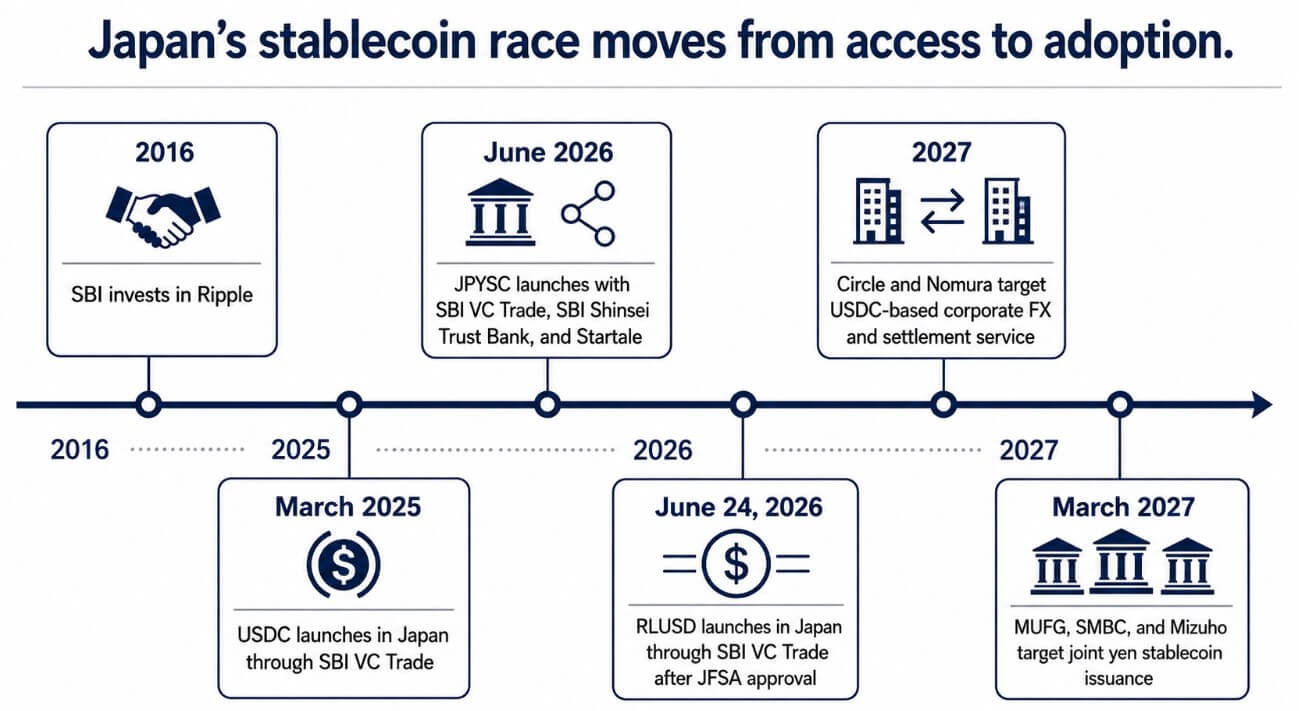

Ripple and SBI announced the official launch of RLUSD in Japan on June 24, following approval by JFSA, with the stablecoin available to institutional and retail users via SBI VC Trade.

Ripple has categorized RLUSD under Japan’s Payment Services Act as a new type of electronic payment instrument for foreign-issued stablecoins. This is the first time the company has had a regulated dollar stablecoin in one of its most established markets.

The day after the launch, Circle and Nomura plan to launch a USDC-based digital asset settlement and business payment service in Japan as early as 2027.

The service would allow Japanese businesses to exchange yen for USDC for supplier payments, transfers to foreign partners and currency payments, compressing cross-border transfers, which currently take two to three business days, into minutes.

According to BIS data, Japan’s foreign exchange market will handle $440 billion in daily transactions by 2025, a figure that puts real institutional weight behind the announcement.

Japan’s FSA-registered list of electronic payment instruments, as of June 24, shows SBI VC Trade processing USDC, RLUSD and JPYSC.

SBI launched RLUSD together with Ripple, distributed USDC starting in March 2025 and launched JPYSC the same week with SBI Shinsei Trust Bank overseeing the issuance and Startale as technical partner.

Ripple’s longtime Japanese ally has built a stablecoin shelf, and every major issuer is on it.

| Stable coin / project | Main Japanese partner | Currency exposure | Primary lane | Strategic implication |

|---|---|---|---|---|

| RLUSD | Ripple + SBI VC trading | USD | Cross-border payments, remittances, Ripple Payments flows | Ripple’s relationship with Japan will be a regulated dollar-stablecoin channel |

| USDC | Circle + SBI VC Trade; future Nomura service | USD | Exchange access, business currency, payments to suppliers, transfers abroad | Circle moves from listed access to institutional settlement |

| JPYSC | SBI VC Trade, SBI Shinsei Trust Bank, Startale | JPY | Large transfers, on-chain currency, institutional loans, RWA settlement | SBI is building a yen-denominated stablecoin avenue |

| Megabank stablecoins | MUFG, SMBC, Mizuho | JPY | Domestic B2B settlement and bank-directed payments | Institutional confidence could dominate yen settlement in 2027 |

Ripple’s Japan Position

SBI Group invested in Ripple in 2016; SBI Remit built money corridors on Ripple Payments after that investment; and XRP won retail exposure through SBI VC Trade at a depth unusual for blockchain assets outside Japan.

RLUSD extends that decade-long relationship by being the first regulated dollar stablecoin to be distributed through SBI’s existing payments infrastructure.

