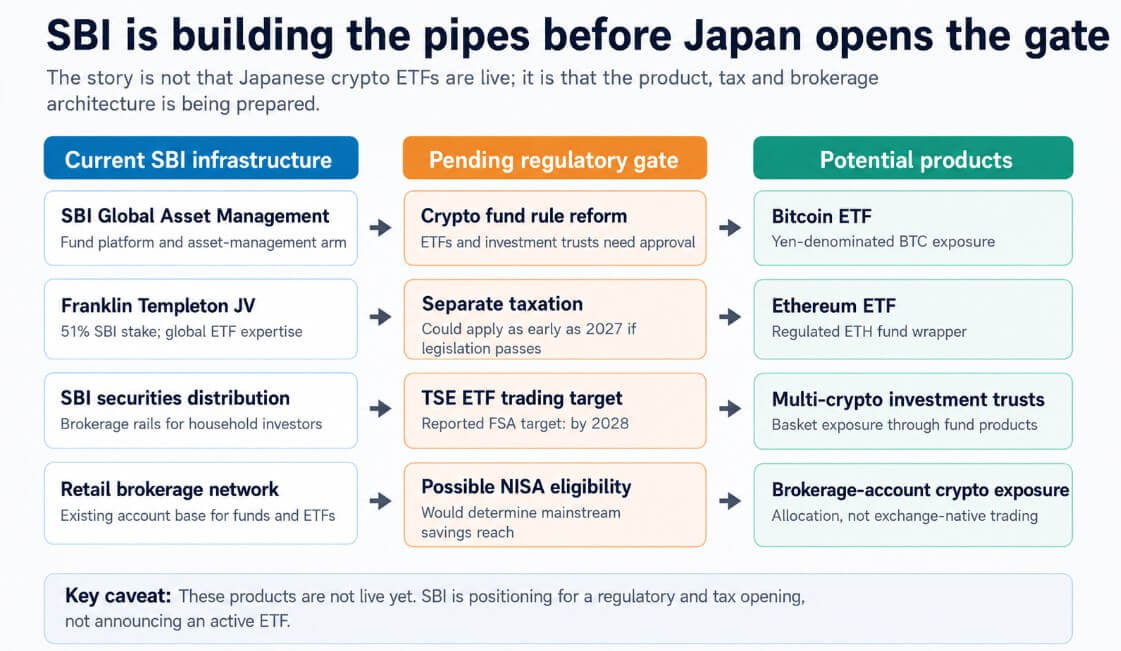

SBI Group has told investors that its asset management unit plans to launch ETFs focused on Bitcoin and Ethereum, as well as investment trusts holding baskets of multiple crypto assets, once Japan reforms its rules on crypto funds and taxes.

SBI has already built the architecture through a joint venture with Franklin Templeton, established product categories and set an AUM target of $31.5 billion within three years of launch.

SBI Global Asset Management Group’s assets under management exceeded $75.5 billion at the end of March 2026, with the firm holding a 51% stake in the Franklin Templeton business and managing a broader securities business with assets under management of more than $415 billion.

The crypto ETF products would be connected to that distribution network upon arrival, the kind that already directs millions of Japanese households to stocks, bonds and mutual funds.

The FSA is reportedly aiming to enable crypto ETF trading on the Tokyo Stock Exchange by 2028, and separate taxation could apply as early as 2027 if related legislation is passed.

Why Bitcoin ETF Japan Demand Matters

Data from the Bank of Japan shows that Japanese households held $14.8 trillion in financial assets at the end of 2025, of which 48.5% were in cash and deposits.

The government has pushed households toward investment for years, and Japan’s tax-advantaged investment package, NISA accounts, reached 28.26 million accounts and $447 billion in purchases by the end of 2025.

To achieve SBI’s target of $31.5 billion, an allocation rate of just 0.21% of total household financial assets would be required.

The number of Japanese crypto accounts has already reached approximately 14 million, almost half the number of NISA accounts, with customer assets of more than $31.5 billion.

