The U.S. economy added 178,000 jobs in March, nearly three times the consensus estimate of 60,000, and the unemployment rate fell to 4.3%. That’s the kind of print that resets macro narratives and hits risky assets before traders complete their first read.

Bitcoin was trading around $67,000, unfazed by the data. Ten-year government bond yields rose four basis points to 4.35%, and the dollar index rose to 100.08.

The market’s first-order view was clear: A labor market that looks this strong gives the Federal Reserve less reason to cut spending, which in turn produces tighter financial conditions and weighs on a macro-sensitive asset like Bitcoin.

Why this is important: Bitcoin responded to more than a job loss. The signal was a stronger labor market, which reduced the Fed’s urgency to cut rates. If that view holds, rates and the dollar could remain stable, keeping pressure on liquidity-sensitive assets like BTC.

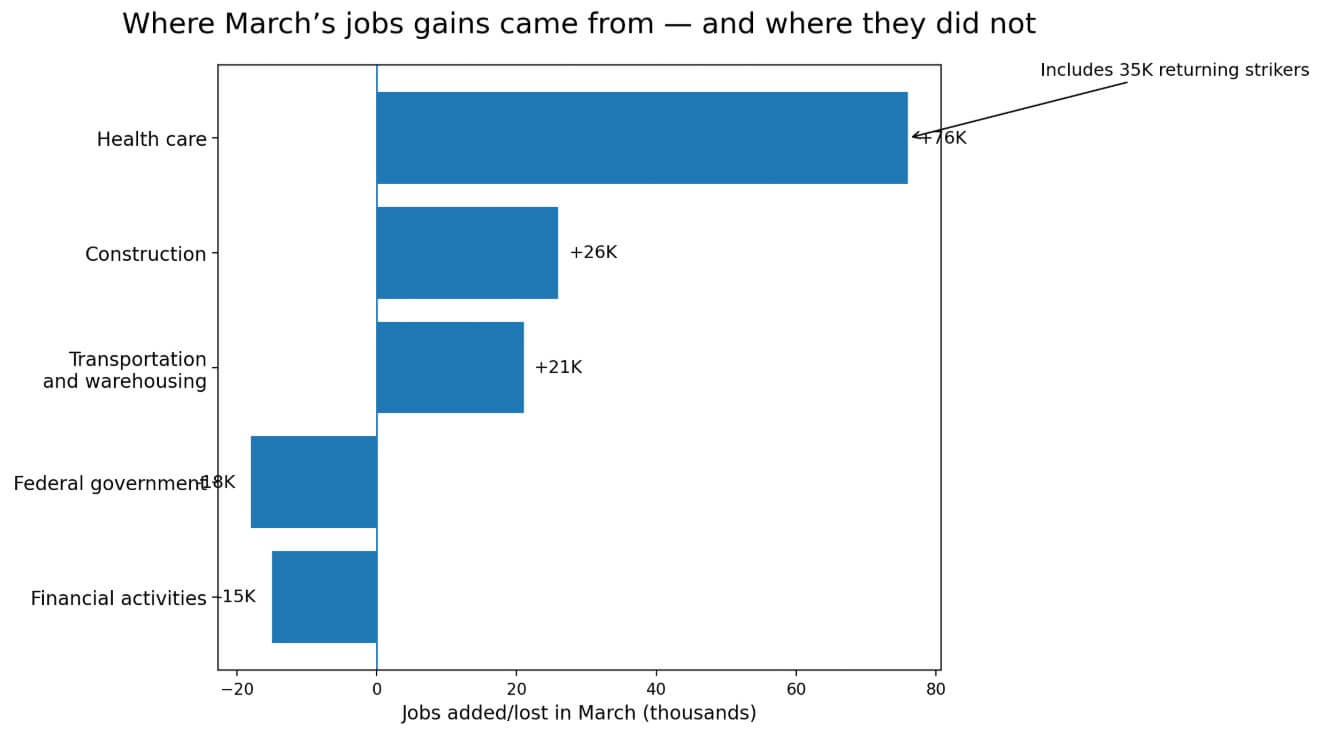

Zoom in on where those 178,000 jobs came fromand the image becomes less clear. In healthcare alone, 76,000 jobs were added, and 35,000 of those were workers returning from a strike at doctors’ offices. The numbers represented catch-up recruitment.

