Bitcoin is seeing a return to mid-month strength this year, and it’s becoming increasingly difficult to separate it from Strategy’s (formerly MicroStrategy) growing preferred stock machine. The financing channel helps the company continue to buy flagship digital assets while adding an increasing layer of costs to its balance sheet.

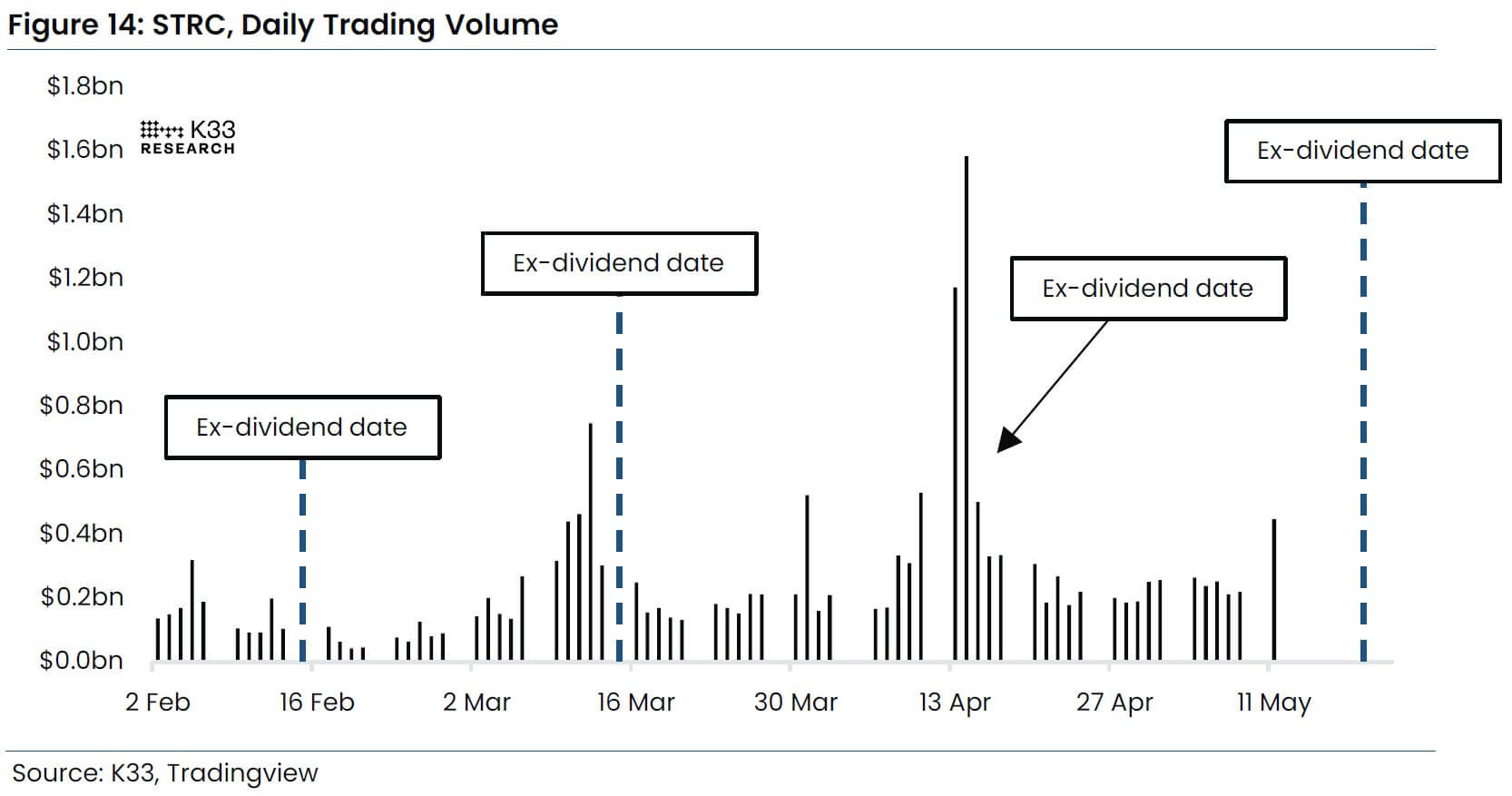

Research firm K33 has linked the pattern to Strategy’s perpetual preferred stock, STRC, which has become a key source of liquidity for the world’s largest corporate Bitcoin holder. The instrument pays dividends at the end of the month, but investors must own the shares by the 15th to qualify for the payout.

