Ethereum’s decline to its lowest level in more than a year is testing Wall Street trading, sending the token deeper into institutional portfolios.

Data from CryptoSlate shows that the second-largest cryptocurrency fell to $1,506 in the past 24 hours, its weakest level since April 2025, continuing a broad crypto sell-off that has already deleveraged derivatives markets and pushed traders toward defensive positioning.

Crucially, the downturn is not limited to ETH’s spot market, as the digital asset is also experiencing a broader deterioration in regulated ETF flows, centralized currency deposits and derivatives positioning.

This situation comes at a time when broader sentiment in the crypto market has weakened significantly, with Bitcoin falling to a four-month low near $60,000, while Ethereum has wiped out much of its market support.

ETF outflows weaken Ethereum’s institutional bid

The pressure has been most visible in the ETF market, where the products that gave institutions a regulated way to buy Ethereum have turned into a source of continued outflows.

Data from SoSoValue shows that spot ETH ETFs have recorded four consecutive weeks of withdrawals totaling more than $870 million.

During that period, the funds posted a 17-day outflow streak, interrupted by just one day of inflows, as investors added $19.3 million.

As a result, data from sosoValue shows that total Ethereum ETF assets have fallen by more than 70% from their peak of $30 billion to $8.71 billion, which is equivalent to approximately 4.01% of Ethereum’s circulating market cap.

The reversal has weakened one of the main arguments behind Ethereum’s institutional expansion. The ETFs were expected to broaden access to the asset, deepen liquidity and provide traditional investors with a cleaner way to gain exposure without dealing directly with tokens.

However, that demand has waned as the price of ETH has fallen and investors have reduced risk on digital assets.

The inflow of foreign exchange adds another supply risk

As institutional forces on the demand side waned, the physical supply available on liquid trading platforms experienced a sudden and substantial expansion.

