Bitcoin’s bear market reversal can be traced to October 10, 2025, a session widely described as the largest liquidation of crypto derivatives ever, during which roughly $19 billion in futures positions were forcibly unwound as prices fell sharply from their all-time highs.

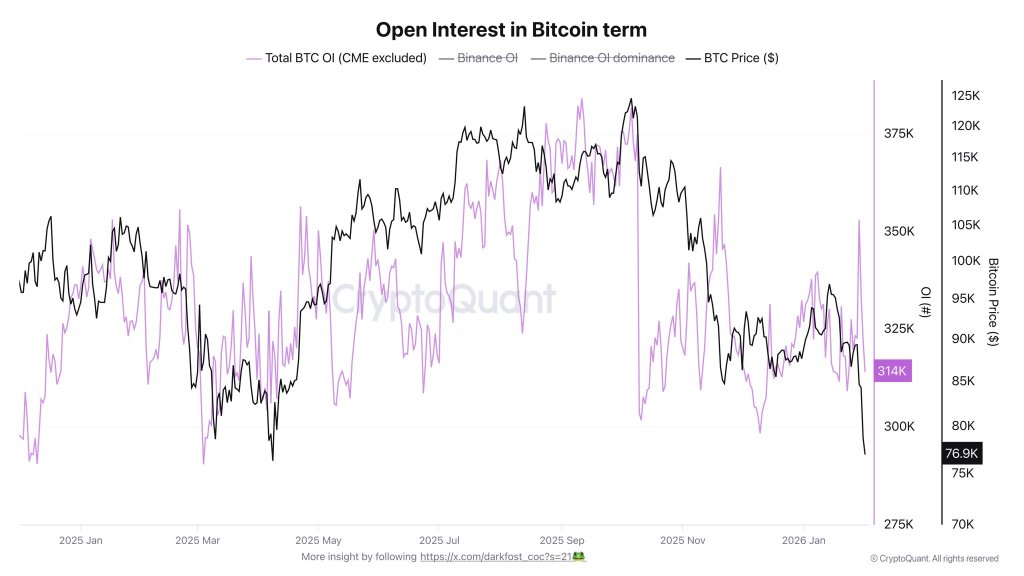

CryptoQuant contributor Darkfost argues The damage was both structural and directional: Open interest fell by around 70,000 BTC in a single day, wiping out months of accumulated debt and leaving speculation struggling to reform. He claims that the October 10 flush was “really the one that pushed BTC into a bear market” due to the speed and magnitude of the liquidity destruction in futures.

Why the Bitcoin Bear Market Started on October 10th

Darkfost pointed to a collapse in open interest measured in BTC terms. “In one day, approximately 70,000 BTC were wiped out of Open Interest, returning it to April 2025 levels,” he wrote. “That’s the equivalent of more than six months of Open Interest accumulation wiped out in one session. Since then, Open Interest has stagnated and struggled to rebuild.”

Related reading

The implication is less about the specific catalyst for the sell-off and more about the market structure afterward. According to Darkfost, the October 10 event was not just a price move; it was a sudden reduction in the market’s ability to sustain leverage, which tends to suppress speculative activity throughout the complex.

“Liquidity destruction in an already uncertain crypto market environment is not conducive to a return of speculation, which is nevertheless an important part of the crypto market,” he added.

That view was echoed by Bitcoin Capital, which responded that “nothing has been the same after 10/10,” adding that “it feels like something has broken.” Darkfost’s response was blunt about the road back: “It needs to be rebuilt and it could take months…”

