A new argument about state reserves is gaining ground: an asset doesn’t really function as a reserve if it can’t be accessed during a crisis. That shift is pushing Bitcoin into the policy debate, not as a growth strategy, but as a hedge against sanctions, custody risks and geopolitical disruption.

A recent Bitcoin Policy Institute article on Taiwan begins with a familiar argument that the country’s reserves are overconcentrated in dollars. Gold is performing below its potential, and Bitcoin could complement both.

Readers who stop there will miss the more consequential claim hidden in the blockade-and-invasion framework on pages 5 through 7, where the article attempts to redefine what makes a reserve asset fail.

Traditional reserve analysis assesses assets based on liquidity, price stability and credit quality. The BPI document adds a fourth test: Can the asset still be moved, spent or mobilized if shipping lanes are blocked, the host state withdraws custodial access or another state becomes politically hostile?

That measure could leave gold stranded, dollar reserves becoming contingent, and Bitcoin remaining electronically portable regardless of physical access or diplomatic status.

That’s a bigger conceptual move than advocating a Taiwanese BTC position.

Why this is important: The reserve policy is no longer just about returns, liquidity or stability under normal circumstances. If governments come to view access under stress as a core reserve test, Bitcoin will move closer to the discussion as a contingency asset rather than a speculative asset.

From macro bets to sovereignty insurance

For years, the Bitcoin argument at the state level ran on one track: cap the monetary cut, diversify reserves, take advantage of the adoption momentum.

That argument still appears in the BPI article, especially in the pages about the accumulation of US debt and the Federal Reserve’s balance sheet expansion. The more original contribution is elsewhere, where the newspaper ranks the reserves based on whether they remain accessible under duress.

A government only has to accept that government bonds, correspondent banking networks, physically stored metal and foreign government securities each have their own specific dependencies.

The policy question revolves around which asset remains accessible if storage, transport or politics in the host country go wrong.

Official reticent behavior already confirms that framing extends far beyond Bitcoin proponents. The IMF reports that total international reserves, including gold, reached SDR 12.5 trillion at the end of 2024.

