Bitcoin’s corporate bond boom is losing oxygen: A $100 billion bet on public companies has shrunk, buying has collapsed outside of Strategy (formerly MicroStrategy), and the financing model that powered the trade is starting to fail.

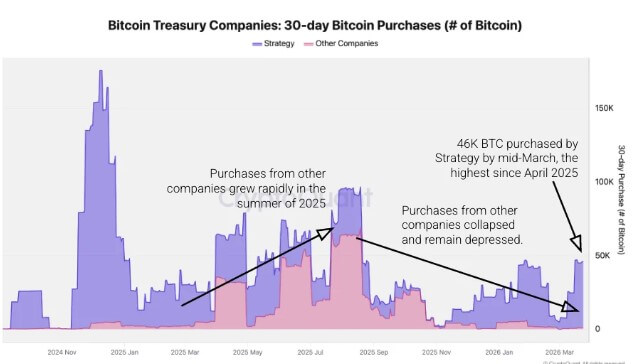

Data from CryptoQuant shows that the Michael Saylor-led company purchased approximately 45,000 Bitcoin in the past 30 days, the largest 30-day purchase since April 2025.

During the same period, all other Bitcoin Treasury companies together bought about 1,000 Bitcoin, down about 99% from the 69,000 BTC they bought at the peak of trading in August 2025.

CryptoQuant noted that the gap has grown so wide that Strategy now accounts for about 98% of all Bitcoin purchased by treasuries in the past month.

Last October, the balance sheet looked very different, with companies outside of Strategy accounting for about 95% of net purchases, at a time when corporate purchases were spreading across a broader list of names.

This shift has made Strategy the dominant source of increasing demand for government bonds in a sector that was only months ago promoted as a broader corporate movement linked to Bitcoin’s rally and the ability of listed companies to use their shares as financing instruments.

Participation shrinks further than Strategy

The slowdown outside of Strategy is reflected not only in the volume of purchases, but also in the number of companies still participating.

Treasuries other than Strategy have made 13 Bitcoin purchases in the past 30 days, down 76% from 54 in August 2025, when business activity was at its peak. Strategy, on the other hand, has maintained a steadier pace, making approximately 4 to 5 purchases each 30 day period.

The figures point to a market where both the depth and breadth of demand have weakened. There are fewer companies buying, and those that remain active are deploying less capital than during the peak of trading.

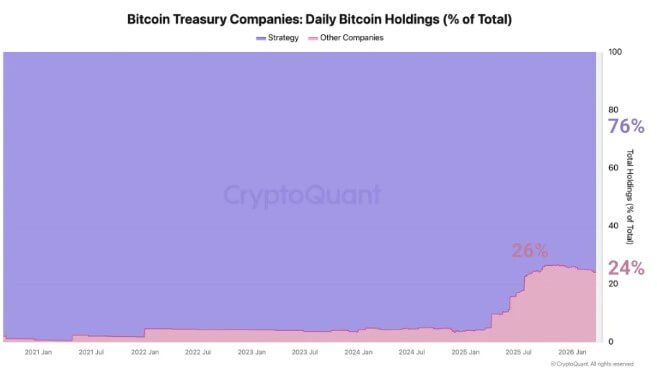

That change has changed the composition of the sector. While Strategy’s total Bitcoin holdings have grown by about 90,000 Bitcoin so far this year, other treasury firms have collectively added a net 4,000 Bitcoin over the same period.

As a result, their share of total corporate bond holdings has fallen from 26% in November 2025 to 24% today, while Strategy’s share has continued to rise.

Strategy now owns approximately 76% of all Bitcoin owned by treasury companies. The next two largest holders, XXI and Metaplanet, account for 4.3% and 3.5% respectively.

For an industry that grew rapidly as rising Bitcoin prices attracted newcomers, the concentration is becoming increasingly difficult to ignore.

A trade based on rising prices loses momentum

The corporate treasury model gained momentum last year as Bitcoin rose and public market investors rewarded publicly traded companies that offered leveraged exposure to the asset.

As Bitcoin rose, many companies were able to issue shares at a premium to the value of the BTC already on their balance sheets.

That gave them a way to raise capital, buy more Bitcoin and, in some cases, widen the gap between their market value and the underlying value of their holdings. It is notable that some also used debt financing to increase their exposure.

That structure worked well in a rising market. However, things became much more difficult when Bitcoin stopped growing and equity premiums narrowed.

Bitcoin’s price has fallen from an all-time high of $126,000 in October to around $70,000, wiping out much of the gains that had supported trading.

As prices fell, so did the intrinsic value of corporate interests. At the same time, stock valuations of many digital asset treasuries fell, reducing their ability to issue shares on favorable terms.

