Artificial intelligence and crypto-native tools are quickly shaping a future where software agents can fund themselves, execute cross-chain strategies, and move through financial markets without anyone in control.

According to a recent report from DWF Ventures, automated and agentic activities now account for an estimated 19% of all on-chain transactions, with 17,000 agents launched since 2025.

The report added that the agent economy is already here.

For now, most of this machine-driven money movement happens via bots shuffling stablecoins through a patchwork of payment systems that still rely on centralized gateways, managed issuers and card-linked rails.

Crypto is building the interfaces for machine payments before it has built the autonomy that these interfaces are supposed to enable.

The machine that actually runs

Before you start treating DWF’s 19% figure as a pure measure of autonomous finance, it helps to understand what it actually measures.

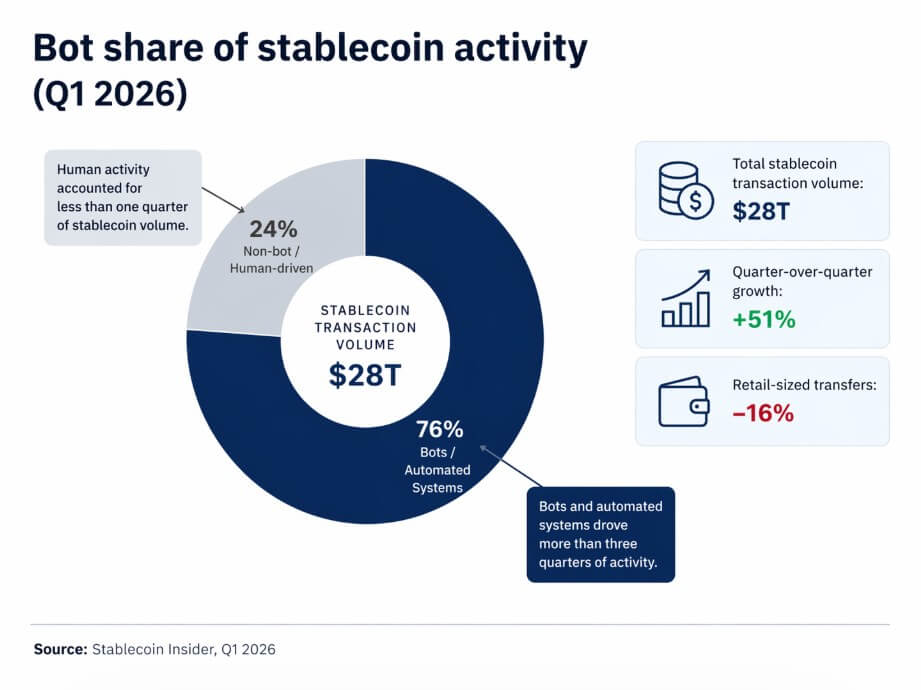

Stablecoin Insider’s data for the first quarter of 2026 shows that bots are responsible for this approximately 76% of stablecoin transaction volumewhile total stablecoin transaction volume reached $28 trillion, up 51% quarter-on-quarter.

Transfers in retail sectors fell by 16% over the same period, the sharpest decline on record.

Automation, routing and high-frequency machine activity drove this growth. Software systems that programmatically move dollars across exchanges, wallets, liquidity platforms, and payment intermediaries are the currently visible form of the machine economy.

Stablecoins naturally fit in here. They don’t vary in price, they opt for programmable rails, and they use the same computing units that most software already understands. For any automated system that needs to move money without worrying about currency risk, stablecoins just make sense.

DefiLlama currently estimates the stablecoin market at around $320 billion, with Ethereum holding around 52% of the supply, Tron at $86.7 billion, predominantly in USDT, Solana at $15.7 billion, led by USDC, and Base at $4.9 billion, also heavily in USDC.

The blockchains at the forefront of machine-driven stablecoin flows are the ones already built for moving dollar tokens at scale. In many ways, stablecoins are turning into the first money rails used as much by software as by people.

Hybrid in design

Payment standards for machine commerce are starting to take shape. x402, Stripe’s Machine Payments Protocol (launching March 2026), and Google Cloud’s Agent Payment Protocol 2 are all signs that this space is gaining real momentum.

| Current infrastructure for automatic payments | Which would require complete autonomy |

|---|---|

| Stablecoin transfers supported | Self-financing and cash management by agents |

| Agent-to-agent or human-activated agent calls | Independent execution without human approval |

| Payment via card or bank-linked intermediaries | Native end-to-end settlement in the chain |

| Managed publishers and centralized gateways | Decentralized trust and identity systems |

| Compliance and custody handled by intermediaries | Built-in reputation, insurance and fail-safes |

| Hybrid payment standards (x402, MPP, AP2) | Autonomous optimization under changing market conditions |

The x402 Foundation, launched under the Linux Foundation April 2026includes Coinbase, Cloudflare, Stripe, Google and Visa as participants.

Still, x402’s public dashboard showed about 75 million transactions and $24 million in volume over the past 30 days, a dip in the bucket compared to the trillions already flowing through stablecoins.

Stripe’s x402 implementation runs through Stripe-managed deposit addresses and capture flows, while Google’s AP2 explicitly supports cards and real-time bank transfers in addition to stablecoins.

Artemis reports that crypto card volume, which grew from approximately $100 million per month in early 2023 to more than $1.5 billion per month by the end of 2025, is still mainly arranges via fiatrails.

Current infrastructure builds programmable machine-money interfaces on top of centralized systems.