That deadline has turned the middle of every month into a predictable window of demand. Investors buy STRC before the cutoff, causing trading volume to increase, and the stock moves back towards its par value of $100.

Once STRC trades at or above par, Strategy can issue new shares through its at-the-market program and use the proceeds to buy more Bitcoin.

Facts from STRC.live shows this loop has become active this week, with STRC back on track and giving Strategy enough room to fund the purchase of over 5,000 Bitcoin before the next ex-dividend deadline on Friday.

This move extends a pattern that has seen Strategy’s capital market activity become a recurring feature of Bitcoin’s spot market flow. It also reinforces why STRC has become the most dominant preferred stock in the market.

STRC converts the demand for dividends into buying Bitcoin

The volume of Bitcoin acquired through this particular funding channel has increased aggressively since the beginning of the year.

Research from K33 noted that Strategy bought 4,467 Bitcoin in January using STRC proceeds. By March, purchases linked to the preferred shares had risen to 22,131 Bitcoin.

In April, the figure rose again to around 46,872 Bitcoin, demonstrating how quickly the instrument has evolved from a financing tool to a key driver of the company’s accumulation strategy.

Vetle Lunde, head of research at the crypto research firm, described the setup as a mechanical source of demand.

According to him, STRC attracts yield-oriented investors before the ex-dividend date, which will restore preferred stock and give Strategy the market depth needed to issue more shares. The company then converts that demand into spot Bitcoin purchases.

Meanwhile, Strategy is now trying to tighten the cycle. The company has suggested shifting STRC’s dividend schedule from monthly payments to bimonthly distributions, arguing that more frequent payouts would reduce reinvestment delays and improve market efficiency.

The change would also create more frequent opportunities to raise capital. That could strengthen the mid-month buying pattern, while leaving Strategy more reliant on a product that carries a much higher cost than its previous financing vehicles.

The cheap capital era of strategy is giving way to preferred stock

While the STRC mechanism helps shape BTC’s market performance in the short term, institutional researchers are sounding the alarm about the long-term sustainability of the trade.

For much of its Bitcoin accumulation history, the Michael Saylor-led company had relied on issuing common stock and convertible debt.

Both were attractive when Strategy’s shares were trading at a wide premium to the value of their Bitcoin investments, and bond investors were willing to accept low coupons in exchange for exposure to potential stock gains.

However, these conditions have deteriorated significantly over the past year.

