Bitcoin is now down 50% from its all-time high, a correction that wiped out about $988 billion in market value between October 2025 and April 2026.

The prolonged downturn has been caused by a combination of market-specific and macroeconomic factors. The sell-off gained momentum after October’s $19 billion liquidation, which triggered a broader capitulation phase in the crypto market.

Since then, several headwinds have emerged at various points in the cycle, limiting Bitcoin’s ability to sustain any meaningful recovery despite periods of renewed capital inflows.

The capital outflow indicates increasing caution among investors

One of the first signs that Bitcoin [BTC] The broader correction was far from over in the US spot Bitcoin ETF market, which serves as a key indicator of institutional and traditional investor sentiment.

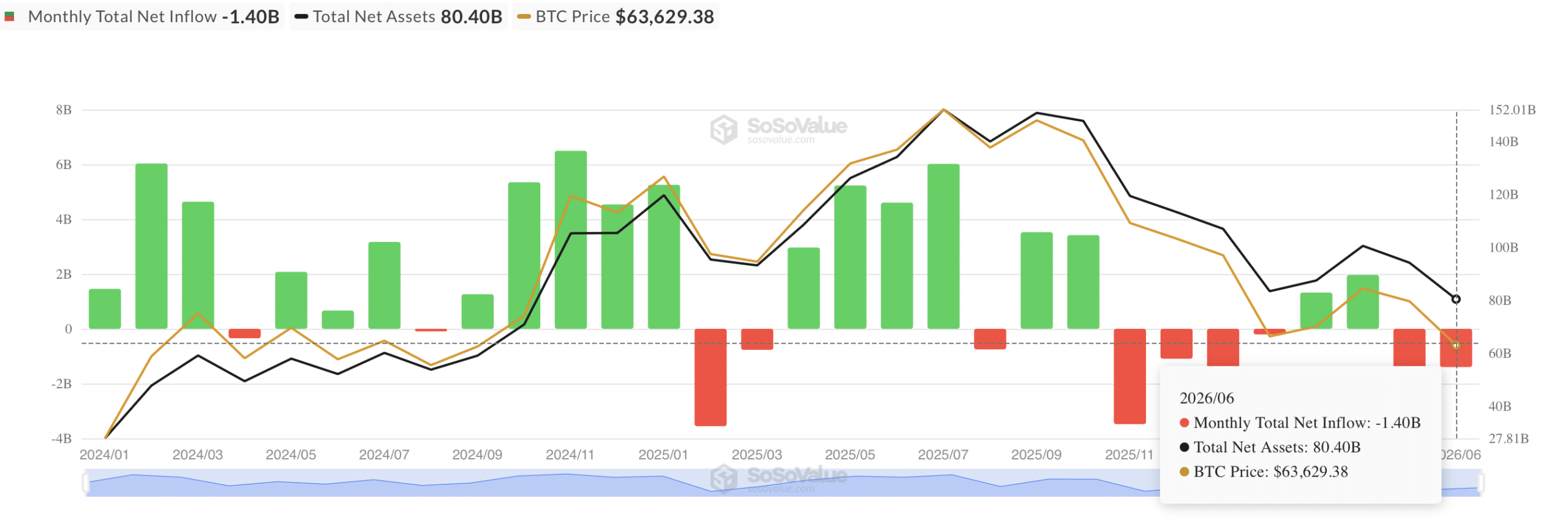

According to data from SoSoValue, US spot Bitcoin ETFs recorded net outflows totaling $3.83 billion between May 1 and June 4.

This figure exceeds the net inflows of $3.29 billion recorded in March and April combined, indicating that investors have not only reversed their previous accumulation efforts but have also begun to actively reduce their exposure.

The magnitude of these outflows indicates a notable deterioration in market sentiment. Institutional investors appear to be becoming increasingly cautious, with many banking on the possibility of a further downturn rather than a near-term recovery.

Macroeconomic conditions have increased the pressure. At the time of writing this article, concerns about unresolved tensions between the United States, Iran and Israel continue to weigh on financial markets.

With no clear indication that a lasting solution is imminent, investors remain reluctant to increase their exposure to volatile assets like Bitcoin.

The risk-off rotation continues

The recent capital flight from Bitcoin also appears to be linked to a broader rotation into traditional financial markets.

Investors are repositioning ahead of a busy mega-IPO window led by Elon Musk’s SpaceX and Anthropic, the company behind Claude.

SpaceX has filed its S-1 and is targeting a Nasdaq debut on June 12 under the ticker SPCX, pricing shares at $135 to raise about $75 billion at a valuation of about $1.77 trillion — the largest IPO ever.

This shift has accelerated capital rotation between asset classes. At the same time, traditional stocks continue to outperform.

The S&P 500 is up more than 11% this year and recently hit a new all-time high of 7,629.80.

Bitcoin, meanwhile, remains under pressure as investors increasingly favor assets seen as offering stronger risk-adjusted returns in an uncertain macroeconomic environment.

While Bitcoin and the S&P 500 have historically shown periods of positive correlation, their performance has diverged widely in recent months.