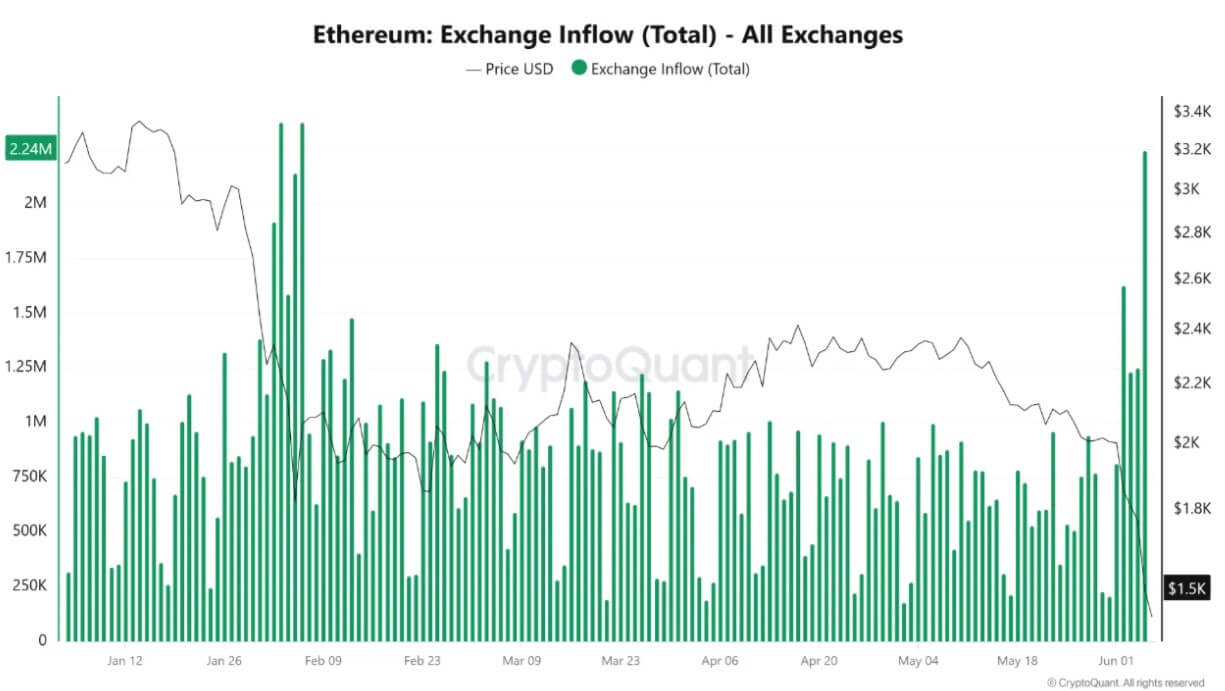

Data from CryptoQuant shows that Ethereum inflows into trading platforms rose to around 2.24 million ETH in a single day, the highest level in four months. Binance was responsible for over 1.16 million ETH of this inflow, representing more than half of the total.

This increase in active supply can be seen in high-profile moves along the chain that served as striking evidence of the liquidity migration.

Notably, a wallet linked to Ethereum co-founder Joseph Lubin woke up after more than three years of dormancy and mobilized 80,001 ETH, worth approximately $122 million.

The massive transfer epitomized the broader trend of long-idle capital breaking away from cold storage and seeking active trading platforms and liquid architectures amid mounting market stress.

A large inflow to trading platforms does not automatically mean that investors are selling. They may reflect market-making activities, collateral movements, internal transfers or portfolio restructuring during periods of stress.

However, traders keep a close eye on the metric because coins held on exchanges are easier to sell or use in derivatives activities than coins held in private wallets.

The timing has made the increase harder to ignore. Ethereum was already trading around $1,580 when inflows accelerated, while Bitcoin had fallen towards $59,000. That combination suggested that investors were moving assets during a market-wide reset rather than during a routine repositioning period.

If currency deposits remain high, the market may experience additional short-term volatility.

