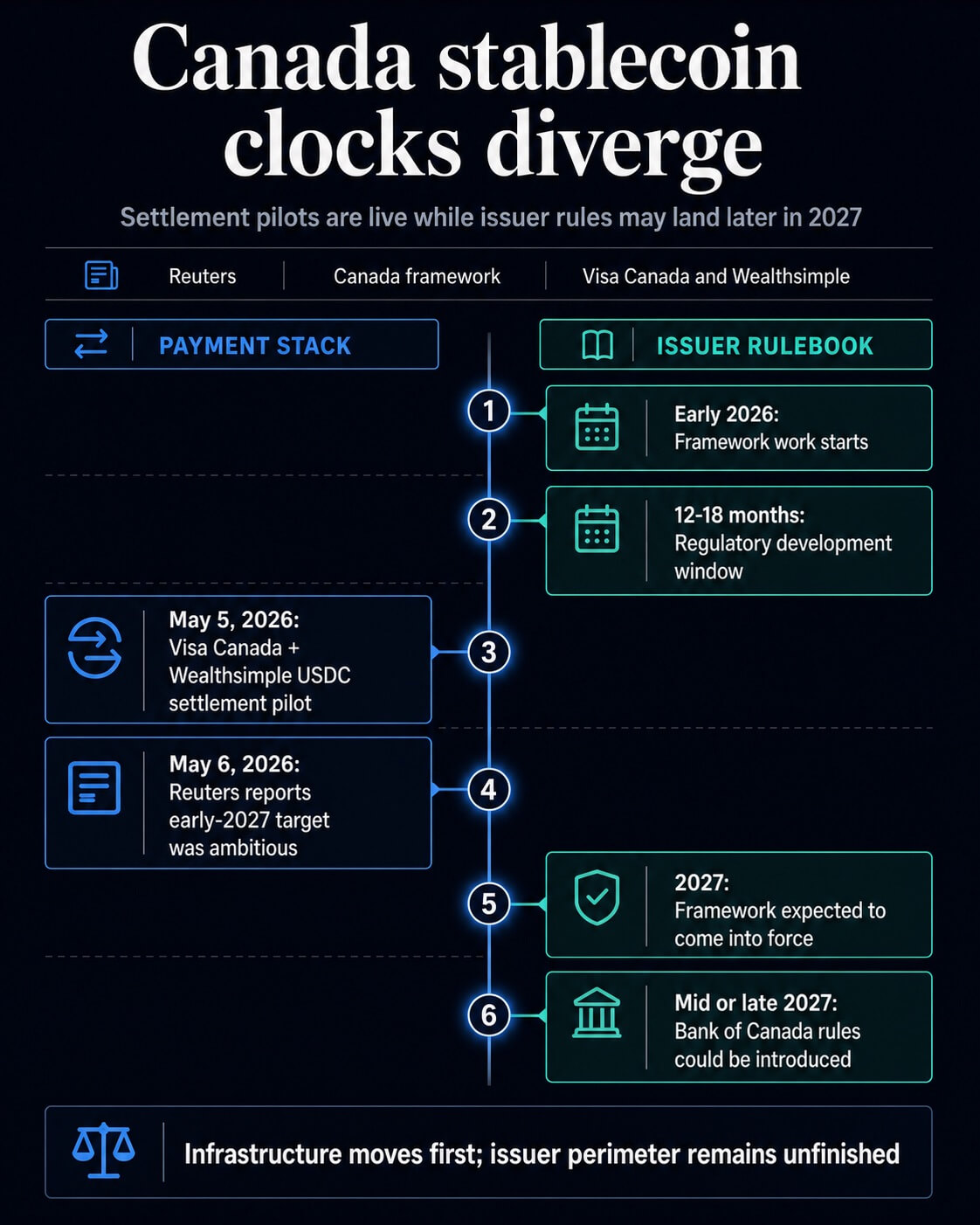

Stablecoin regulations from the Bank of Canada could arrive in mid-to-late 2027, bringing the detailed rulebook later in the same year that the Canadian government has already flagged for the framework to come into effect.

That timing comes just as Visa Canada and Wealthsimple are piloting USDC settlements for certain card network obligations in Canada. The result is a live institutional use case in part of the payments stack, while the framework for non-bank stablecoin issuers is still unfinished.