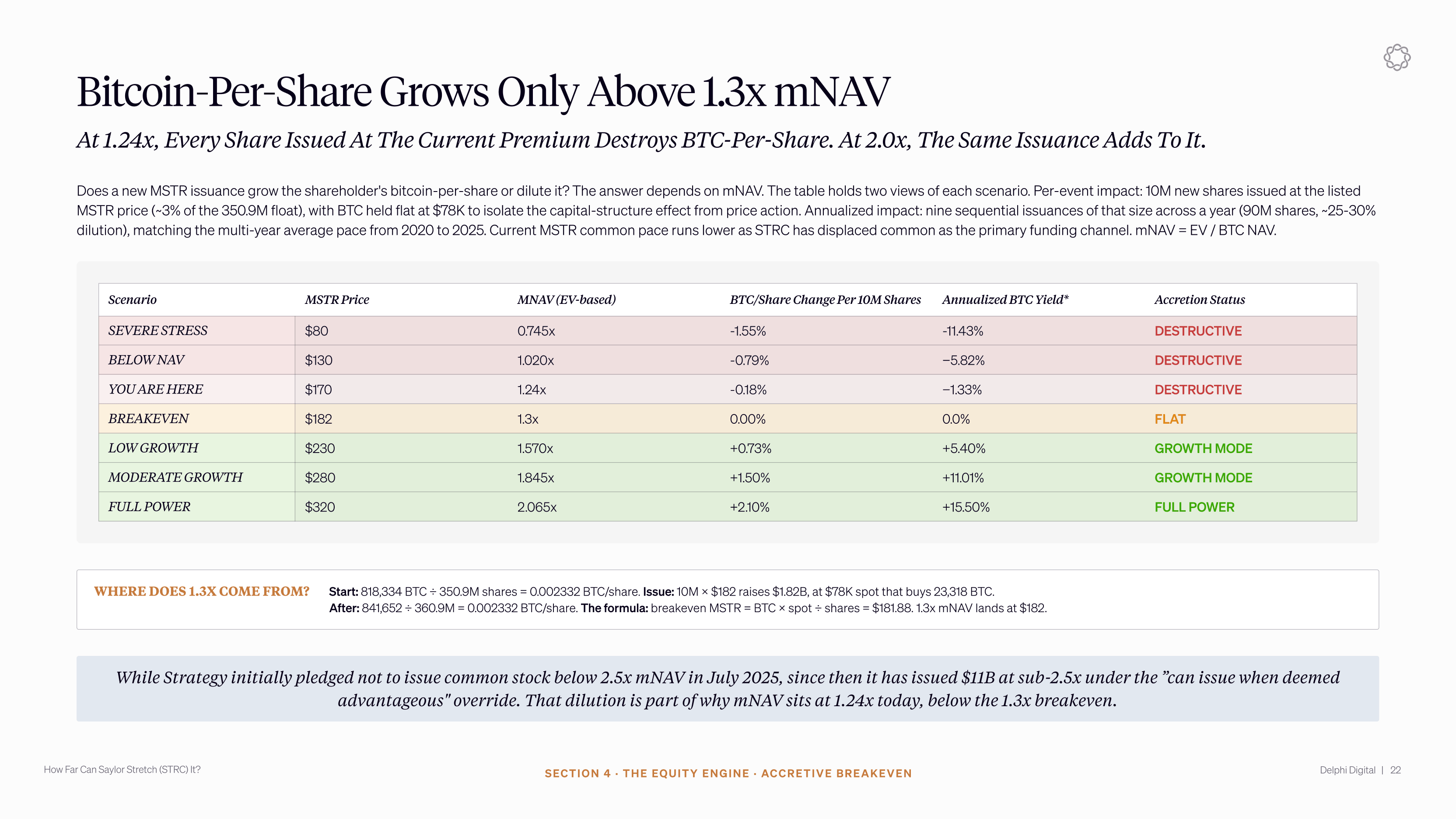

Delphi Digital estimates that Strategy’s common stock premium is now approximately 1.24 times enterprise value-based net asset value. At that level, issuing common stock offers far fewer benefits for increasing Bitcoin per share.

Moreover, the period for convertible debt has also narrowed. Strategy has approximately $8.2 billion in principal from prior deals, with repayments scheduled for September 2027.

This leaves STRC as the main funding driver for Strategy’s recent BTC purchases. Because preferred stock sits below senior debt and convertibles in the capital stack, investors need more compensation for the risk.

STRC’s annualized return has already risen to 11.5%, a sharp increase from the cheaper financing that supported Strategy’s previous Bitcoin purchases.

