Senate Banking is targeting the second half of April for an increase in the Digital Asset Market Clarity Act, with an Easter recess through April 13.

Senator Cynthia Lummis publicly confirmed the timetable, and Senator Bernie Moreno made the deadline clear: missing the Senate floor in May could push serious digital asset legislation past the 2026 midterm cycle and close the window.

The five-step route, from Banking Committee elevation to floor vote, conference with the Agriculture Committee version, final passage, and President’s signature, compresses the bill’s timeline to a few weeks.

The stablecoin yield dispute that canceled January’s markup now has a resolution in principle.

Senators Thom Tillis and Angela Alsobrooks reached an agreement that Lummis said was 99% resolved. The framework would ban passive returns on stablecoin holdings, while allowing activity-based rewards tied to payments, transfers, wallet usage, and similar functions.

Alsobrooks described the compromise as one that would make both sides “a little bit unhappy.”

Senators still need to resolve new complications regarding the deregulation of community banks, ethics provisions for crypto-linked officials, and the handling of DeFi before they can lock down the markup text.

The House passed CLARITY 294-134 in July 2025, and the GENIUS Act became law the same month. The White House established the Strategic Bitcoin Reserve by executive order in March 2025.

The SEC and CFTC jointly clarified the treatment of crypto on March 17. Together, these steps show the US building a policy stack that sorts digital asset models by how well they fit within the US financial system.

| Date | Event | What it added to the policy stack |

|---|---|---|

| July 2025 | House passes CLARITY, 294–134 | Establish a federal market structure framework in one room |

| July 2025 | GENIUS Law becomes law | Created the federal stablecoin framework and narrowed stablecoins into payment utilities |

| March 2025 | The White House establishes the Strategic Bitcoin Reserve by executive order | Gave Bitcoin formal policy symbolism within the US digital asset agenda |

| March 17, 2026 | SEC and CFTC jointly clarify the treatment of cryptocurrencies | The sorting logic for raw materials and effects behind CLARITY has been strengthened |

| Objective second half of April 2026 | Bench markup in the Senate | Opens the way for the Senate to close the largest remaining gap in the legislation |

| Emergency period from May 2026 | Deadline for the Senate floor, according to the wording of the article | It compresses the path of the bill into a narrow political window |

CLARITY would close the biggest regulatory gap in that architecture, and Bitcoin is at the top of that hierarchy.

According to Senate Banking’s own formulation, the bill would draw a clear line between digital asset securities and digital asset commodities, replace regulatory enforcement with a rules-based regime, and give the CFTC authority over spot markets for non-security digital assets.

Bitcoin already occupies the commodity lane in market conventions, court rulings and political symbolism. CLARITY would give that position legal support and increase the policy weight of the Strategic Bitcoin Reserve.

What the stablecoin squeeze does for Bitcoin

The stablecoin architecture now taking shape points toward a payment utility.

The GENIUS Act requires 100% reserve support, monthly disclosures, and marketing rules that exclude misleading claims about government support, insurance, or legal tender status.

Section 404 of the Senate CLARITY bill prohibits digital asset service providers from paying interest or returns solely for holding a payments stablecoin and blocks any marketing that describes stablecoin compensation as deposit-like, FDIC-insured, or risk-free.

Activity-based rewards tied to transactions and platform participation remain on the table. The familiar field of holding a dollar-pegged token and collecting revenue falls outside of what both laws allow.

That framework reshapes Bitcoin’s narrative position. As Congress channels stablecoins into regulated payments, Bitcoin is emerging more clearly as the investable risk asset in US crypto markets.

Stablecoins see greater transaction volume and usability within the framework. They lose the quasi-savings economics that could otherwise compete for capital alongside a Bitcoin position in the long term.

The market has already priced in that asymmetry in real time. Circle suffered a 20% sell-off when the stablecoin reward cap language surfaced.

Coinbase’s stablecoin revenue was $364.1 million in the quarter ended December 31, 2025, while Circle’s reserve revenue-linked business accounted for the bulk of the results. Traders viewed the compensation limits as a direct blow to those business models.

Bitcoin’s value proposition runs through scarcity and demand for commodities, a model that Congress leaves intact.