Deleveraging derivatives deprives the market of rebound capital

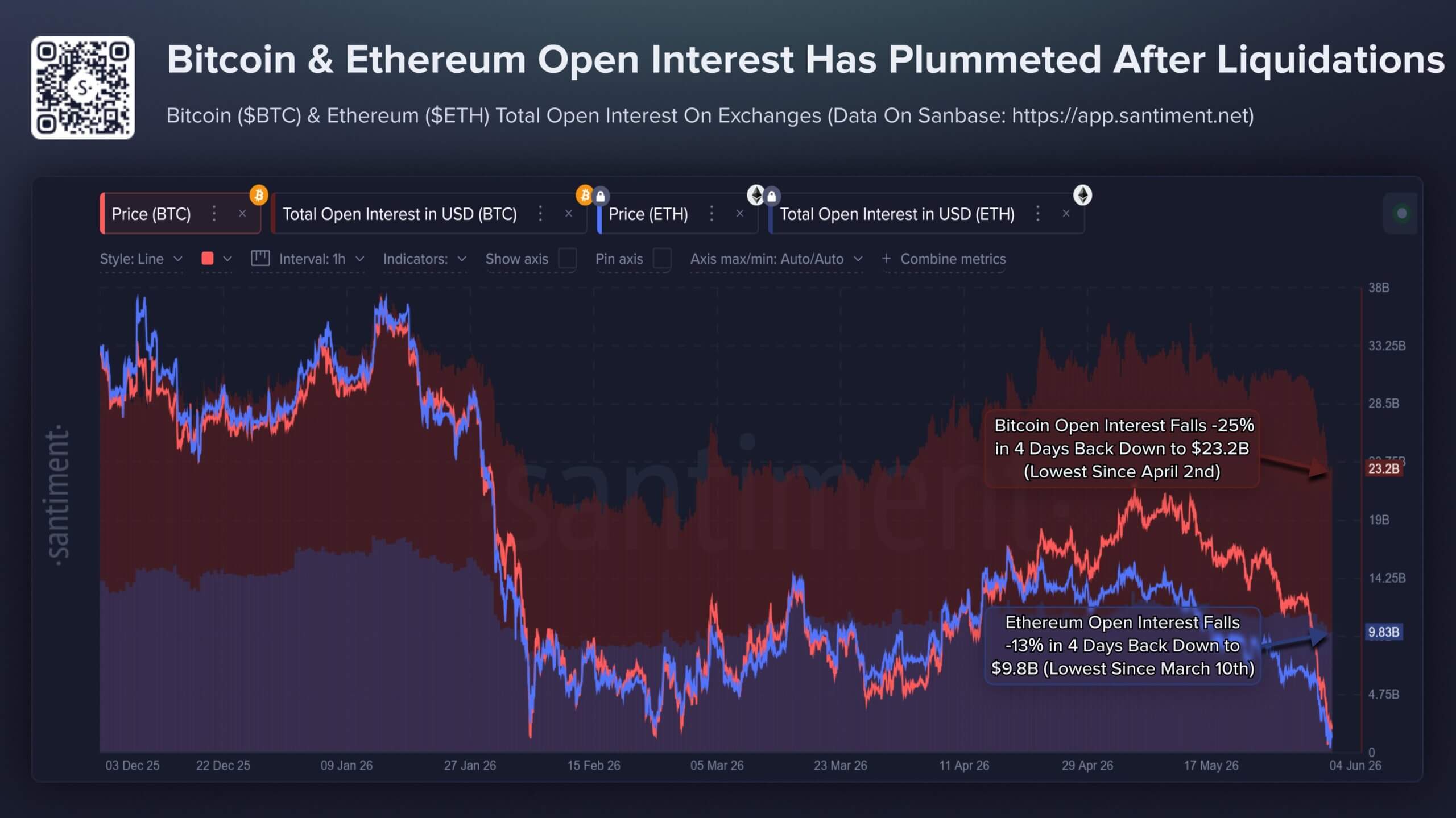

The pace of the crypto market’s current decline has been accelerated by an extensive cycle of deleveraging on leveraged futures platforms.

As spot valuations rapidly deteriorated, automated liquidation engines on major exchanges systematically closed underwater long positions to protect the integrity of the clearinghouse, amplifying organic selling pressure.

Data analyzed by Santiment illustrates that this liquidation wave effectively washed away a huge block of speculative capital over a narrow four-day window:

- Bitcoin Total Open Interest: Shrunk by about 25% and dropped to $23.2 billion, which is the lowest operating total since early April.

- Ethereum Total Open Interest: fell 13% to reach $9.8 billion, a structural low not seen since March.

While this aggressive deleveraging makes the underlying market structurally sounder by eliminating speculative surpluses and excessive margins, it creates an immediate liquidity vacuum.

The severe drop in open interest shows that the speculative floor has thinned out, leaving the market highly vulnerable to further spot pressure due to the lack of immediately available leverage capital to drive a classic V-shaped recovery.

As a result, retail sentiment has fallen to its most pessimistic level since mid-February.

The company noted that social statistics show an exponential increase in the phraseology of capitulation, with organic social discussions increasingly combining terms like “Bitcoin” and “altcoins” with terminal descriptors like “dead,” “finished,” “over,” and “finally.”

Traders are hedging for a break below $1,500

The increasing tension on ETFs, currency flows, whale cost bases and leveraged markets has shifted attention to ETH’s options market, where traders pay more to protect against another leg lower.