Bitcoin trading per share is becoming more expensive

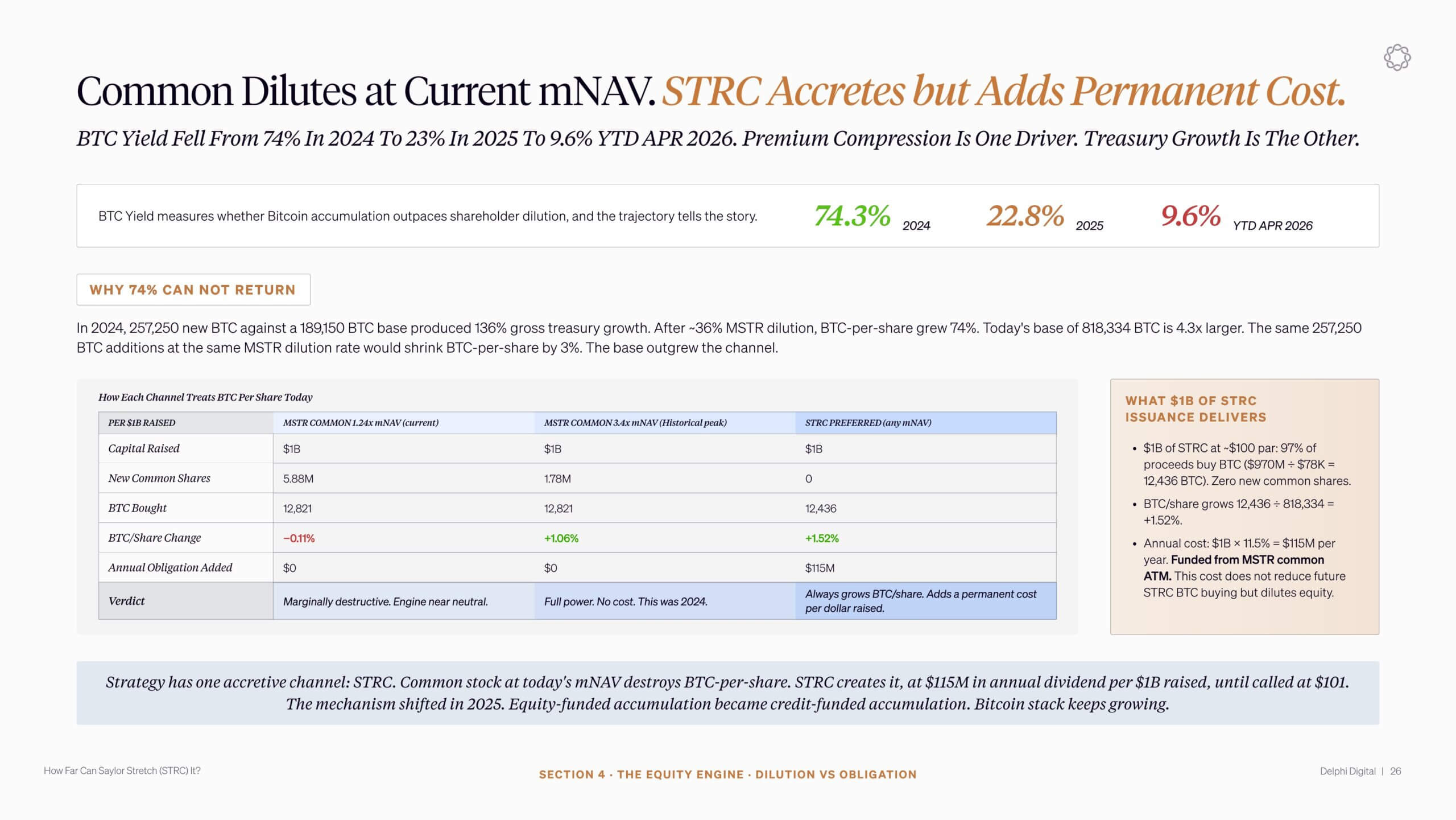

STRC is still helping Strategy purchase Bitcoin without directly issuing common stock for the purchase. That’s central to the company’s argument that the program can support Bitcoin per share growth.

Delphi estimates that about 97% of every $1 billion raised through STRC can be staked in Bitcoin. At current prices, that could boost Strategy’s Bitcoin-per-share metric at issue time.

The costs come later. Every $1 billion in STRC creates roughly $115 million in annual dividend obligations. These payments must be made, and Delphi expects that Strategy will rely on the issuance of common shares to do so.

That turns the preferred program into a delayed dilution mechanism. The Bitcoin purchased with STRC proceeds may initially increase exposure per share, but the recurring dividend account gradually offsets that benefit as more common shares are issued to fund payments.

Delphi’s model shows that the effect fades over time. Bitcoin per share growth could exceed 7% in the first year of the program, but drop to just above 3% in the third year as the preferred stock base grows and dividend obligations increase.