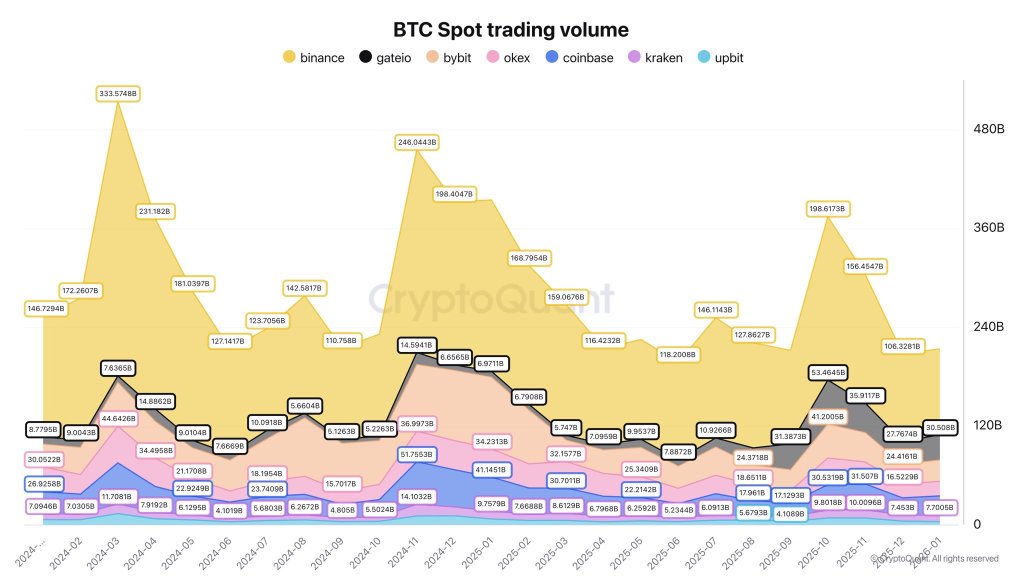

In a follow-up post, Darkfost broadened the lens beyond derivatives and described an environment in which spot participation has also cooled. He said Bitcoin is entering a fifth straight month of correction, with the October 10 event a major driver due to its impact on futures liquidity, but “not the only factor at play.”

Related reading

He flagged broader liquidity pressure through stablecoin flows and supply. According to his figures, stablecoin outflows from exchanges have coincided with a decline of around $10 billion in total stablecoin market capitalization over the same period, which is an additional headwind for risk-taking, especially when risks are already being reduced.

Spot volumes, he argued, tell a similar story of disengagement. Since October, BTC spot volumes have roughly halved, with Binance still holding the largest share at $104 billion. He contrasted that with October levels when Binance’s volume had “reached almost $200 billion,” alongside $53 billion on Gate.io and $47 billion on Bybit.

Darkfost characterized the contraction as a return to “levels that are among the lowest since 2024” and interpreted it as weaker demand rather than simply a lull in activity. The current setup, he wrote, “remains uncertain and does not encourage risk-taking,” arguing that a sustainable recovery would require monitoring liquidity conditions and, “above all,” seeing spot trading volumes return.

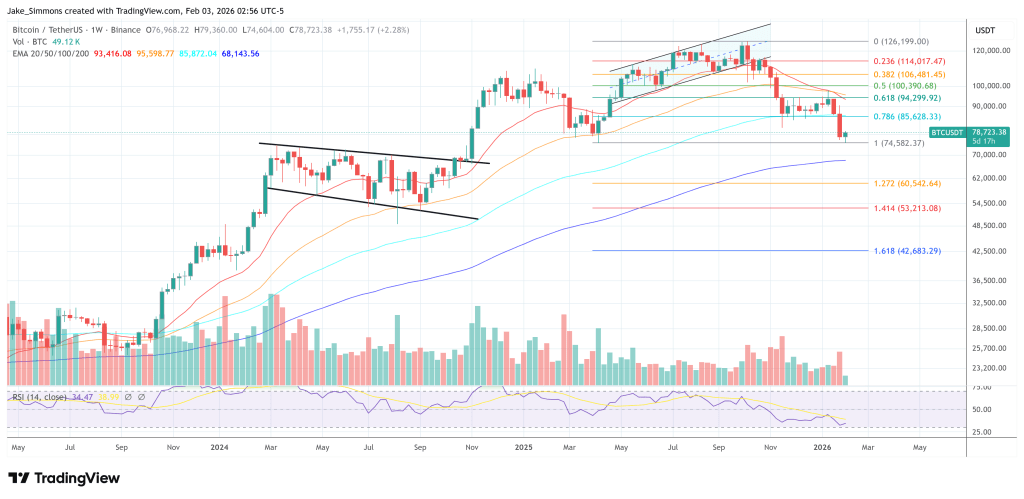

At the time of writing, Bitcoin was trading at $78,723.

Featured image created with DALL.E, chart from TradingView.com