The CLARITY Act markup has moved past the stablecoin yield stalemate, to Senator John Kennedy’s housing frustration, unresolved protections for software developers, and the Republican voting math that Senate Bankers Chairman Tim Scott has yet to close.

The Tillis-Alsobrooks compromise, which broke the yield impasse, allows stablecoin rewards to be tied to platform usage and activity, while banning passive returns on inactive balances, preventing crypto firms from replicating high-yield savings accounts.

Scott must now turn that policy victory into a coalition victory. He has publicly said he wants “thirteen out of thirteen Republicans” before switching to a bipartisan markup in May.

Punchbowl reported that Kennedy is withholding his support in part due to frustration with the White House over the 21st Century ROAD to Housing Act. Kennedy’s Build Now Act cleared the Senate for that package, the House of Representatives passed its own version, and bicameral reconciliation is not yet complete.

His influence on the CLARITY Act timeline is positional, as he has a voice that Scott needs, and his prize is a movement on housing that Scott cannot unilaterally deliver.

| Problem | Where it is now | Who is most important | Why it matters for markup |

|---|---|---|---|

| Stable coin yield | Key impasse resolved by the Tillis-Alsobrooks compromise: rewards tied to usage/activity allowed, passive returns on inactive balances excluded | Tillis, Alsobrooks, bank lobby, crypto companies | Takes away the most visible policy battles, but doesn’t in itself provide an increase |

| Frustration over Kennedy’s housing | Still an active political complication related to the unfinished bicameral work on the ROAD to Housing Act / Build Now Act | Senator John Kennedy, House of Representatives Leader, White House | Kennedy holds a vote that Scott needs, causing a non-crypto issue to impact the crypto timeline |

| Republican voting math | Scott has said he wants all 13 bench Republicans before moving to a bipartisan markup | Tim Scott and the thirteen banking Republicans in the Senate | Full GOP unity makes markup easier and helps build Democratic support later |

| Protections for software developers | Still unresolved; the BRCA/Section 1960 language is still under negotiation | Bank negotiators in the Senate, votes of the judiciary, crypto industry | One of the largest remaining dust battles and a possible source of delay |

| Ethical/AML issues | Still alive and able to reopen the opposition even after the compromise on yields | Democrats, law enforcement, bank critics | Could delay or limit support even if Republicans unite |

| Calendar/floor time | The window tightens; delays after mid-May make a summer trail more difficult | Senate leadership, committee staff, House counterparts | Every week something goes wrong compresses markup, floor planning, house coordination and conference time |

From one fight to several

Banks feared that issuers paying returns on inactive balances would pull deposits out of the traditional system, while crypto companies wanted returns as a product feature. The Compromise resolved that dispute by separating activity-based rewards from passive accumulation.

Banks still privately worry that the “economically or functionally equivalent” clause leaves room for solutions, but the public language has done enough for Scott to move past it.

Galaxy’s April update identified DeFi provisions, protections for non-custodial software developers, ethics provisions, and full Republican committee support as outstanding items. This cluster requires several negotiations with different stakeholders, taking place simultaneously against a tighter calendar.

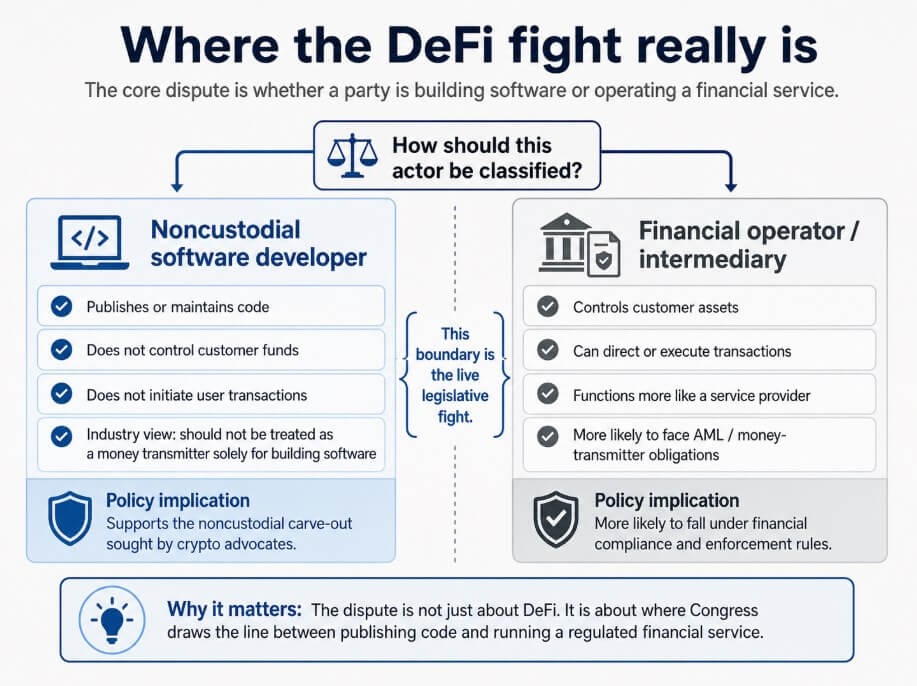

Software developer protections are technically the most consistently open item and the least publicly visible.