The result is therefore a tighter feedback loop in the industry, with a lower Bitcoin price lowering Bitcoin’s intrinsic value per share. This leads to lower share premiums, making the share issue less profitable.

Once these conditions are met, the same financing mechanism that has helped companies grow their Bitcoin holdings begins to lose effectiveness.

That pressure has hit government bond stocks hard. Stocks that traded as a high beta expression of Bitcoin’s upside have fallen sharply from their 2025 highs, many of which have underperformed BTC itself.

For companies that have bought heavily at the top of the market, such as Metaplanet, unrealized losses are starting to mount.

Stress arises throughout the sector

Meanwhile, signs of tension are beginning to appear in individual cases across the sector.

A recent example came from GD Culture, the publicly traded artificial intelligence and livestreaming company, which approved the sale of its 7,500 Bitcoin, worth approximately $503 million, to fund share buybacks and support the stock price.

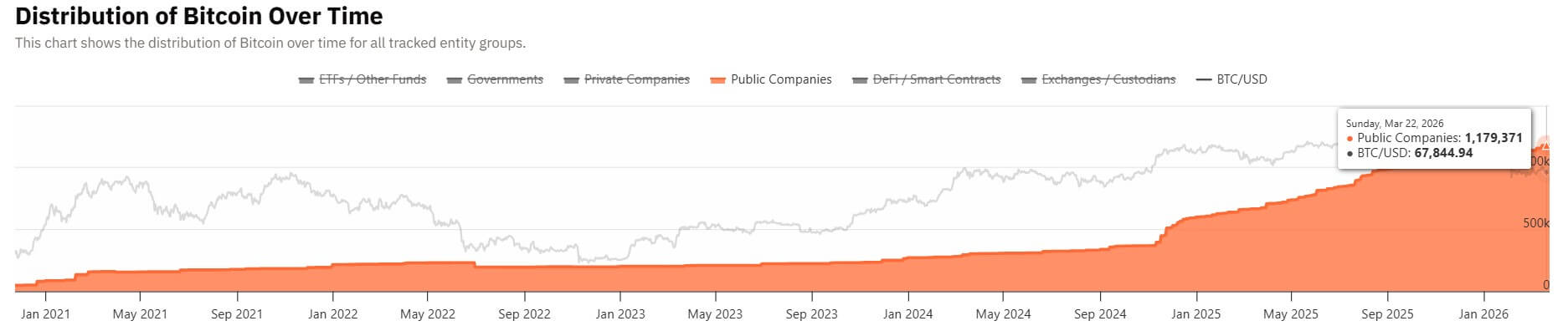

The industry’s overall figures also reflect the change in conditions. More than 100 publicly traded companies poured about $100 billion into Bitcoin last year as trading accelerated.

Those assets are now worth about $83.7 billion, according to the U.S. government Bitcoin Treasuries dataa sharp decline from their peak value.

At the same time, only two of the publicly traded companies that have Bitcoin on their balance sheets bought more of the asset in the past week, according to facts compiled by Hodl15Capital.

The slowdown suggests that, outside of a small number of committed players, the willingness to continue adding more exposure has waned with the market.

Even among companies that continue to present Bitcoin accumulation as a long-term strategy, activity has become more uneven.

Metaplanet, one of Japan’s best-known Bitcoin treasury companies, has raised 40.8 billion yen, or about $255 million, as part of a financing that could raise up to $531 million in total capital for Bitcoin purchases.

Yet it hasn’t made a Bitcoin purchase this year, even as it maintains a long-term goal of owning 210,000 Bitcoin. The company currently owns 35,102 Bitcoin.

The next phase looks more selective

Against that backdrop, research across the industry increasingly points to a tougher environment for companies that have built their strategies around stock issuance and rising Bitcoin prices.

Analysts at Galaxy Digital have done just that said The same financial technique that amplified the uptrend when valuations were high is now magnifying the downtrend as equity premiums contract.

For treasuries whose shares had functioned as leveraged crypto trades, softer markets and weaker risk appetite in public equities have changed the economics of the model.

Crypto research firm 10x Research too argued that the first phase of the bond-to-Government bond trade is already behind us, with the easy profits from rich premiums to intrinsic value no longer available to most companies.

In that environment, companies will likely face increased scrutiny over how much stock they issued at peak valuations, how much Bitcoin they bought around a cycle high and how much debt they took on to fund those positions.

Now a more selective phase is starting to take shape.

Galaxy Digital stated that companies with stronger balance sheets and more sustainable access to capital are better positioned to weather an extended period of flat or negative intrinsic value premiums.

Several Bitcoin treasury firms, including Strategy and Strive, are already using preferred stock options to fund new BTC acquisitions, with the aim of outperforming the top crypto over the long term.

On the other hand, others may have to scale back purchases, rethink capital strategy or defend shareholder support if equity markets remain unreceptive.