The Senate Banking Committee advanced the Digital Asset Market Clarity Act on a 15-9 vote, and the National Cryptocurrency Association (NCA) says the vote’s most lasting effect could be a signal that Washington is building a defined regulatory framework for digital assets.

The bill still needs a vote in the Senate, and Democrats have raised concerns around anti-money laundering provisions and political conflicts of interest, while banks and crypto companies have yet to agree on how to handle stablecoin rewards.

Those disputes are live, but NCA says the commission’s advance already sends a message that ordinary consumers need to hear.

Ali Tager, VP of External Affairs at the NCA, told CryptoSlate:

“Meaningful progress toward clearer, smarter safeguards signals to consumers and businesses alike that crypto – one of the fastest-growing financial technologies – will operate under predictable scrutiny, just like traditional banks or credit unions do. That means greater confidence in when, where and how to handle digital assets safely and responsibly.”

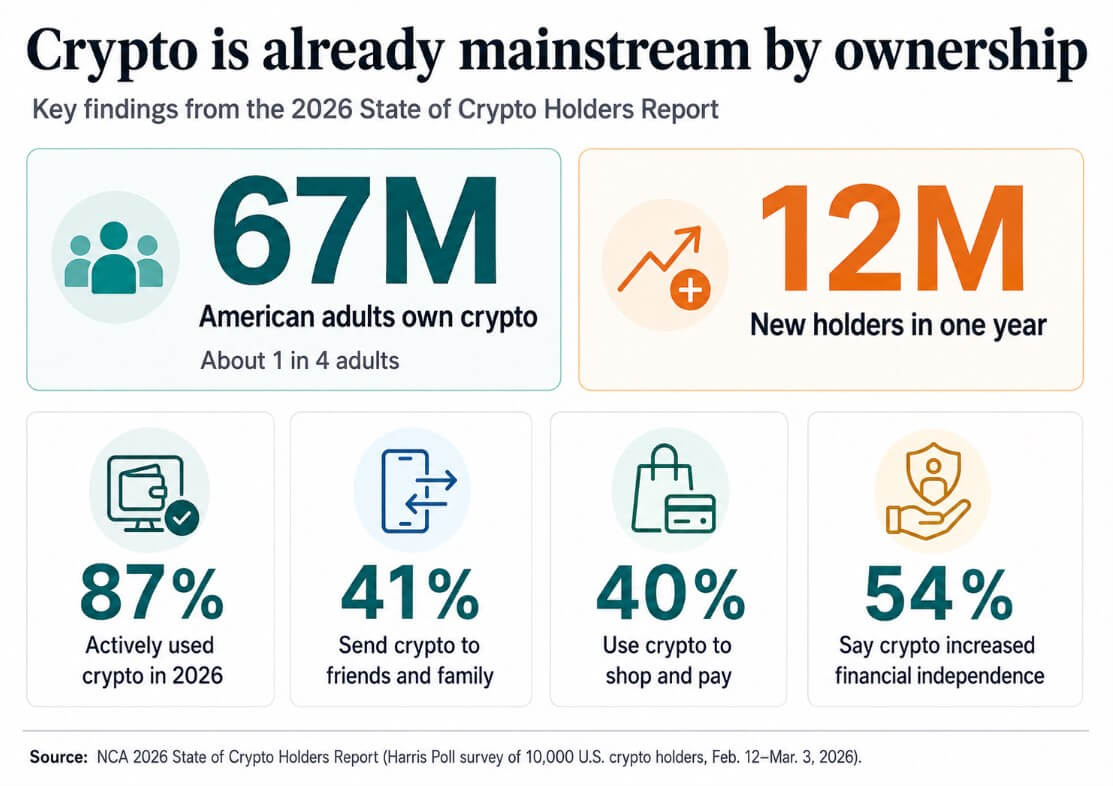

NCA’s State of Crypto Holders Report 2026, based on a Harris Poll survey of 10,000 US crypto holders conducted from February 12 to March 3, maps the consumer audience behind the committee’s vote.