Chainalysis recorded Japanese on-chain value rising 120% in the 12 months to June 2025, the strongest growth among major APAC markets. A fund wrapper would channel that existing demand through the brokerage and securities platforms where Japanese households’ broader savings already reside.

Hong Kong launched Asia’s first Bitcoin and Ethereum ETFs in April 2024, setting a regional precedent.

Japan would enter with a clear structural advantage, with a much larger domestic savings pool, an entrenched retail brokerage culture and large financial institutions already managing the daily investment behavior of millions of households.

The approval of the US spot Bitcoin ETF in January 2024 gave Bitcoin access to Wall Street balance sheets, registered investment advisors and institutional custody.

The Japanese version would give Bitcoin access to yen-denominated investment accounts, fund supermarkets, conservative household portfolios and a tax-favored savings infrastructure that already directs millions of ordinary investors to stock and bond funds.

US ETF flows made US trading hours the dominant regulated demand window, and Japanese ETFs would add a yen-denominated, Asia-hours denominated flow channel as a second regulated layer with its own institutional buyers, custody providers and broker incentives.

What needs to be done first

Proposed reforms could bring Japanese crypto profits the current ceiling of 55% up to 20%, which corresponds to the rate applied to stock trading.

SBI’s May 2026 report states that separate taxation could be introduced as early as 2027 if the legislation is passed. A regulated ETF with a 20% tax cap becomes a portfolio product.

In addition to taxation, the products require regulatory approval for ETF and investment trust structures, custody frameworks, benchmark construction, market maker depth and a decision by regulators on whether crypto funds can qualify for NISA-style tax-favored accounts.

That last question could determine whether cryptocurrency exposure reaches the same households currently purchasing domestic and foreign stock index funds through their NISA allocations.

Open savings trail or regulatory delay?

In the bullish case, crypto funds will receive a 20% tax treatment and become eligible for regular long-term brokerage accounts in 2027, and SBI and Rakuten will launch products through their combined distribution networks.

The $31.5 billion target falls within the three-year time frame, tapping into 14 million existing crypto account holders and brokerage investors who would never open a crypto exchange account.

Japan joins Hong Kong as a regulated source of ETF flows in Asia hours, and Bitcoin’s demand base expands into a second major currency and time zone.

Chainalysis’s 120% on-chain growth rate suggests that domestic appetite is already growing, and the ETF wrapper is channeling it through the securities infrastructure into regular portfolio allocations.

In the bearish case, ETF and investment trust rules slip past 2028, and tax reform delivers a framework that excludes crypto funds from NISA accounts.

Products are launching with a high-risk rating, which keeps them out of mainstream brokerage platforms and out of tax-favored accounts, and SBI reaches $3.1 billion to $12.6 billion, largely coming from existing crypto-native users migrating to a regulated wrapper.

Asia’s regulated crypto story remains focused on Hong Kong and offshore trading platforms, and the Franklin Templeton JV produces a credible product that only reaches a limited, already crypto-native audience.

| Scenario | What needs to be done | Result under management over three years | Market impact |

|---|---|---|---|

| Bull case: open savings rail | 20% tax treatment, ETF/trust approval, mainstream brokerage distribution, possible NISA style entry | ~$31.5 billion+ | Japan is becoming a major Asia-hours regulated Bitcoin flow conduit |

| Bear case: regulatory delay | ETF rules slip past 2028, crypto funds excluded from NISA, high-risk classification limits distribution | ~$3.1 billion – $12.6 billion | Products mainly serve existing crypto-native users; Locations in Hong Kong and offshore remain central |

SBI built the product architecture to accommodate the regulatory opening that set in motion Japan’s regulatory calendar.

The people who could invest meaningful capital in Bitcoin exposure in Japan could be the same people who hold $7.2 trillion in cash deposits and are already using NISA accounts to buy index funds.

An ETF wrapper, favorable tax treatment and broker distribution would provide a familiar path for these investors, and that is what SBI is now building.