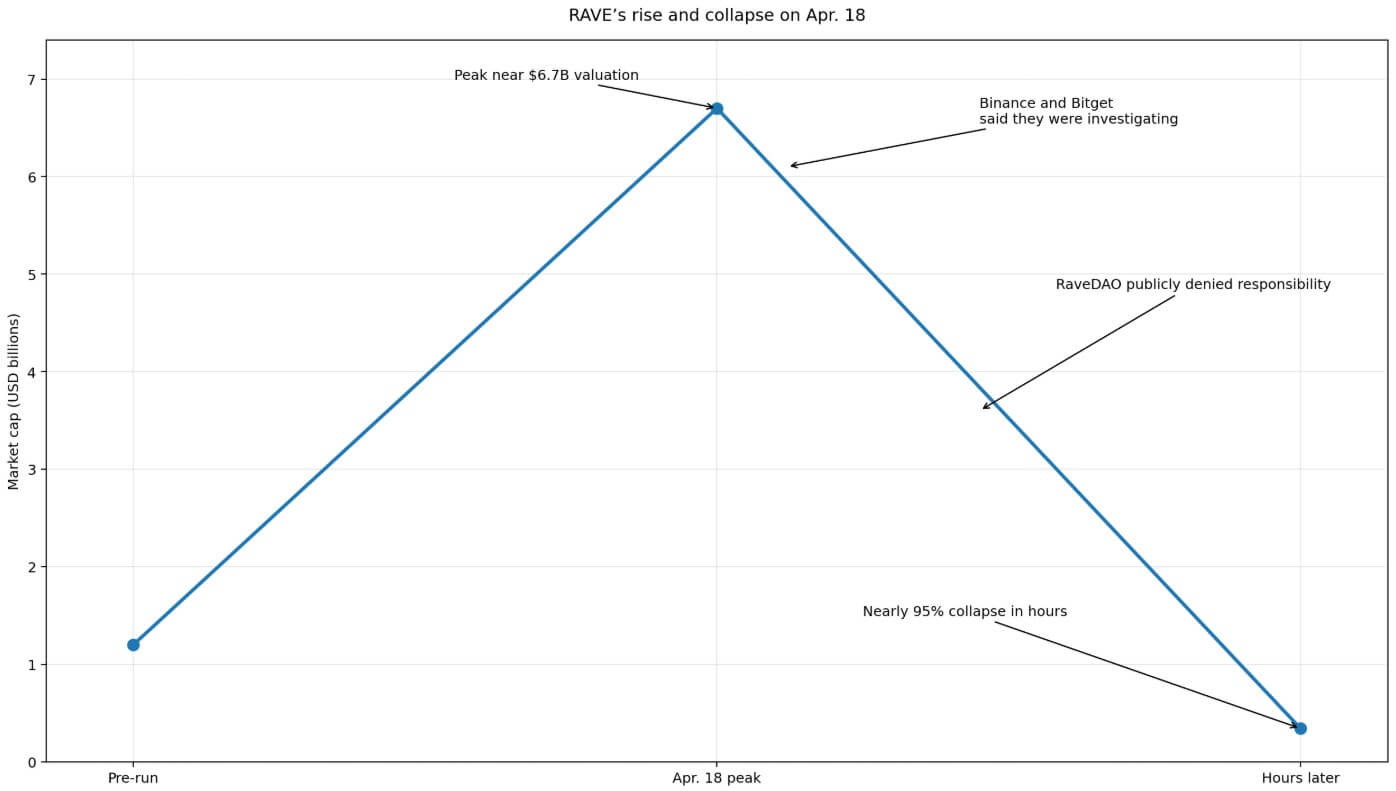

RAVE briefly surpassed its $6.7 billion valuation on April 18 before collapsing nearly 95% in a matter of hours. The market infrastructure surrounding the token, consisting of thin float, concentrated supply, and a live perpetual market, drove the magnitude of both the rally and destruction.

ZachXBT claimed that insiders controlled more than 90% of RAVE’s supply, with about 75% of that in one wallet and about 10% more spread across two connected wallets.

Binance and Bitget both publicly recognized they were investigating, and OKX’s Star Xu stated that the risk driver was his exchange no disruption registered and added a $25,000 bounty to support ZachXBTs research.

RaveDAO publicly denied responsibility.

The mechanism

What traders call “scam coins” is often a repeatable derivative structure.

The loop runs when a token with a concentrated supply and a small effective float receives a perpetual market listing. Bearish traders pile into shorts, and a small push in thin spot liquidity leads to forced buying that sends the price vertically higher.

When the value of the token rises several times, concentrated holders sell at that forced bid.