Ripple said RLUSD has reached a market capitalization of approximately $1.7 billion since its launch in late 2024. SBI VC Trade’s own announcement positioned RLUSD as the platform’s second US dollar stablecoin, joining USDC on the same shelf, with relationship history as a differentiator.

Cross-border payments, money transfers, and Ripple Payments flows are where that history translates into actual transaction volume, and those routes represent Ripple’s most defensible position in Japan.

The Circle and Nomura institutional track open

USDC arrived in Japan via SBI VC Trade in March 2025, with Binance Japan, bitbank and bitFlyer signaling future listings, allowing Circle to achieve exchange level distribution.

The Nomura partnership brings USDC to corporate bonds, vendor payment chains and FX settlement desks within Japanese companies, an area that stock exchange listings never reach.

A survey of 518 Japanese investment professionals by Nomura and Laser Digital found that 63% saw stablecoin use cases including treasury management, cross-border payments, crypto investing and tokenized securities settlement.

The same study found that stablecoins issued by major financial institutions received the highest trust ratings for the denominations of JPY, USD and EUR.

Ripple is positioning RLUSD around payments, cross-border liquidity and settlement infrastructure, the same institutional problem that gives Nomura Circle a bank-centric route to solve, with the institutional layer of trust that Ripple’s own brand just needs to earn in the Japanese corporate market.

The yen stablecoin floor

Reports indicated that MUFG, SMBC and Mizuho plan to jointly issue yen-based stablecoins during the fiscal year ending March 2027, with Japan’s FSA supporting the experimental phase.

That timeline parallels Circle and Nomura’s 2027 target and JPYSC’s current distribution through SBI VC Trade.

SBI and Startale call JPYSC Japan’s first trust-type yen stablecoin under the Electronic Payment Instruments Framework.

It focuses on high-value transfers, on-chain FX, institutional lending and tokenized RWA settlements, as well as business use cases where a yen-denominated instrument poses less currency risk to Japanese companies than a dollar-denominated instrument.

For domestic B2B payments and yen-to-yen settlement flows, bank-issued yen stablecoins have an institutional trust advantage that puts dollar stablecoins in a structurally weaker position.

If RLUSD drives meaningful transaction flow on cross-border corridors, connecting Japanese institutions to dollar liquidity faster than SWIFT rails, the SBI relationship will transform from a distribution asset to a revenue-generating payments infrastructure.

Ripple Payments already operates remittance corridors through SBI Remit, and RLUSD adds a regulated stablecoin layer to those rails that Circle, which arrives via Nomura with a 2027 target, has yet to build operations in Japan.

The bear case is for RLUSD to become a listed stablecoin without transaction volume supporting its position.

If Nomura activates USDC for corporate currencies before Ripple deepens RLUSD usage beyond SBI VC Trade listings, and if megabank yen stablecoins absorb domestic settlement flows, RLUSD will ultimately serve the cross-border and crypto settlement route that Ripple already had in place.

Meanwhile, the higher value corporate settlement market is consolidating around Nomura, Circle and the megabanks.

SBI’s position and the adoption test

SBI invested in Ripple in 2016, distributed USDC in March 2025, launched RLUSD in June 2026 and launched JPYSC the same week.

The FSA list showing SBI VC Trade processing all three stablecoins simultaneously makes SBI’s actual Japan strategy visible: a regulated multi-issuer access layer that captures distribution revenue, regardless of which stablecoin wins each use case lane.

SBI’s multi-stablecoin positioning gives Ripple guaranteed distribution and retail access through a regulated partner, and it puts Ripple in direct wallet-share competition with USDC and JPYSC on the same platform.

Four stablecoins now cover Japan’s regulated market: RLUSD on Ripple rail and cross-border dollar liquidity; USDC on access to foreign exchange and Nomura-backed business currency; JPYSC on yen-denominated institutional flows; and megabank stablecoins aimed at domestic settlement by March 2027.

| Use case job | Probably the strongest competitor | Why | Risk for Ripple |

|---|---|---|---|

| Cross-border transfers | RLUSD/Ripple Payments | Ripple has SBI history and remittance infrastructure | Low unless USDC is more readily accepted by businesses |

| Business FX Settlement | USDC + Nomura | Nomura brings bank-centric confidence and corporate distribution | High, because it overlaps with Ripple’s settlement distance |

| Domestic B2B yen payments | JPYSC / megabank stablecoins | Yen instruments reduce currency risk for Japanese companies | High, because stable dollar currencies are structurally weaker for yen-to-yen flows |

| Exchange liquidity | USDC and RLUSD | Both are on SBI VC Trade’s regulated stablecoin shelf | Medium, because listing alone does not prove transaction volume |

| Tokenized securities / RWA settlement | JPYSC / megabank stablecoins / USDC | Institutions may prefer bank-issued or bank-linked settlement assets | Medium to high depending on if RLUSD acquires institutional rails |

| Crypto-native settlement | RLUSD/USDC | Dollar stablecoins are of course for the liquidity of the crypto market | Medium, because USDC has a global scale |

Ripple has the SBI relationship, the payments infrastructure, and a decade of XRP-adjacent brand recognition that Circle and Nomura will be trying to replicate in Japan for years.

Circle has a dollar stablecoin scale, a banking partner with institutional trust credentials, and an enterprise FX pitch that focuses on the highest-value payments problem facing Japanese companies.

Both are entering the adoption phase without proven transaction volume in Japan, which the market will decide.

The next 18 months, ending around Circle/Nomura and megabank 2027 launch targets, will determine whether Ripple’s lead translates into a sustainable position in payments infrastructure or whether Japan’s stablecoin market consolidates around institutional trust and bank distribution.