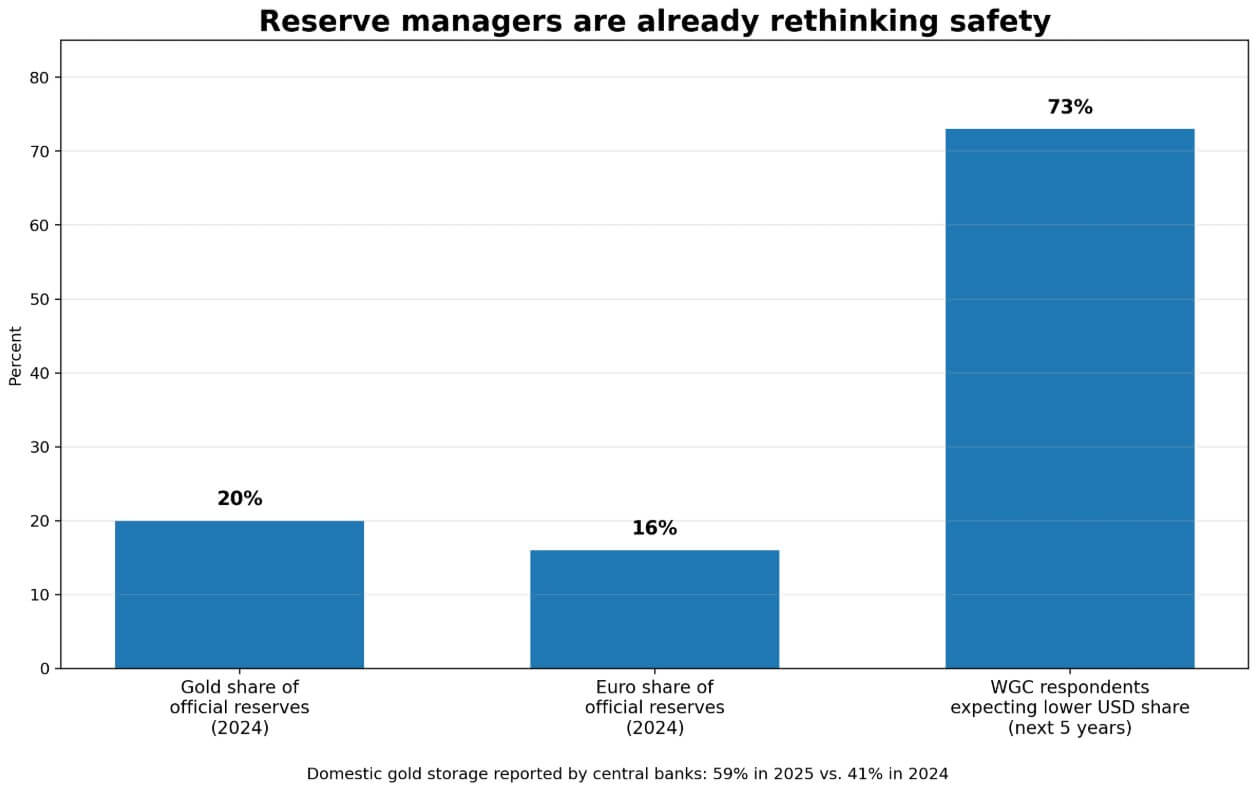

The ECB reported that gold’s share of global official reserves reached 20% of market value in 2024, surpassing the euro’s 16%, and that central banks bought more than 1,000 tons that year.

The 2025 World Gold Council survey found that 73% of respondents expect a lower amount of US dollars in global reserves over the next five years, and the share of central banks reporting domestic gold storage rose to 59% from 41% a year earlier.

Reserve managers are already broadening the definition of reserve risk, and the BPI document extends that logic to Bitcoin.

| Possess | Good luck in normal times | Vulnerability of the crisis | Failure mode under stress | Why it matters in the article |

|---|---|---|---|---|

| US dollar reserves / government bonds | Deep liquidity, high credit quality, global reserve standard | May be politically restricted by host country policies, sanctions or coercive measures | Freezing / conditional access / political pressure | Shows that a reserve can remain ‘safe’ on paper, but becomes less useful in practice |

| Gold | Long-standing reserve ballast, inflation hedge, widely accepted by official institutions | Difficult to move quickly, physically grasp, vulnerable to seizure or transportation bottlenecks | Stranding / seizure / logistical failure | Explains why portability and physical control are now more important in reserve analysis |

| Bitcoin | Digitally portable, carrier-like, can be moved without shipping lanes or physical transportation | High volatility, administrative burden, limited acceptance by the official sector | Institutional reluctance/policy hesitationinstead of physical immobilization | Enters the story as a potential asset for accessibility of last resort, rather than as a conventional safe backup |

| Diversified non-dollar government securities | Reduces dependence on a single reserve issuer while still fitting into conventional reserve frameworks | It still depends on external sovereign systems, settlement infrastructure and market access | External dependence / reduced neutrality | Serves as a bear-case alternative: reserve managers may choose this over BTC even after accepting entry risk |

| Domestically vaulted gold | Improves custody control while maintaining gold’s reserve role | Still suffers from transport friction and limited portability during acute crises | Limited mobility instead of pure custody risk | Shows why gold can benefit from the same entry risk logic without completely solving it |

This is the real shift underlying the debate: reserves can still look safe on paper, while in practice they are more difficult to use. Once that divide enters policy thinking, Bitcoin will be judged less on returns and more on access.

Living proof of access risk

The access risk argument draws strength from concrete recent events.

In March, Russia’s central bank challenged the EU freeze, which affected about $300 billion in sovereign wealth funds. That dispute keeps the central premise operational: reserve assets can become politically immobilized while retaining their face value.

An asset owned on paper but frozen in practice has already failed as a reserve, regardless of its creditworthiness.

Brazil’s central bank drew a parallel conclusion. On March 31, Brazil increased gold’s share of reserves to 7.19% from 3.55% in one year, while the US dollar’s share was cut to 72, citing diversification as a driving force.

The BPI article argues that Bitcoin belongs in that same diversification calculus, especially for reserve decisions driven by geopolitical logic.

The US Strategic Bitcoin Reserve adds a clear data point. The White House order prioritizes the reserve of forfeited BTC, prohibits direct sales, and considers additional acquisition only on a budget-neutral basis.

That pulls the Bitcoin reserve language into an actual sovereign administrative structure, setting a precedent regardless of the unconventional funding source.