Binance’s own March 25 red flag guide for market makers expressly warned about coordinated sell-offs across platforms, volume that does not match price behavior, price spikes in limited liquidity and shallow order books that make it easier to artificially depress prices.

CoinGlass data from the post-crash period is visible approximately $3.36 billion in 24-hour futures volume versus $138.9 million in spot volume, a derivatives-to-spot ratio of 24.7x. Open interest of approximately $105.7 million represented approximately 67.3% of the market capitalization.

If roughly 85% of the supply could not realistically be traded, RAVE’s open interest exceeded the mark-to-market value of its effective float.

Using CoinGlass’ post-crash price of around $0.625, 15% of a one billion token supply yields an effective float of around $93.8 million, which is lower than the $105.7 million in open interest on top of that.

This data point does not prove manipulation, but describes a market in which derivatives exposure had outgrown the cash market underneath.

Same structure for three different tokens

On March 23, SIREN’s open interest rose to about $105 million before retreating to $65 million as short positions faced liquidation. Binance and Bybit together recorded approximately $7.1 million in liquidations during that period.

Over 59% of positions were still leaning toward short after the initial push ended, structurally exposing the market to another round of forced hedging.

Phemex reported that there is one wallet cluster checked about 88% of SIREN’s offering and recorded a funding rate of -0.2989%, one of the most visible signs of a ‘crowd-short’ setup. CoinGlass now posts SIREN’s futures-to-spot turnover at about 40.5x.

A deeply negative funding rate means short position holders are paying longs to hold their trades. When this situation combines with concentrated supply in the spot market and low real float, price discovery effectively moves to the derivatives layer, and whoever controls the spot market can choose when to squeeze.

ARIA illustrates the exit side, as the token addresses suspected of manipulating ARIA sold 45.64 million tokens for approximately 5.42 million USDT. The sign fell 91%with market capitalization falling from approximately $315 million to $38.5 million.

Even with that collapse behind it, CoinGlass shows ARIA’s futures-to-spot turnover at around 12.0x, with open interest at around 77.7% of the remaining market cap.

RAVE, SIREN and ARIA map the same research structure, the ongoing crisis and the post-dumping residue at three different moments.

| Token | Phase in the loop | Concentration offer | Futures/spot ratio | OI / market capitalization signal | Evidence of key squeeze/dump | Result |

|---|---|---|---|---|---|---|

| RAASING | Investigation structure/scandal phase | ~75% in one wallet; ~10% in two connected wallets; ~85% estimated from public circulation | 24.7x | OI ~$105.7 million vs. effective float ~$93.8 million — derivatives exceeded the tradable spot market | ZachXBT claimed insider control of more than 90% of the supply; pre-rally exchange deposits; 32M Token Withdrawal During Rally; Binance and Bitget have started investigations | peaked at a valuation of ~$6.7 billion; collapsed ~95% in hours |

| SIREN | Squeeze busy | One wallet cluster controls ~88% of the supply | 40.5x | OI reached ~$105 million at the peak of the squeeze; dropped to ~$65 million after liquidations | Financing rate of -0.2989% (extreme pressure-short signal); ~$7.1 million liquidated via Binance and Bybit; 59%+ of positions are still short after the squeeze | Squeeze performed; market remained largely deficient and was structurally exposed to recurrence |

| ARIA | Relax after the dump | Not made public | 12.0x | OI ~77.7% of the remaining market cap after the collapse | On-chain analysts identified wallets that sold 45.64 million tokens for ~5.42 million USDT in the forced bid | Fell 91%; the market cap dropped from ~$315 million to ~$38.5 million |

The infrastructure that enables the most effective movements in each episode runs through locations where guidelines have already been published that explicitly describe those movements.

Binance’s March 25 guide and the public acknowledgment of the RAVE study both come from the same institution managing the same business tension. Listing volatile, thin-float assets with perpetual markets generates fee income on a large scale.

The futures-to-spot ratios of 24.7x, 40.5x and 12.0x for RAVE, SIREN and ARIA also represent turnover figures. Futures volume on RAVE alone was approximately $3.36 billion in one day after the crash.

Exchanges can point to surveillance and investigations as evidence of responsibility, while retailers can point to the listings themselves as evidence to the contrary.

Two paths from here

As venues adopt float-aware listing standards, with minimum circulation thresholds, portfolio concentration screens and lower leverage limits on thinbook assets, the frequency of these episodes decreases.

Binance’s March 25 red flag framework already gives exchanges a ready-made rationale for such requirements.

The constructive case rests on RAVE becoming the episode that moves listing standards from informal guidelines to enforceable policies, because the reputational costs of another high-profile investigation ultimately exceed the revenue from listing fees.

