The Morgan Stanley Bitcoin Trust completed its first month of trading without a single day of net outflows, providing an early test case for how a Wall Street bank’s brand, pricing and distribution network can change the competitive landscape of the digital asset market.

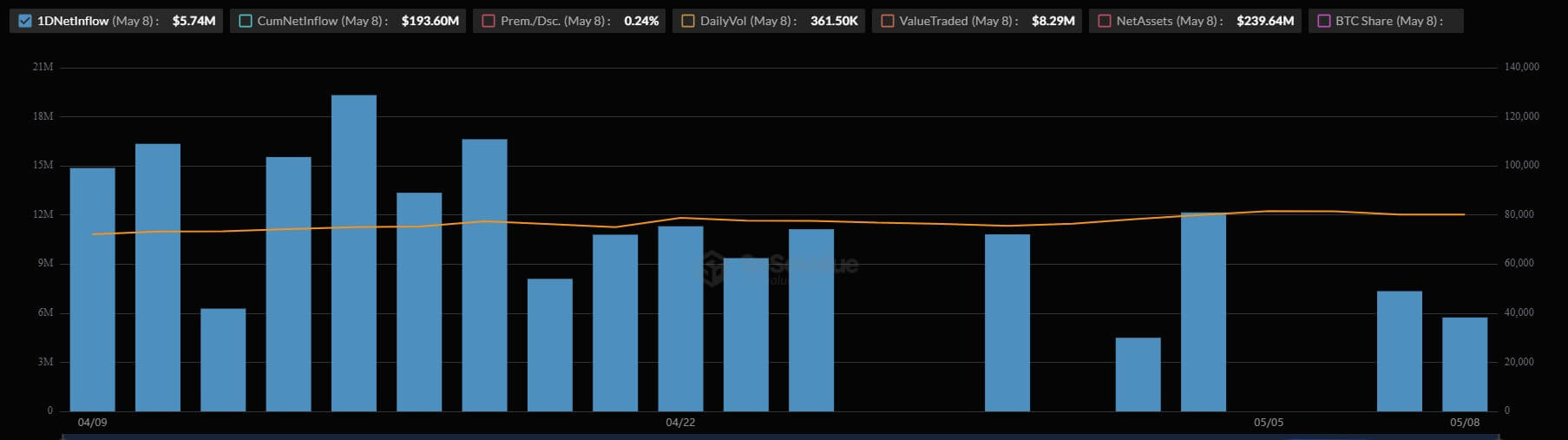

The product, which trades under the ticker MSBT, launched on April 8 and has since generated net inflows of approximately $193 million while managing more than $240 million in assets.

Facts SoSoValue shows that the fund’s first month included 17 days of positive inflows and five days of flat inflows, with no daily redemptions recorded.

This streak stands out during a period of local volatility for competing US Bitcoin funds. For context, the broader Bitcoin ETF category has lost $422 million in combined outflows over the last two trading sessions, while MSBT has successfully absorbed another $13 million in fresh capital.

This divergence gives Morgan Stanley a flow record that fund sponsors typically need quarters to build.

Currently, MSBT owns approximately 2,620 Bitcoin, which ranks it 32nd among crypto ETFs and exchanges that hold Bitcoin, according to Bitcoin Treasuries data.

While it trails the largest spot funds in raw size, its resilience during market downturns indicates that institutional clients are treating the fund as a long-term allocation.

How Morgan Stanley’s MSBT achieved a flawless first month of trading

To understand why this capital is proving so sticky, market observers look directly at the origins of the issuer, as Morgan Stanley’s main advantage in a turbulent market is familiarity.

While crypto-native firms and dedicated asset managers pioneered the US spot Bitcoin ETF market, the bank offers investors a distinctly different entry point: a regulated financial institution with an established asset management and advisory base.

The bank addressed this distinction at the launch. Amy Oldenburg, head of digital asset strategy at Morgan Stanley, noted that digital assets are increasingly intersecting with traditional markets. She highlighted the firm’s focus on helping clients navigate this shift through financial structures they already trust.

This sees MSBT as part of Morgan Stanley’s broader customer service model, rather than as a standalone, speculative crypto business.

However, brand awareness and trust are only half the story, as the company also uses its cost structure to gain market share.

The fund charges a 0.14% sponsorship fee, which the bank positioned as the lowest of all spot Bitcoin ETPs at launch. It deliberately undercuts the Grayscale Bitcoin Mini Trust by 0.15%, Bitwise by 0.20%, and BlackRock’s industry-leading iShares Bitcoin Trust by 0.25%.

While the margin may seem small in percentage terms, fees are becoming a critical battleground as Bitcoin ETFs transition from new launch products to standard portfolio allocation tools.

For fiduciaries, advisors and institutions, a lower expense ratio has a major impact on model portfolio decisions when multiple products track the same underlying assets and offer similar execution and custody standards.

This aggressive pricing strategy gives Morgan Stanley a highly effective pitch while expanding access through its internal asset management channel. The company employs approximately 16,000 financial advisors who oversee $9.3 trillion in client assets.

Even a fractional allocation shift through this massive network could exponentially expand MSBT’s asset base in the coming quarters. Yet this internal, advisor-led growth is only one pillar of a much broader rollout on multiple fronts.

Bitcoin ETFs record longest weekly inflows this year

Meanwhile, MSBT’s first month also benefited from a broader recovery in demand for US spot Bitcoin funds.

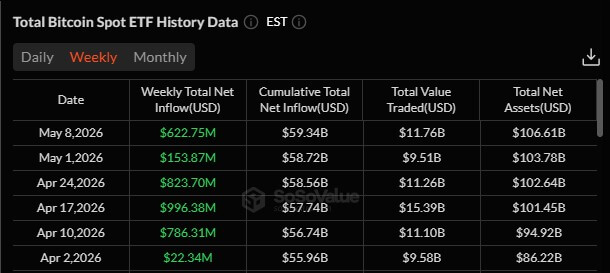

Data from SoSoValue shows that U.S. Bitcoin ETFs have taken in more than $3 billion for six consecutive weeks of net inflows through May 8, the longest streak of weekly gains since last summer.

This trend indicates that demand has stabilized after Bitcoin’s uneven start to the year, even as daily flows remain sensitive to price swings and macroeconomic pressures.

Macroeconomic research platform Ecoinometrics noted that this steady improvement in ETF inflows suggests real long-term capital is returning to the digital asset market, rather than a temporary recovery due to short-term positioning or leverage.

For MSBT, the broader market recovery provides useful context. Morgan Stanley hasn’t entered a weak ETF market, but the lack of daily redemptions still sets it apart in a category where capital still moves unevenly among issuers.