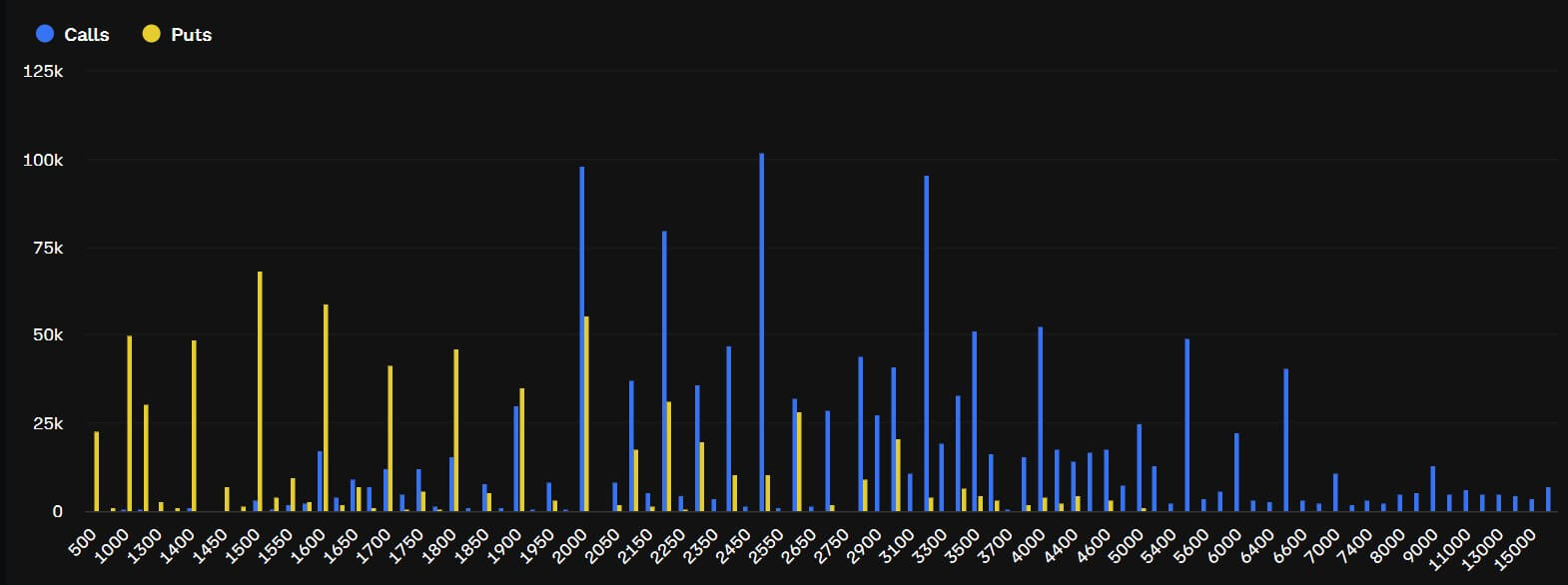

Deribit facts show that the demand for downside protection has increased sharply. The put-to-call premium for ETH options rose to 3.7 times on Friday and has shown consistent excess demand for put options since Monday. Put contracts give holders the right to sell at a fixed price, making them a common hedge when traders expect further losses or want protection against a disorderly move.

ETH’s open interest has clustered around several downside strikes. Traders have accrued approximately $108 million in open interest around the $1,500 strike, while the $1,400 strike has generated approximately $75 million. The $1,000 strike has generated approximately $78 million in positioning.

These levels do not mean that the market expects ETH to drop to $1,000 immediately. Instead, they show traders paying for protection after several support signals weaken simultaneously.

BlockScholes facts show that the shift has also taken place in volatility prices. ETH’s short-term implied volatility has risen from a year-to-date low of 36% to 67%, indicating that traders are now expecting larger price swings in the short term.

This move was accompanied by a sharper trend towards out-of-the-money puts. The seven-day ETH options skew has risen to around -14%, compared to around -3% to -4% at the end of May. Furthermore, demand for puts has also spread across 7-day, 14-day, 30-day and 90-day maturities.

This broadening shows that traders are not just covering a single event or short-term move. They are preparing for the possibility that Ethereum’s weakness could spread if ETF outflows continue, currency market inflows remain high, and large holders remain below key cost levels.

The next test is whether $1,500 becomes a bottom or a trigger. A stabilization of ETF flows and a decline in FX deposits could help alleviate pressure.

Without that, the options market’s focus on downside strikes could become the clearest signal of where traders expect the next phase of the sell-off to concentrate.