The opposite path is equally coherent, as the incentive structure that produced RAVE, SIREN, and ARIA is intact. Concentrated holders can repeatedly use currency deposits, narrative catalysts, and crowded short positions to force liquidations.

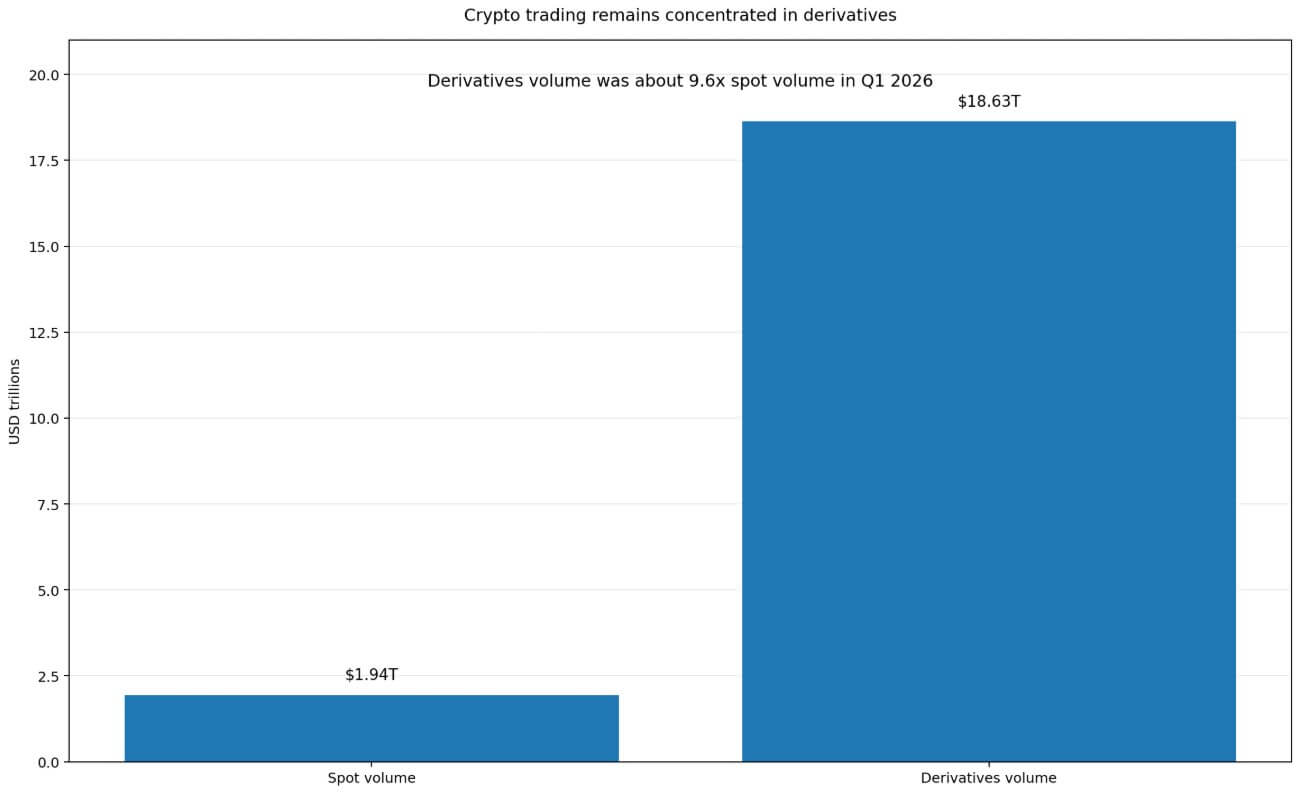

A separate CoinGlass market share report showed that crypto trading activity was at a standstill in the first quarter predominantly concentrated in derivativeswith approximately $18.63 trillion in derivatives volume versus $1.94 trillion in spot volume.

If no hard float or depth requirements emerge, the practical warning sign for traders becomes a recognizable cluster consisting of a top wallet concentration above 80%, futures-to-spot turnover exceeding double digits, extremely negative financing, and price action corresponding to no identifiable catalyst.

That cluster describes what the three episodes had in common: one portfolio cluster controlling an outright majority of the supply, real tradable float controlling price sensitivity, exchange deposits linked to project-linked portfolios prior to the rally, and withdrawals coming in during the forced bid.

Retail shorts that identify this concentration, do the work in the chain and position themselves correctly can still be right on every fundamental point and lose because their timing is exposed to forced buying that they cannot predict.

This asymmetry is a hallmark of asset quoting perp markets where a small number of wallets can dictate the effective supply available to the cash market.

Major venues have now publicly acknowledged that at least one such episode warranted an investigation.