While the US benchmark index continues to rise, Bitcoin is down about 29% this year, underscoring the extent to which investor confidence has shifted away from speculative assets.

Bitcoin is at risk of further declines

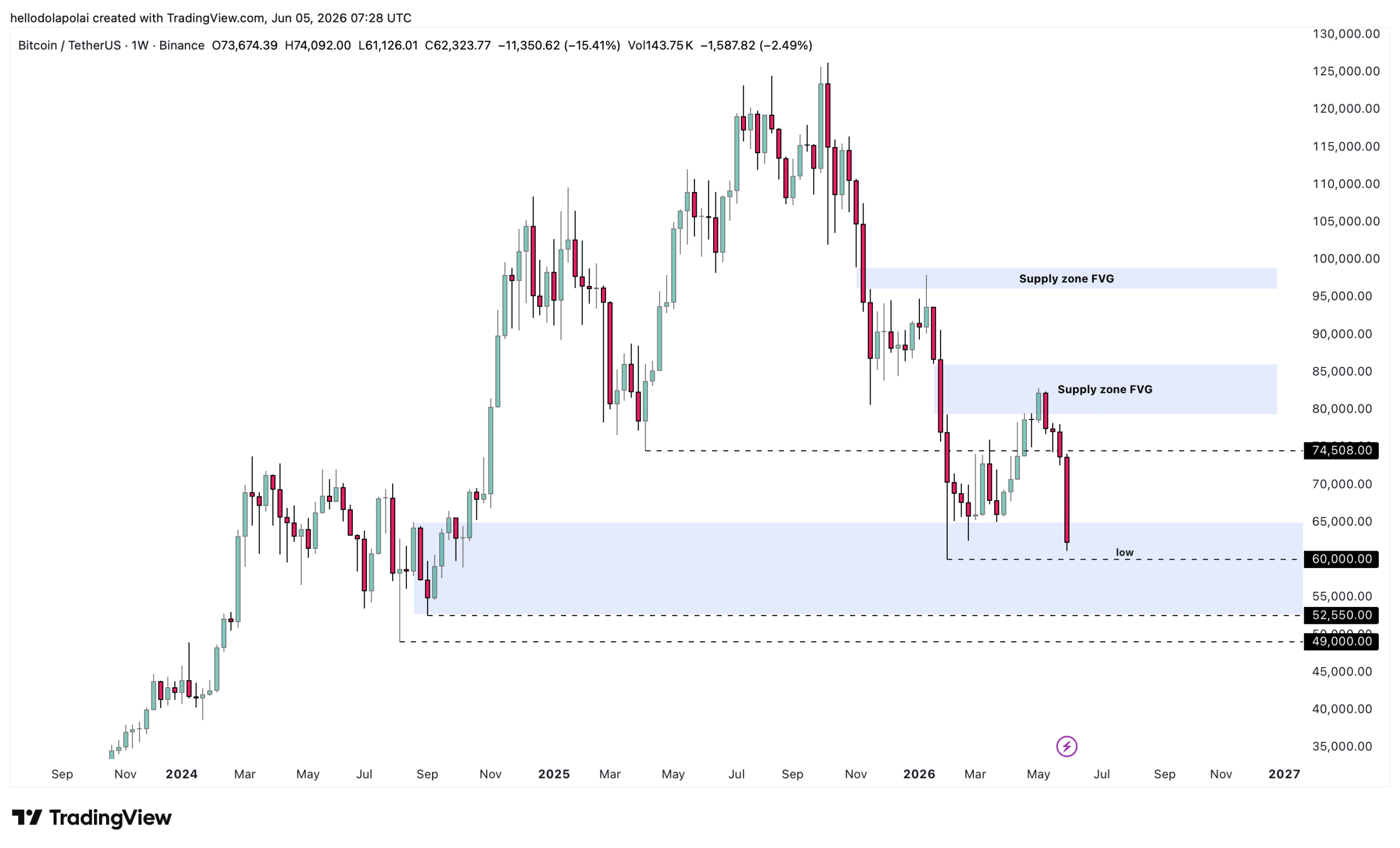

From a technical perspective, Bitcoin’s market structure continues to favor the negative side.

A weekly close below the $60,000 support wick, followed by a sustained bearish follow-through, would significantly increase the chances of a deeper correction.

In such a scenario, Bitcoin could revisit the $52,000-$53,000 range, a region that aligns with key support levels in the broader chart structure.

Right now, Bitcoin remains within what can be interpreted as a long-term accumulation zone, marked by the big blue box on the chart.

However, accumulation ranges do not guarantee upward resolution. Should selling pressure continue to exceed demand, the bears could force the asset to the lower end of that range, near $52,550.

Final summary

- Bitcoin has fallen nearly 50%, wiping out about $988 billion in value, as ETF outflows and geopolitical tensions weigh heavily on investor sentiment.

- The market rotation towards alternative assets is reinforcing bearish pressure, raising concerns that BTC could experience greater losses in the near term.