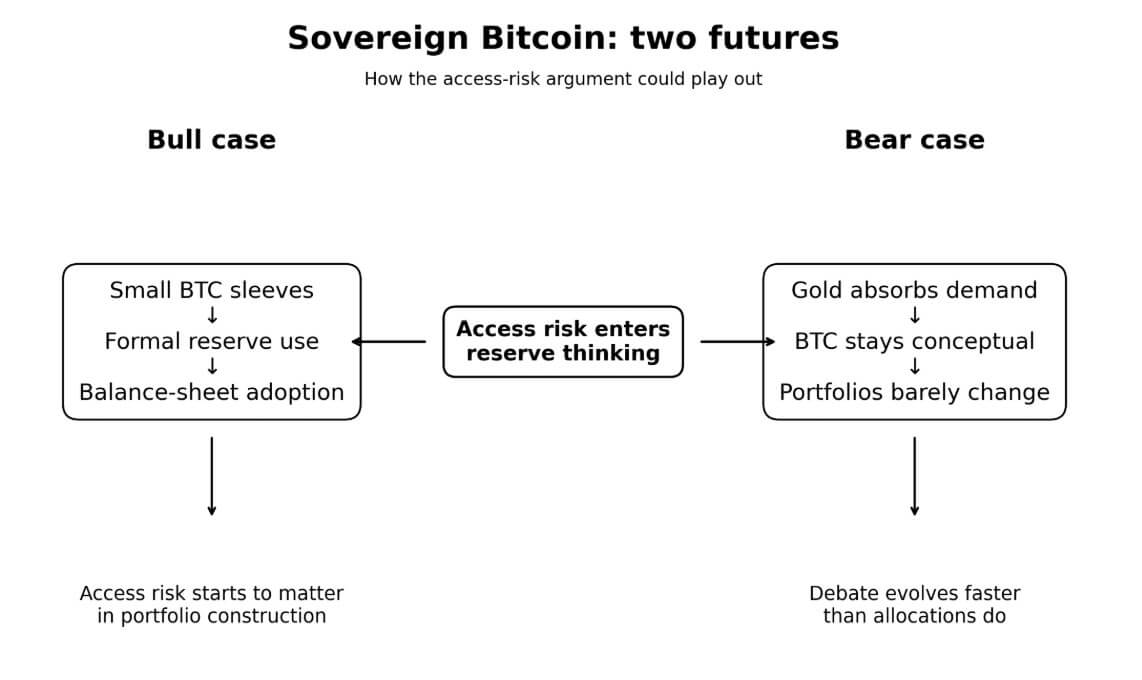

Two Futures for the Sovereign Bitcoin Argument

Scale makes the bull case concrete. Taiwan’s reserves are roughly $602 billion, and a 1% Bitcoin cover would be around $6 billion, while a 5% cover would be $30 billion.

The broader calculation is grimmer: 0.1% of global reserves, about $16.25 billion, would represent about 1.2% of Bitcoin’s entire market capitalization at current prices of around $68,000.

Participation in the reserve system, even on a marginal scale, would have price consequences long before a central bank would make a final allocation decision.

The bull case requires a handful of politically prominent or sanctions-conscious states to first formalize small BTC positions in the 0.25% to 1% range, or consider already seized or mined Bitcoin as reserve before buying more.

Ferranti’s sanctions risk modeling supports this direction: in one sanctions scenario, his model produces an optimal Bitcoin share of around 5% for exposed states. The sovereign Bitcoin discourse would then shift from advocacy documents to actual balance sheet items.

The bear case accepts the entry risk criticism and still concludes that Bitcoin loses.

Reserve managers recognize that physical gold entails logistical dependencies and that dollar reserves entail political dependencies, then decide that the volatility, administrative burden, and near-zero adoption of the official sector leave Bitcoin in a weaker position than domestically stored gold and diversified non-dollar Treasuries.

Gold absorbs the demand for diversification that the entry risk argument for BTC should generate, and Bitcoin’s role as a reserve remains conceptual. The debate evolves while the portfolios maintain their composition.

Where the argument holds up and where it shows tension

The BPI article is strongest when it treats portability and resistance to attack as true reserve characteristics, based on observable reserve behavior.

That framework follows official data: geopolitics is now visibly influencing the composition of reserves, and the desire to hold assets outside of concentrated dependence on one counterparty is real and is already moving portfolios.

The document goes too far if the adoption momentum or price increase is evidence that the policy case has been resolved. Official institutions still weigh acceptability, legal clarity and operational custom alongside entry risk, and these factors weigh heavily on portability rankings.

The most credible version of the paper’s argument is its own position: Bitcoin as a small insurance cover next to gold, optimized for access.

For most of Bitcoin’s history as a subject of reserve policy, the central question in official circles was whether Bitcoin was safe enough to hold. That framework consistently worked against BTC, as its volatility kept it below Treasuries and gold by any conventional measure.

Reserve managers are now focusing on which assets remain deployable in the event of a hostile geopolitical environment. The revival of gold, domestic preferences for vault management, sanctions-induced disputes over reserves and the fragmentation of the payments infrastructure all show that reserve managers are already looking for conventional assets.

Bitcoin proponents are bringing BTC into that same conversation, and the BPI paper shows how that argument works at its most sophisticated.

The next test The question is whether this logic remains limited to papers and strategic rhetoric, or whether real restraint behavior begins to change. If even a small number of geopolitically exposed states start treating entry risk as a formal reserve criterion, Bitcoin will move from a theoretical hedge to a policy variable, and that would matter well beyond Taiwan.