More than 67 million American adults now own cryptocurrency, up from one in five just a year ago, while 12 million new holders entered the market during that period.

The survey found that 87% were actively using crypto in 2026, up from 80%, and 41% sent crypto to friends and family, up from 31%. Using crypto to shop and pay for goods and services was highlighted by 40% of people.

Financial independence through crypto was mentioned by 54%, and 37% plan to send crypto to employees in the coming year, a figure that puts the technology in salary conversations.

NCA found that 69% of holders trust crypto, compared to 65% who trust traditional banking, and almost one in three said their perception of crypto improved most by seeing how it integrated with systems they already trusted, such as PayPal, Visa and banks.

Tager said:

“When the legal uncertainty around crypto is replaced by clear consumer protection, the tool feels less new and more normal.”

Regulation as one lever

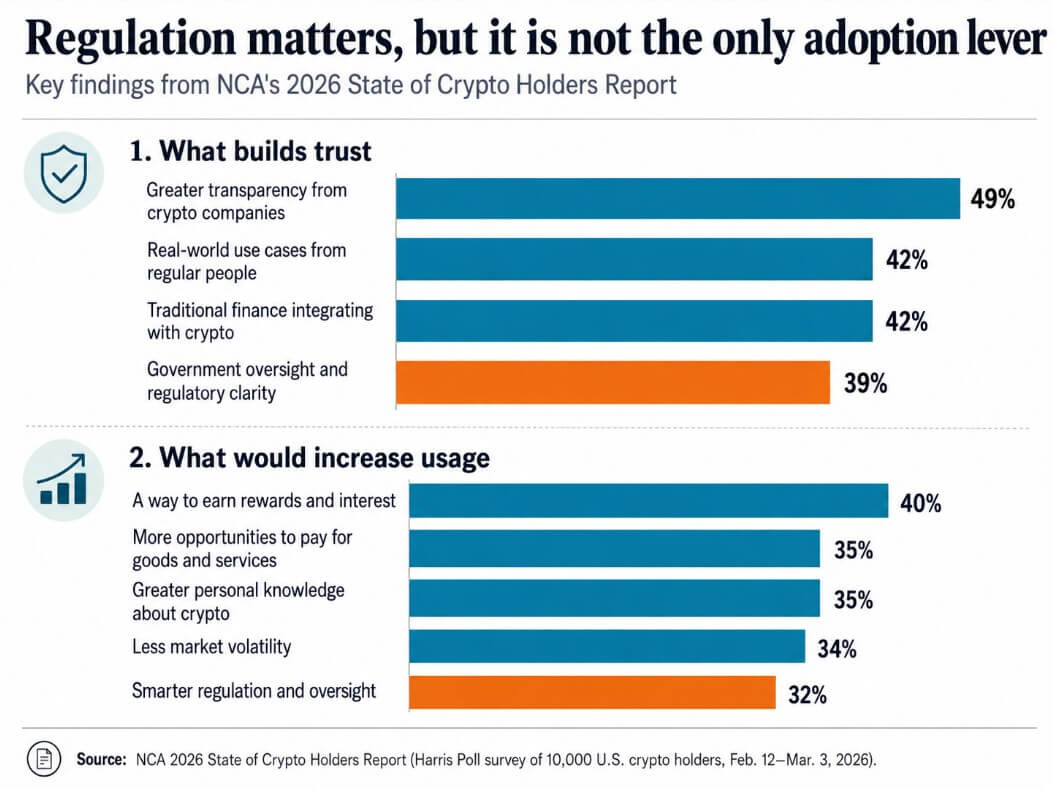

Regulatory clarity is a real driver of adoption, but the NCA data puts this in the middle of the field.

Among the confidence-building signals, 39% of holders cite government oversight and regulatory clarity, behind transparency from crypto companies at 49% and best practices from ordinary people at 42%.