The pressure is becoming more acute as the STRC authorization limit of $28.3 billion approaches. Once Strategy reaches that limit, the preferred stock engine can no longer continue to fund new purchases at the same pace. However, the dividend proposal remains.

Under these conditions, Delphi predicts that Bitcoin’s net growth per share could turn negative and shrink by almost 6% per year as common issuance is used to collect preferred dividends rather than expand holdings.

A bear market could highlight the loop

The bigger risk is that STRC’s mechanisms work best when Bitcoin is rising and investor appetite for returns remains high.

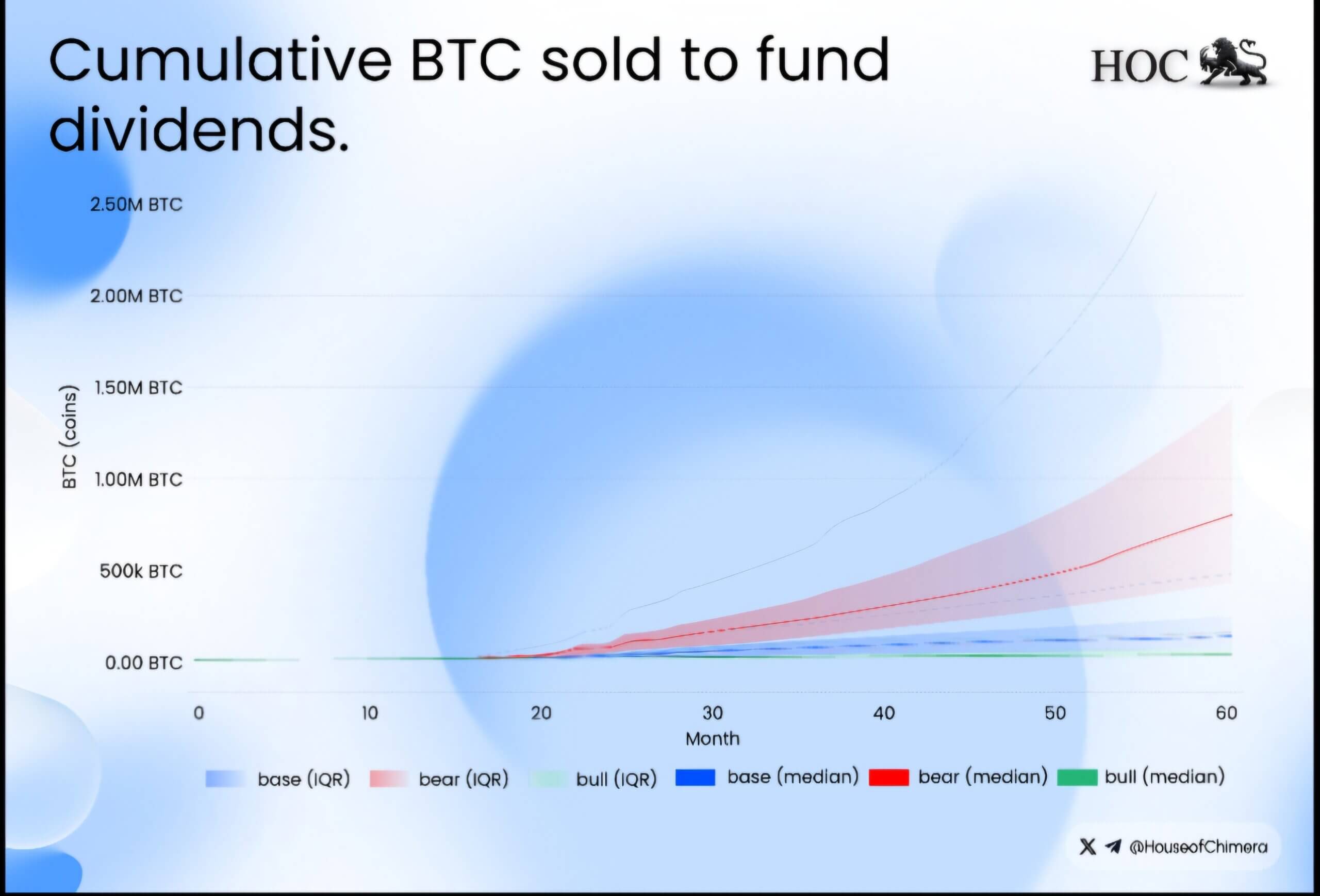

Blockchain research firm House of Chimera has done just that warned that a sustained downturn could create a negative feedback loop.