A Reuters report said an early 2027 launch plan was ambitious and regulations could instead be introduced in mid-to-late 2027. Canada’s own stablecoin framework already set a broader 2027 window, saying regulatory development was expected to continue for 12 to 18 months from early 2026 and the framework would come into effect in 2027.

The gap creates a planning problem for issuers and fintech partners. Companies considering Canadian exposure still need to prepare for registration, reserves, redemption mechanisms, governance controls, risk management and product economics around return limitations.

At the same time, payment networks and major fintech platforms can test stablecoin settlements against defined liabilities before each issuer rule is finalized.

Regulation moves faster than regulations

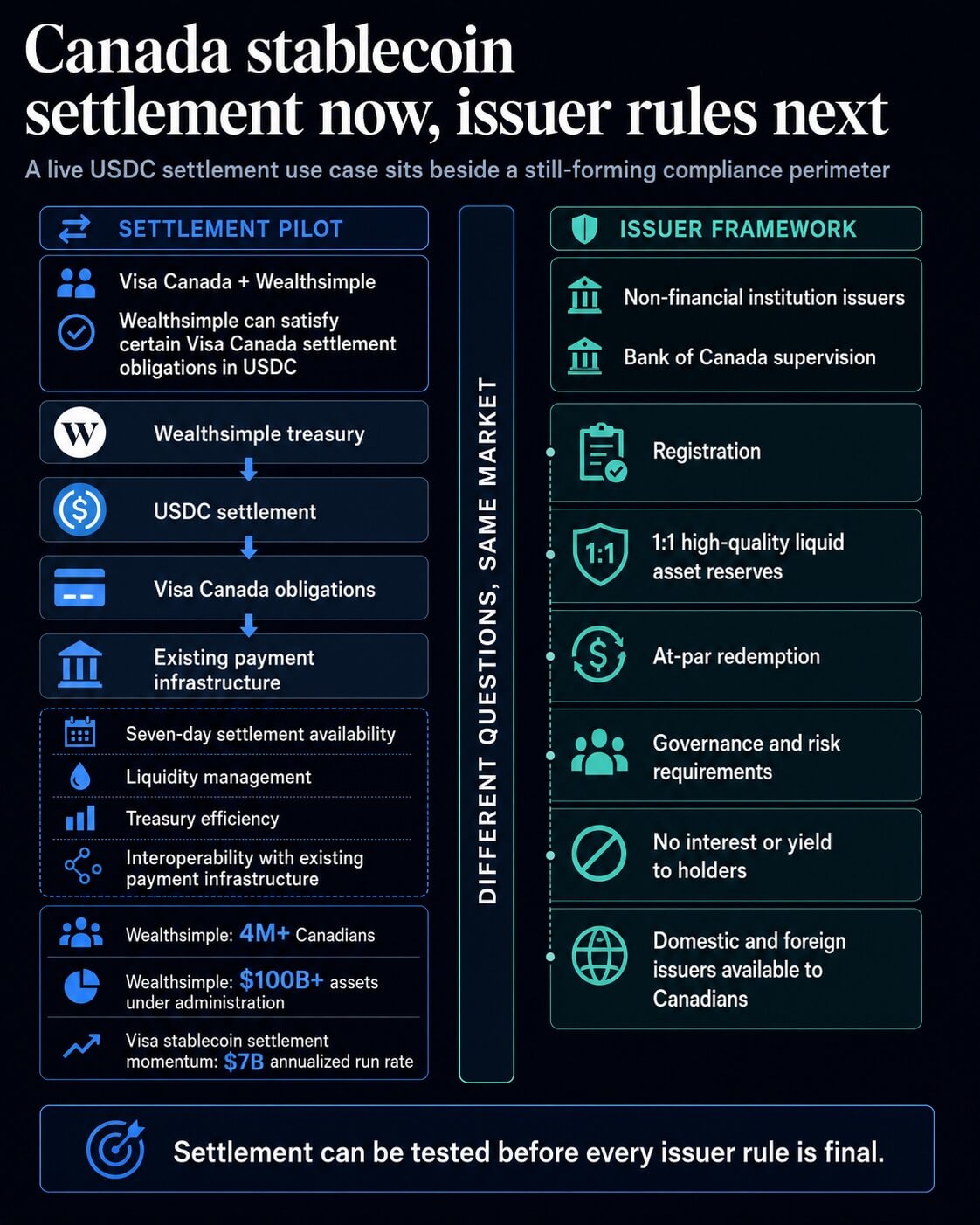

Visa Canada and Wealthsimple said their pilot will enable Wealthsimple to meet certain Visa Canada settlement obligations using USD Coin. The announcement detailed that stablecoin settlement would be coming to the Canadian market through Visa’s pilot and noted the availability of seven-day settlement.