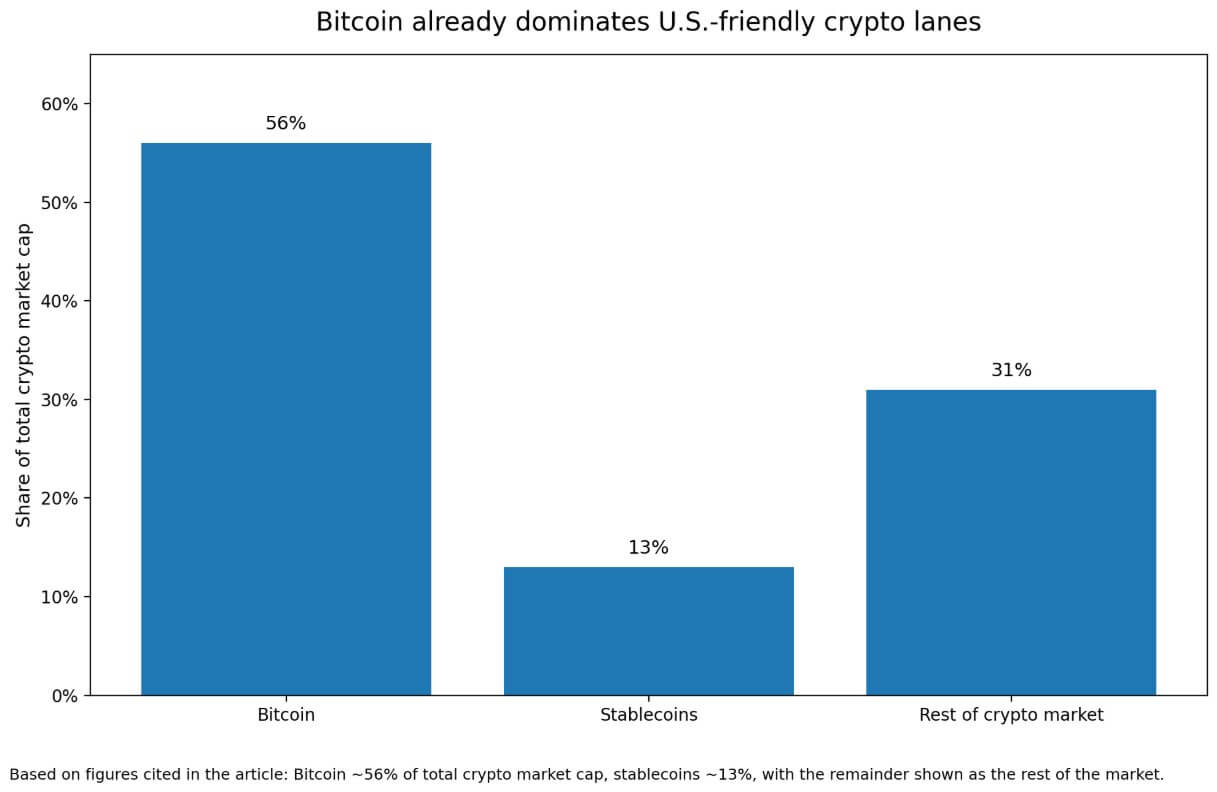

CoinGecko shows that Bitcoin accounts for about 56% of the total crypto market capitalization, while stablecoins represent about 13%.

JPMorgan analysts called the mid-year CLARITY passage a positive catalyst for digital assets, citing regulatory clarity and institutional scale. Polymarket estimated 2026 signing chances at 72%.

These readings reveal a market that expects a cleaner commodity designation will give institutions a cleaner rationale for Bitcoin exposure and formalize a pre-existing dominance structure.

What a markup represents

In a bull case, Senate Banking approves the bill in late April, with the full Senate considering it the final chapter of a coherent U.S. framework for digital assets.

Institutions read the SEC/CFTC’s bright line as a mandate to classify Bitcoin as a commodity for purposes of custody, portfolio construction, and product approval.

Bitcoin’s market capitalization stretches from the mid-1950s to around 60%, as capital concentrates in assets with the clearest legal and political fit. Stablecoins continue to expand as a payment infrastructure.

Congress limits its yield economics while preserving its transactional utility. Altcoins gain process clarity and lose the gray area optionality that once allowed projects to delay classification.

| Category | Taurus case | Bear case |

|---|---|---|

| Bitcoin | Obtains the clearest legal and political fit as a commodity; Market capitalization dominance moves towards 60% from the mid-1950s | Still outperforming the rest of crypto, but the broader market interprets CLARITY as selective rather than broadly bullish |

| Stable coins | Continue to expand as a payment infrastructure under a clearer federal regime | Growing in utility, but losing the economics that made them attractive as yield-related products |

| Stablecoin-linked shares | Benefit from long-term legal certainty and institutional adoption of regulated stablecoin rails | Keep the pressure on as pay and compensation caps cut into core business models |

| Altcoins | Gain process clarity and a cleaner route to classification and compliance | Facing stricter disclosure and intermediary standards that favor incumbents over smaller projects |

| Exchanges and intermediaries | Operate within a more readable rulebook that supports institutional participation | Lose a marketing tool tied to stablecoin rewards and face a heavier compliance burden |

| Institutional adoption | Gets a cleaner reason for Bitcoin exposure, custody and product approval | Remains selective and focuses first on Bitcoin and the most compliance-ready parts of the market |

| General market structure | Formalizes a US hierarchy: stablecoins for payments, Bitcoin for investable exposure, other cryptocurrencies deeper in the compliance funnel | Produces an uneven market in which Bitcoin gains legitimacy faster than the rest of the sector |

In the bear scenario, CLARITY passes and distributes the benefits unevenly. Stablecoin-linked stocks remain under pressure as compensation limits directly interfere with business models built around yield sharing. Trade fairs lose a marketing tool.

Altcoin projects face disclosure requirements and intermediary standards that favor incumbents over new entrants. Bitcoin is outperforming on a relative basis, while the broader crypto complex is trading sideways or weaker.

Circle’s sale offered a taste of how quickly that separation could hit the market.

Each outcome points to the same destination: Bitcoin leaves the process in a stronger position than the rest of the market. If CLARITY succeeds, Washington will have chosen which crypto asset can look legitimate first, and Bitcoin has the strongest claim to that role.