Visa’s US stablecoin settlement product reached a Annual volume of $3.5 billion run rate at the end of 2025. In April, the company joined Tempo as a validator on a blockchain designed for agent trading.

Visa’s latest move confirms that the most active builders of the agent economy are designing hybrid rails.

DWF’s own report concludes that true end-to-end autonomy has yet to be achieved, and the architecture explains why.

A fully autonomous agent in financial markets needs a verifiable identity, custody arrangements that survive model failures, reputation systems that allow counterparties to extend credit, fail-safe mechanisms that limit damage, and financing flows that do not rely on human replenishments.

None of these layers exist at production scale. DWF’s performance data reinforces the finding that agents perform better in limited, rule-based tasks such as return optimization, while humans still perform better in messier trading contexts.

Today’s machine economy functions as automation for well-defined workflows. The conditions for independent financial decision-making, such as verifiable identity, custody, reputation systems and execution fail-safes, have yet to converge at production scale.

Chainalysis adds bot activity, MEV, liquidity provision and internal operational transfers inflating raw stablecoin volume.

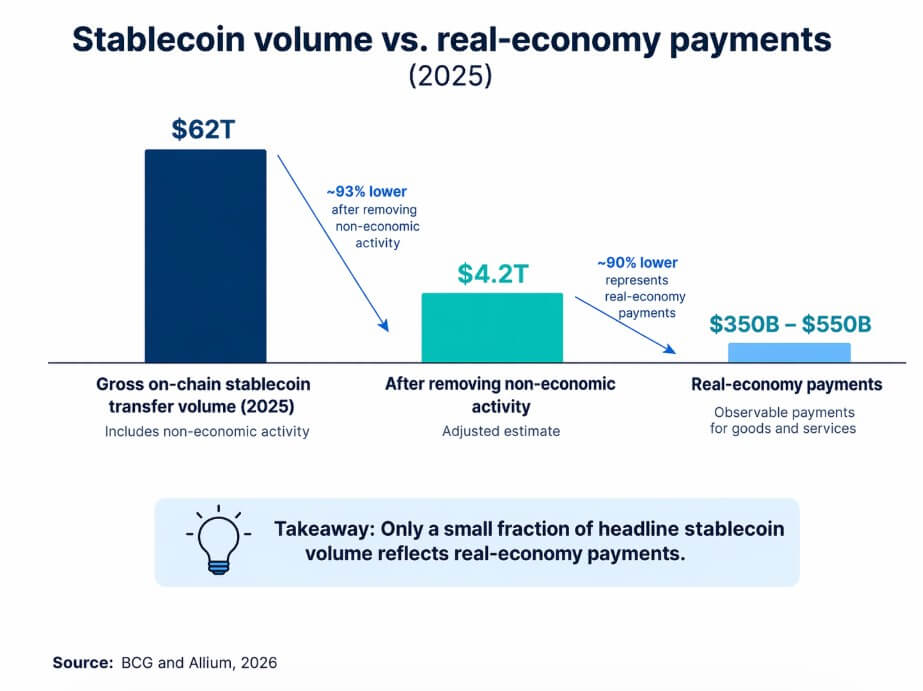

BCG and Allium estimate that of approximately $62 trillion in gross on-chain stablecoin transfer volume by 2025, only $4.2 trillion would remain after removing non-economic activities, with only $350 to $550 billion associated with payments in the real economy.

Much of what is recorded as machine trading is still market research.

Two paths from here

The bull case is that payment standards converge, regulated stablecoin issuers expand, and machine-to-machine payment flows move from proofs of concept to production.

Stablecoin’s market cap, currently nearly $320 billion, is approaching the higher forecast of $2.3 trillion by 2030, and adjusted payments activity is consistent with Chainalysis’s higher growth scenario, in which the number of stablecoin transactions begins to converge with Visa and Mastercard volumes over the next decade.

The platforms that combine trusted identity, compliant dollar liquidity, and low-friction orchestration between chains and off-chain services are leading the way.

The agent economy becomes a payment infrastructure story carried on crypto rails that most users never consciously interact with as crypto.

The bear case scenario is more consistent with current data. Bot volume in stablecoins remains high, but little of it is converted into sustainable machine trading in the real economy.

Card networks and banking intermediaries absorb most machine-readable payment demand without decentralizing anything, and regulatory costs concentrate operations among larger incumbents.

Stablecoins grow mainly through collateral from the exchange, liquidity from the treasury and settlement middleware. The current centralized infrastructure still limits programmable machine money on a full economic scale.

BCG and Allium’s finding that only $350 billion to $550 billion in gross stablecoin volumes represented real economy payments in 2025 supports this reading: the base is much smaller than the numbers suggest, and the distance between the current stack and a truly autonomous economy is greater than the promotional narratives acknowledge.

The railway problem

The deeper battle running through all of this revolves around who processes machine payments and where trust lies once programmable dollar flows reach meaningful economic scale.

Stripe, Visa, Google and regulated stablecoin issuers are running that race at least as often as any crypto-native agent platform.

Treasury data shows that stablecoin issuers hold about 53% of their assets in government bonds, with their holdings increasing by about $70 billion since 2022.

Each step in machine-based stablecoin adoption increases demand for short-term U.S. government debt and enshrines dollar-denominated settlement standards in automated systems around the world.

The agent economy, as currently constructed, is more of a dollar expansion story, where the entities best positioned to control the rails are the same ones that already control the pipes.