The release also tied the launch in Canada to treasury and liquidity management. Stablecoin settlement can give a fintech more flexibility when it comes to when its obligations are met, how liquidity is positioned, and how treasury operations interact with the existing payments infrastructure.

For a company like Wealthsimple, which according to the release serves more than four million Canadians and oversees more than $100 billion in assets under management, these back-office mechanisms can impact liquidity planning even if retail users never see the settlement rail.

The Canadian pilot extends a broader Visa strategy CryptoSlate covered last week. Visa had already announced a stablecoin settlement pilot that includes nine blockchains and an annualized settlement rate of $7 billion.

The new Canadian link adds a named local partner and a specific settlement function to that global infrastructure story.

| Area | What is live or announced | What remains unresolved |

|---|---|---|

| Settlement | Wealthsimple may use USDC for certain Visa Canada settlement obligations. | The resulting announcement does not provide a Canada-specific settlement volume. |

| Publisher’s Rules | Canada has published framework expectations for fiat-backed stablecoins. | Detailed regulations could arrive in mid-to-late 2027, according to Reuters. |

| Market scale | CryptoSlate’s market pages showed stablecoins with a sector market cap of around $300.78 billion, while USDC was around $78.31 billion. | These figures show the scale of stablecoins rather than the demand for Canadian settlements. |

Visa Canada and Wealthsimple describe a defined pilot rather than a nationwide rollout for consumers. The release says Wealthsimple can fulfill certain obligations with Visa Canada in USDC; the final Canadian issuer framework will answer a different set of questions about who can issue fiat-backed stablecoins in the Canadian market and under what conditions.

The rule book still carries a heavier load

The Canadian framework focuses on fiat-backed stablecoins issued by non-financial institutions. The government page says issuers would be regulated by the Bank of Canada and face requirements such as registration, one-for-one reserves in high-quality liquid assets, redemption at par, governance controls, risk management and a ban on offering interest or returns to holders.

These requirements extend into the operating model. A non-bank issuer planning Canadian distribution must design reserve composition, redemption channels, governance controls and product terms around a ruleset that is still being drafted.

A move from early 2027 to mid or late 2027 could shift when those decisions become binding and how much flexibility companies retain while they wait for details.

The scope also keeps USDC relevant even though the Canadian framework is domestic. The government page says the framework applies to domestic and foreign issuers that make fiat-backed stablecoins available directly or indirectly to Canadians, and that it does not distinguish between Canadian dollar-denominated and foreign currency-denominated stablecoins.

For a USDC pilot, the final rules could shape how issuers think about Canadian availability, even if the Visa-Wealthsimple scheme itself remains a defined settlement program.

Canada has already seen questions about stablecoin compliance impact market access. CryptoSlate previously covered Circle’s Canadian stance after USDC met Canadian virtual crypto asset listing requirements, while the Bank of Canada’s framework would move that history to a more formal issuer regime.

The strongest signal now is whether Canada can align a formal issuer regime with pilots with payment networks that have already proven stablecoins are useful for settlement, treasury and liquidity transactions.

CryptoSlate market pages showed stablecoins with a combined sector market cap of about $300.78 billion, USDC of about $78.31 billion and USDT of about $189.61 billion. These figures give the policy debate its scope, while the question specific to Canada is how much institutional resolution activity will develop before the issuer framework is fully detailed.

From here, two paths are plausible. In one, Canada is finalizing the rules in time to allow issuers and partners to plan 2027 launches around a clear registration and reserve regime, while keeping settlement pilots limited but operationally useful.

Otherwise, detailed rules will come later in 2027 and companies will have to choose between waiting for certainty, setting up adaptable compliance systems, or maintaining Canadian exposure within partner-led arrangements.

Later, the Bank of Canada or the government will need to clarify how the mid- to late-2027 timing translates into regulatory release, legal force and practical compliance expectations. Until then, Canada has a living example of institutional USDC settlement and an unfinished issuer rulebook that moves on different clocks.