According to the company:

“As Bitcoin declines, STRC may need to increase its dividend to maintain investor demand. But higher yields also increase Strategy’s monthly cash obligations just as the BTC investments lose value. This creates a structurally fragile feedback loop in which deteriorating market conditions force the structure to promise ever-larger payouts.”

The House of Chimera test suggests that under pessimistic market conditions, Strategy’s $2.5 billion cash reserves could be depleted within 17 to 22 months.

This would leave the company facing a liquidity crisis at a time when market access is at its weakest.

Furthermore, the bigger danger is that Strategy could ultimately be forced to sell Bitcoin to meet dividend obligations.

Any forced selling would increase pressure on the spot market, weaken demand for STRC and potentially require even higher returns to restore investor confidence.

In House of Chimera’s worst scenario, the stack of preferred shares could eventually force a turnover of nearly 800,000 Bitcoin.

The strategy moves from accumulation to balance sheet management

By recognizing changing financial realities, Strategy’s business posture has evolved.

The company’s recent revelations indicate a more active approach than the previous “never sell” attitude associated with founder and chairman Michael Saylor.

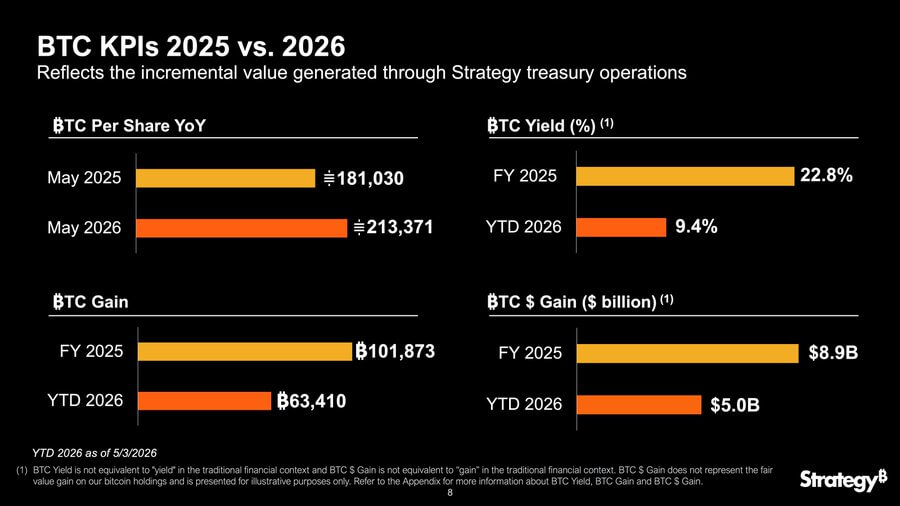

The focus has shifted to maximizing BTC Yield, a corporate metric that tracks the growth of physical Bitcoin holdings relative to the number of shares outstanding. In an X-post, Phong Le, president and CEO of the company, said, said:

“Bitcoin per share (BPS) is our true north. Strategy uses multivariate models every day to optimize capital, equity, debt and credit decisions to maximize annual BTC return (growth in BPS). YTD we delivered 9.4% BTC return and $5.0 billion in BTC profit.”

It will become harder to keep these numbers positive as cheap debt disappears, preferred dividends increase, and the cost of each new Bitcoin purchase rises.

For now, STRC continues to support a reliable mid-month Bitcoin bid. The instrument converts the demand for return into fresh capital, and that capital continues to flow to the spot market.

However, trade is also becoming more vulnerable. Strategy’s financing engine can still boost Bitcoin in the short term, but the same structure builds a larger dividend burden behind each purchase.

As STRC grows, the question for shareholders and Bitcoin traders becomes whether the company can continue to increase Bitcoin per share after the cost of the machine is fully accounted for.