The Blockchain Regulatory surety Act framework and related Section 1960 language would exempt non-custodial software developers from certain compliance requirements, a provision the crypto industry considers essential to keep DeFi development onshore.

Law enforcement agencies have raised objections to previous versions of this language, arguing that broad exceptions could weaken enforcement of money transmitters and create AML blind spots.

Senate Bench Republicans have continued to publicly defend the text, which in itself is proof that the fight is still alive. The dispute centers on where Congress draws the line between building software and operating a financial service.

That distinction has real consequences because the developer and operator of a protocol can be the same person or completely different parties, and compliance obligations are governed by different rules depending on that classification.

The calendar underneath everything

The bill still faces ethics disputes, AML objections, Senate time limits and election year timing frictions, and missing a July window would effectively close legislative opportunity for the cycle.

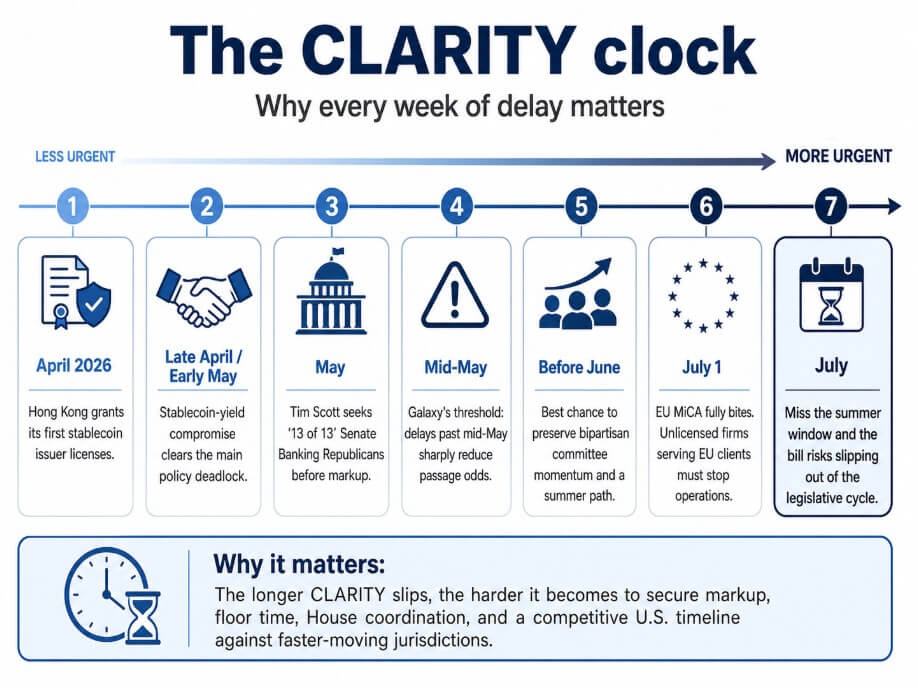

Galaxy put the chances of passage at about 50-50 and said they would drop sharply if the markup goes past mid-May. Meanwhile, Polymarket’s 2026 CLARITY Act approval odds rose 17% in the past week, from 47% to 64%.

A unanimous vote in the Republican committee makes it easier to attract Democratic co-sponsors and harder for leaders to prioritize floor time. Each week of slippage compresses the available space for house coordination, conference negotiations, and floor planning.

The global context makes that compression costly, as Hong Kong’s regulator granted its first licenses to issue stablecoins in April 2026, and the EU’s MiCA framework comes into full effect on July 1, forcing unlicensed companies serving EU customers to cease operations.

The bull case requires Scott to win over all thirteen Republicans by securing enough movement on housing to satisfy Kennedy, or by having a direct conversation that separates his mood on market structure from his frustration on housing.

At the same time, lawmakers are producing language at the software developer level that is narrow enough to avoid law enforcement resistance without taking away the non-custodial exceptions that the industry considers essential.

If both conditions apply, a two-way commission margin becomes feasible before June and a summer bottom remains feasible.

BlackRock’s IBIT held approximately $63.5 billion in net assets as of May 1, with nearly $630 million in inflows across all US-traded Bitcoin ETFs on the same day.

Bitcoin’s institutional access infrastructure already functions without CLARITY, but the bill’s passage carries more weight for exchange economics, stablecoin generation, and DeFi formation than it does for Bitcoin’s fundamental investability.

The bear case scenario unfolds as the markup passes mid-May and outstanding items pile up. Bitcoin holds up better than the rest of the crypto complex in that scenario, because the ETF rails, demand for government bonds, and the custody infrastructure built over the past two years are independent of congressional action.

However, the broader argument that Washington is building a framework that invites domestic capital formation is losing credibility with each delay, and more of the next wave of stablecoin monetization, tokenization, and developer activity is being attracted to jurisdictions with rules already in place.

The stablecoin compromise gave Scott a policy anchor. Kennedy’s demand for housing and negotiations over developer protections will be a test of whether he can keep his coalition on the ground where the disputes are political and structural.

Galaxy’s mid-May threshold noted that missing the time will make the bill’s chances of passage more dependent on leaders finding time in an election year for legislation that still draws objections from several parties.