Among the factors that make holders more likely to adopt crypto, earning rewards and interest ranks first at 40%, with greater payment acceptance at 35%, personal knowledge at 35%, reduced volatility at 34% and smarter regulation at 32%.

That arrangement means that a federal framework addresses a meaningful part of the underwriting gap, with payment instruments, rewards programs and personal exposure each working separately alongside each other.

More than 33% of crypto holders are women, an increase of 10% in one year. The 55 and over cohort is now larger than the 18 to 24 cohort among recent buyers, and more property owners work in construction than in the financial sector.

The South accounts for 38% of all property owners, the West 27%, and the Northeast and Midwest each 18%, a distribution that reflects the general U.S. population. The people a federal consumer protection framework would reach are already in the marketplace.

Tager rated:

“The CLARITY Act should be a major catalyst to secure American leadership and prevent innovation and capital from moving abroad.”

The EU Framework for Markets in Crypto Assets came into effect in June 2023 and is now fully implemented, while the UK regulatory regime for crypto assets is expected to come into force in October 2027.

Jurisdictions with established frameworks are becoming the default destinations for product development and compliance infrastructure when US regulations lag behind.

Two scenarios you can expect

If the CLARITY Act passes the Senate with the core framework of market structure intact, the consumer confidence thesis has a direct mechanism.

The 39% of holders who cite government oversight and regulatory clarity as a confidence builder will get the assurance they described, exchanges and custodians will get clearer compliance paths, and the 76% of holders who want their bank to let them buy and manage crypto in addition to regular accounts can find that option routine.

The 90% of holders who plan to buy more crypto in the coming year would do so within a better-defined legal environment, and the NCA’s argument that clearer rules drive the transition from ‘new to normal’ would have a legislative anchor.

| Scenario | Legislative outcome | Consumer signal | Institutional signal | Implication of adoption | Market framework |

|---|---|---|---|---|---|

| CLARITY passes with core framework intact | Senate passage leaves the bill’s market structure framework largely intact, followed by House reconciliation, agency rulemaking, and implementation. | The 39% of holders who cite government supervision and regulatory clarity as confidence builders are given a clear legal anchor. The 76% Those who want banking access to buy, hold and manage crypto may see that option become more routine. | Exchanges, custodians, banks and crypto companies will have clearer compliance paths for their activities in the US. | Crypto’s transition to ‘normal’ is accelerating as regulations, consumer protections and banking integration make digital assets feel more normal. | Boring becomes bullish: regulations support regular confidence instead of speculative hype. |

| BRIGHTNESS blocks or breaks | Senate Coalition Breaks AML Rules, Concerns Over Political Conflicts, Disputes Over Stablecoin Rewards, or Broader Negotiations. | The 32% of holders who say that smarter regulation would make them more likely to use crypto are not given any new legal certainty to respond to. | Companies continue to wait and see, with compliance strategy determined by uncertainty and fragmented guidance from agencies. | Adoption continues, but through separate channels: payments, rewards, merchant acceptance, banking access, personal exposure, and private sector integration. | Signal without status: the markup shows political feasibility, but not enough certainty to unlock the next phase. |

If Democratic objections to anti-money laundering rules, political conflict questions and unresolved stablecoin reward disputes break the coalition in the Senate, the markup becomes a signal without statute.

The 32% of holders who said smarter regulation would make them more likely to adopt crypto would have no new legal certainty to respond to. Institutional players would maintain the wait-and-see approach that has characterized US crypto compliance throughout the current cycle.

In that outcome, adoption continues with payment integration, rewards programs, access to banking and personal exposure, with each process operating on its own timetable.

The committee’s advance of the CLARITY Act tells the market that a sustainable U.S. framework for digital assets is politically feasible.

The path involving a vote in the Senate, reconciliation with the House of Representatives, agency rulemaking, and implementation is long enough that crypto’s near-term adoption curve will still depend on the factors already visible in the NCA’s data.

What Congress still has to decide is what kind of boring it wants.