Bitcoin investors are buying protection around $50,000, while the flagship digital asset holds nearly $70,000 and has recently outperformed gold, the S&P 500 and the US dollar amid the ongoing war in Iran.

According to Crypto Slates Data shows that Bitcoin was trading at around $70,688 at the time of writing, meaning hedging around the $50,000 level means investors should guard against a drop of around $20,000 even if the spot price remains firm.

The contrast has become one of the clearest signals on the market. Spot Bitcoin has shown resilience during the initial phase of the conflict, but the derivatives market still shows traders paying for insurance against setbacks.

On Deribit, the latest public options flow note showed buying in the $50,000 to $60,000 put zone, along with put spreads in March and new downside structures following attacks on Middle East energy infrastructure and a surge in US producer prices.

That split suggests that investors are no longer treating Bitcoin as a one-way war trade. Instead, they weigh two outcomes at once.

One of these is that Bitcoin continues to absorb geopolitical tension better than many expected. The other is that the oil shock turns into inflation, pushing expectations for rate cuts further out and dragging risky assets down, forcing BTC back into the low $50,000s.

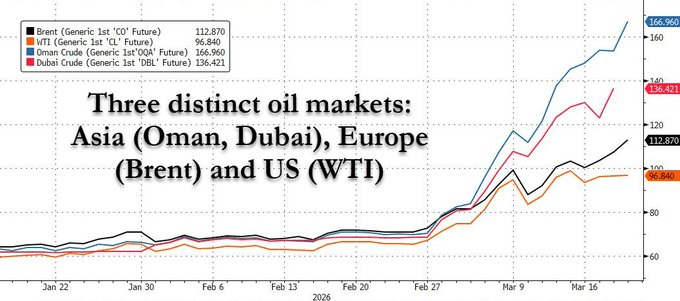

Middle Eastern crude is rising faster than Brent

Oil helps explain why that cover has stayed in place. Reuters reported Brent settled at $108.65 per barrel on March 19, after reaching an intraday high of $119.13, while West Texas Intermediate reached $100.02 before closing at $96.14. Brent later traded at $107.29 after hitting $119 the day before.

The Kobeissi Letter, a macro analysis platform, noted that the most serious step has taken place in the Middle East itself.

Dubai crude, a regional benchmark more closely tied to Gulf exports, reached $166.80 on March 19, according to the firm, while physical freight prices for crude oil and fuel also set records as the conflict over Iran disrupted shipments through the Strait of Hormuz.

Oil prices in Oman rose to $167 per barrel, while Brent remained around $113 and WTI traded around $97, leaving the gap between regional and global benchmarks at one of the widest levels in years.

That difference has changed the market’s interpretation of the oil shock. Brent remains the main benchmark, but the bigger tension is in Gulf-linked cargoes, where traders are assessing the immediate impact of disrupted shipping, lower exports and supply fears around the Strait of Hormuz.

The Kobeissi letter explained:

“When the war first started, US oil prices rose due to the uncertainty. However, when the Strait of Hormuz closed, markets began to reassess the risks. While the Strait of Hormuz is closed, approximately 18% of global crude oil supply is offline.”

So when the war premium moved from futures to physical barrels, the macro risk became harder for Bitcoin traders to ignore.

That would essentially shift the question for crypto investors from whether oil rises to whether the rise stays within global benchmarks or continues to feed through Middle Eastern freight markets, keeping inflationary pressures elevated for longer.

Why Traders Still Buy Downside Protection

That background is clearly evident in Bitcoin derivatives.

Deribit of March 19 remark described buying $50,000 to $60,000 puts and said downside protection was provided through risk reversal structures in April and December when the energy shock and inflation data came on tape.

The current market structure of the flow also adds nuance, with some of the recent downside positions manifesting in put spreads and risk reversals rather than outright crash bets.

This indicates a market that manages costs and defines risk, rather than simply creating panic. Investors are still paying for defense, but they are doing so with targeted structures around a specific lower range.