Construction added 26,000, partly due to weather, and transportation and warehousing contributed another 21,000. Federal government employment fell by 18,000, and financial activity fell by 15,000.

BLS noted that total payroll employment had changed little net over the past twelve months.

This backdrop means that March can be read as a rebound from a noisy February, with sector-specific catch-up driving most of the improvement.

The household survey runs in the other direction

The household survey, which tracks employed and unemployed people across the population, moved in the opposite direction of the payroll numbers.

The civilian labor force shrank by 396,000 in March, with participation falling to 61.9%. Household employment fell by 64,000, and the number of people not in the labor force increased by 488,000.

The number of marginally attached workers rose by 325,000 to 1.9 million, and the number of discouraged workers rose by 144,000 to 510,000. The average working week is shortened to 34.2 hours.

The average hourly wage increased by only 0.2% month-on-month and by 3.5% year-on-year, without any wage increase to supplement the wage bill.

| Indicator | March lecture | Why it matters |

|---|---|---|

| Non-farm payrolls | +178K | Strong headline was correct compared to expectations |

| Unemployment rate | 4.3% | Makes the labor market look solid at first glance |

| Civilian workforce | -396K | Suggests weaker labor market participation under the heading |

| Labor participation rate | 61.9% | Fewer people are working or looking for work |

| Domestic employment | -64K | The people-based survey moved against the wage survey |

| Not in the workforce | +488K | Reinforces the softer last under the hood |

| Marginally attached employees | +325K to 1.9 million | Shows a weaker labor relationship at the margin |

| Discouraged employees | +144K to 510K | Signals that more and more employees are giving up looking for a job |

| Average working week | 34.2 hours | A shorter workweek may indicate weaker demand for labor |

| Average hourly wage | +0.2% m/m, +3.5% y/y | No wage re-acceleration to confirm the wage bill |

The February revision adds another layer. BLS downgraded February from -92,000 to -133,000 and revised January from 126,000 to 160,000. The two-month net revision was only -7,000, making the pattern noisy and lacking consistent directional pull.

Wage growth averaged about 68,000 per month in the first quarter, a soft pace by any expansion standard.

BLS revises the monthly estimates twice as additional employer reports come in and seasonal factors reset.

Since 2003, the average absolute revision from the first to the third estimate has been 51,000 jobs. A revision of that magnitude would take March from 178,000 to around 127,000, which is noticeably less dramatic.

To erase the entire trend would require job creation of more than 118,000 in March, roughly 2.3 times the historical average, and ordinary revision noise is not involved.

BLS’s annual benchmark revision removed 898,000 jobs from the March 2025 wage level, four times the average absolute benchmark revision from the previous decade.

The review found that first-print payrolls have recently been carrying more uncertainty than markets normally price in the first hour of trading after a strong print.

The price channel behind Bitcoin’s decline

The Federal Reserve maintained its target range at 3.50% to 3.75% in March.

The average participant’s projection puts 2026 unemployment at 4.4%, PCE inflation at 2.7%, and the year-end Fed Funds rate at 3.4%. March’s unemployment rate of 4.3% and a payroll print of 178,000 gave policymakers no urgency to act.

NYDIG’s research describes the link between Bitcoin and macro in the same terms: BTC trades in accordance with real interest rates, liquidity and risk appetite. A Fed that maintains its position in a strong labor market removes the short-term catalyst who needs Bitcoin the most.

The February JOLTS report reinforces this without being alarmist. Openings held almost 6.9 millionbut hiring fell to 4.8 million, and the hiring rate fell to 3.1%, the lowest figure since April 2020.

Initial jobless claims for the week ending March 28 came in at 202,000, near a cycle low.

Together, these data points describe a labor market at a standstill, with layoffs in check, new hires tepid, and companies keeping workforces stable.

That environment will not lead to a Fed turnaround, and a Fed that does not turnaround will keep financial conditions tighter for longer.

