JPMorgan’s forecast of $500 billion by 2028, a ceiling anchored by the fact that payments represent only about 6% of current demand for stablecoins, roughly $15 billion of the outstanding $310 billion.

In that world, state trust structures and banking partnerships remain practical, and the federal route becomes a premium niche.

The federal bet

Washington sorts the functions of cryptocurrencies into those it wants to oversee and those it doesn’t want to oversee, or at least not yet.

The charter cluster, the stablecoin reserve rules under the GENIUS Act, and the technology-neutral treatment of tokenized securities together form a regulated stack for crypto-native financial infrastructure.

The power the OCC is expanding is real. Still, it comes with oversight costs: monthly disclosure of public reserves for stablecoin issuers, weekly confidential reporting under the proposed implementation rule, and full OCC investigative authority.

| Point of comparison | OCC National Trust Charter | State trust/state licensing structure | Bank partnership model |

|---|---|---|---|

| Primary supervisor | OCC | State regulators | Federal/State Bank Supervisor of the partner bank plus partner compliance requirements |

| Geographic reach | National, under one federal framework for all 50 states | More limited; state-based and possibly patchwork | Depends on the structure of the partner bank and not on the company’s own charter |

| Core features highlighted in article | Custody, reserve management, stablecoin infrastructure, settlement, potential support for tokenized securities | Similar functions can be performed, but without the same single federal lane | Practical way to access banking, payment and settlement functions without your own federal charter |

| Strategic value | Clarity of supervision and national scale | Flexibility, but less unified than the federal route | Faster/practical access for companies that do not want or cannot obtain a charter |

| Supervisory charges | High | Lower than the OCC trajectory, based on the contrast of the item | Shared/mediated through banking partner requirements |

| Disclosure burden for stablecoins | Monthly Public Reserve Disclosures; weekly confidential reporting under the proposed implementation rule | Not described in article at the same level | Not described in article at the same level |

| Exam authority | Full OCC exam eligibility | State Examination Authority | Oversight of banking partners and exam environment, no direct OCC trust bank status for the crypto company |

| Companies that are best positioned | Well-capitalized incumbents with strong governance, capital adequacy and operational controls | Companies feel comfortable in a state-recognized tier | Companies using partnerships as a practical alternative to federal chartering |

| Competitive implication | Could become a scarce “picks and shovels” infrastructure if the financial scale is symbolized | Remains viable if federal approvals remain slow or limited | Remains viable in a bear/slower adoption scenario |

| Most important consideration | National reach and legitimacy, but heavier compliance and monitoring costs | Less supervisory intensity, but less federal uniformity | Less direct control over the infrastructure stack, but easier access route |

| Fits best in the frame of the article | Companies pursuing crypto utilities are under federal supervision | Companies that stay outside the federal line | Companies opt for a practical alternative, while the federal route remains selective |

The companies clearing this bar will operate nationally under a single federal regulator, holding institutional assets and processing token settlements in a framework that traditional financial counterparties can use.

Those who can’t or choose not to stay will remain in the state-licensed tier, and the charter wave will begin to resolve itself.