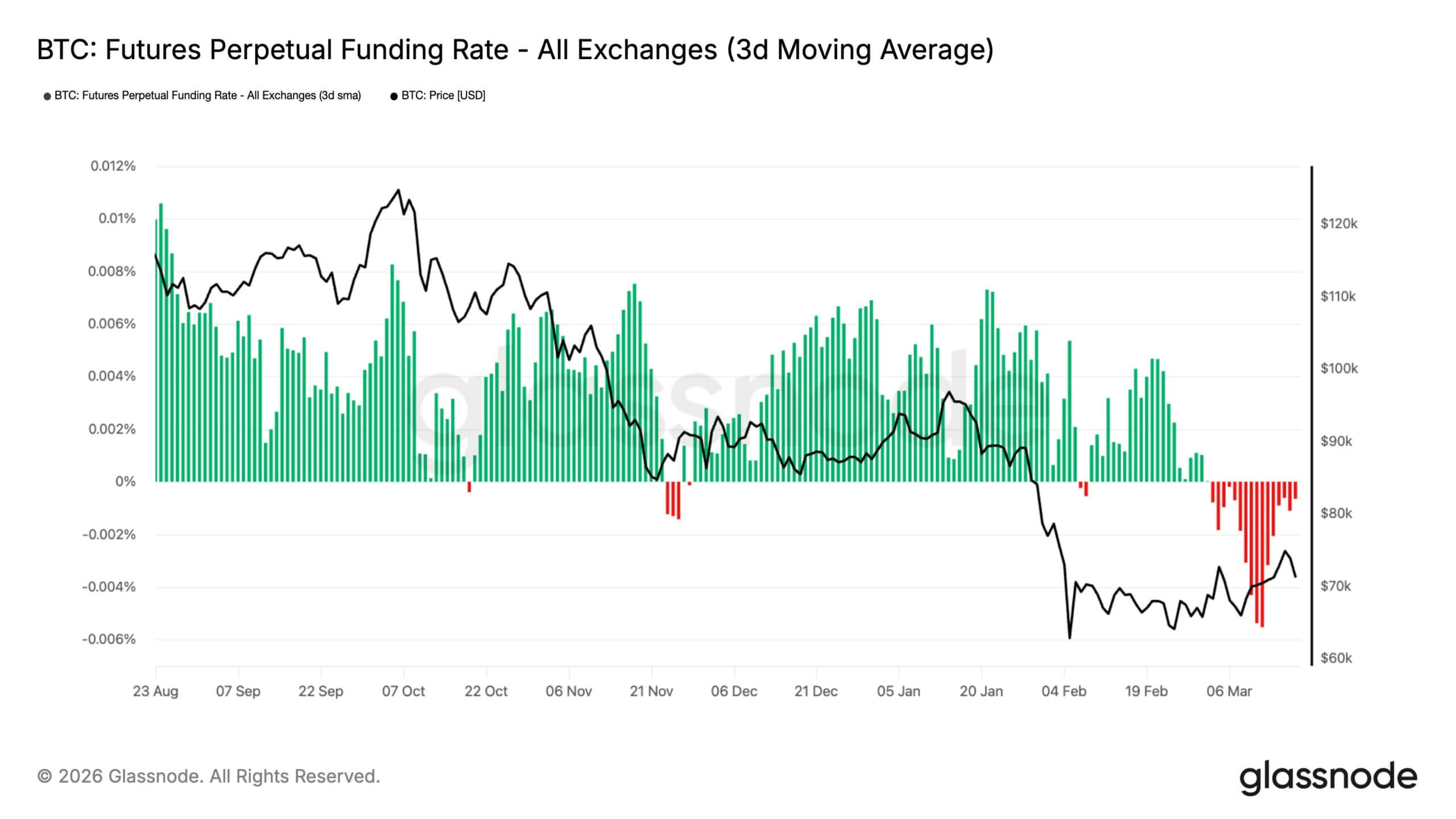

Meanwhile, broader derivatives data points in the same direction. K33 Research said CME Bitcoin futures open interest had climbed back above 110,000 BTC, while perpetual open interest was between 260,000 and 270,000 BTC.