Potential outcomes for Bitcoin

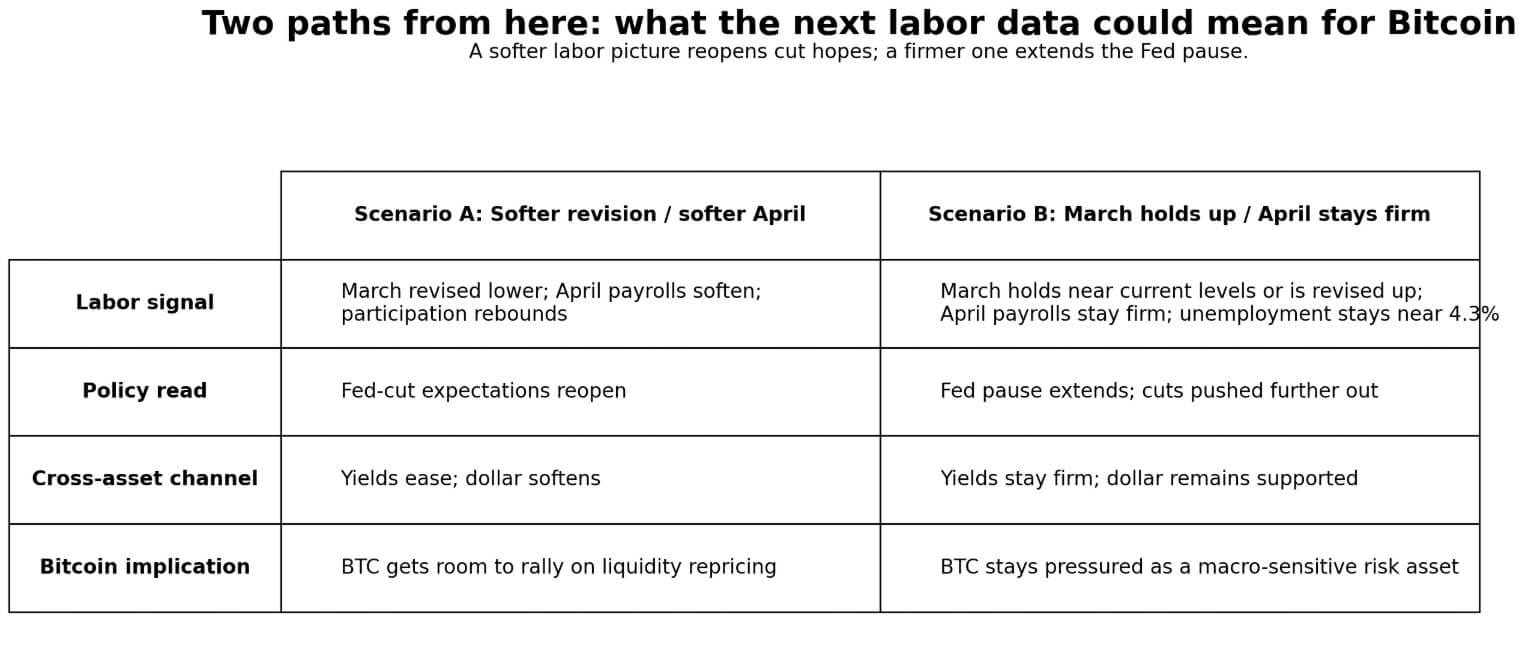

Bitcoin’s price action on April 3 was via the interest rate channel. The labor force eased downgrade expectations, higher yields and a stronger dollar tightened conditions for liquidity-sensitive assets. This channel can reverse.

If BLS revise March wages substantially downward, toward less than 100,000, and April wages also land weakly while participation recovers, the headline-only strength thesis gains traction.

Lowered expectations would reopen, yields would decline, and Bitcoin would have room to recover from liquidity repricing. Weakness in the household survey, the disruption of the healthcare strike and returns, and low JOLTS hiring make that path plausible, but April’s May 8 data should confirm this.

If March stays near current levels or the BLS adjusts higher, and April payrolls rise above about 125,000 while unemployment remains around 4.3% or lower, February becomes the clear outlier.

The Fed extends its pause with more confidence, cuts continue, and Bitcoin continues to trade as a macro risk asset with no near-term liquidity catalyst.

The cross-asset move on April 3, with a rise in yields, a rise in the dollar and a fall in BTC, showed that the market had already started pricing in that path.

The next employment situation release is scheduled for May 8 at 8:30 a.m. ET, which will push both April payrolls and the first revision into March.

That makes it the real checkpoint for any argument based on the April 3 picture. The March CPI will be released on April 10 and the next FOMC meeting will take place from April 28 to 29, two data points that the Fed processes before setting policy again.

The CPI in particular will test whether the strength of the labor market is associated with persistent inflation or with the wage slowdown that the March publication already indicated.