It also said the seven-day average financing rate was -2.2% and the 30-day average was negative for 18 consecutive trading days, the longest streak since December 2022.

In practical terms, the futures and perpetuals markets are still leaning defensively, even as Bitcoin trades near the top of its recent range.

Deribit is weekly report with Block, Scholes showed the same caution about options. BTC’s at-the-money implied volatility was around 50%, its seven-day implied volatility was 52%, and the futures-implied yield curve remained flat at 2% to 3% across maturities.

The put-call skew had recovered from the late February low, but the surface still had not moved toward calls. So traders were no longer hunting for downside hedges at the same pace as earlier this month, but were still willing to pay for protection.

Glassnode’s positioning data reinforces that view, showing that perpetual funding remained firmly negative, while the directional premium remained bearish and the directional perp premium turned negative for the first time since 2022.

This means that traders were still shorting even after BTC’s recovery from recent lows.

What comes next for Bitcoin

The positive is that this positioning with many hedges becomes fuel for a tightness. Glassnode said the combination of crowded short positions, negative funding and stress on easing options leaves Bitcoin vulnerable to further upward pressure if spot demand continues to recover.

In this setup, the same defensive stance that now reflects caution could turn into forced buying as traders need to cover shorts into strong positions.

Meanwhile, CryptoQuant’s more constructive scenario points in the same direction.

The crypto analysis company said Daily demand from accumulator addresses remained high at 224,700 BTC, above the monthly average, while currency outflows reached 11,300 BTC in three days. At the same time, Coinbase Premium remained positive, indicating that US buyers were still active.

Under that view, institutions are absorbing liquidity while retail is selling into war headlines, creating the conditions for a bear trap rather than a collapse.

However, the negative scenario remains linked to a broader conflict and a more persistent inflation shock. CryptoQuant said that if the US sends more troops to Iran and the conflict escalates further, the Fed’s restrictive policies could remain in place longer.

In that scenario, BTC’s probability of a return to the February bottom rises near $60,000, with the final liquidation zone around $54,800.

For traders trying to time the next entry, the more useful signal may be less about headlines and more about positioning.

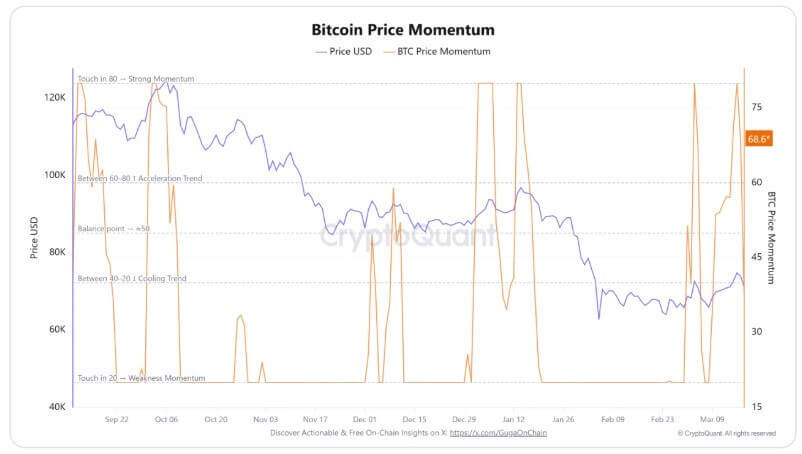

CryptoQuant’s framework posits that the price could continue to fluctuate between $69,000 and $65,000 amid heavy military tensions, with a clearer outcome only once the Bitcoin Price Momentum indicator returns to its equilibrium point near 50 and begins to show a reversal in the support region.