Bitcoin price is entering a pivotal week, with several on-chain models pushing the market bottom just as investors brace for new signals from the Federal Reserve and the US labor market.

The shift has sharpened a debate that no longer focuses just on how low the flagship digital asset might fall, but also on how long the repair process might take even if the worst sales are running low.

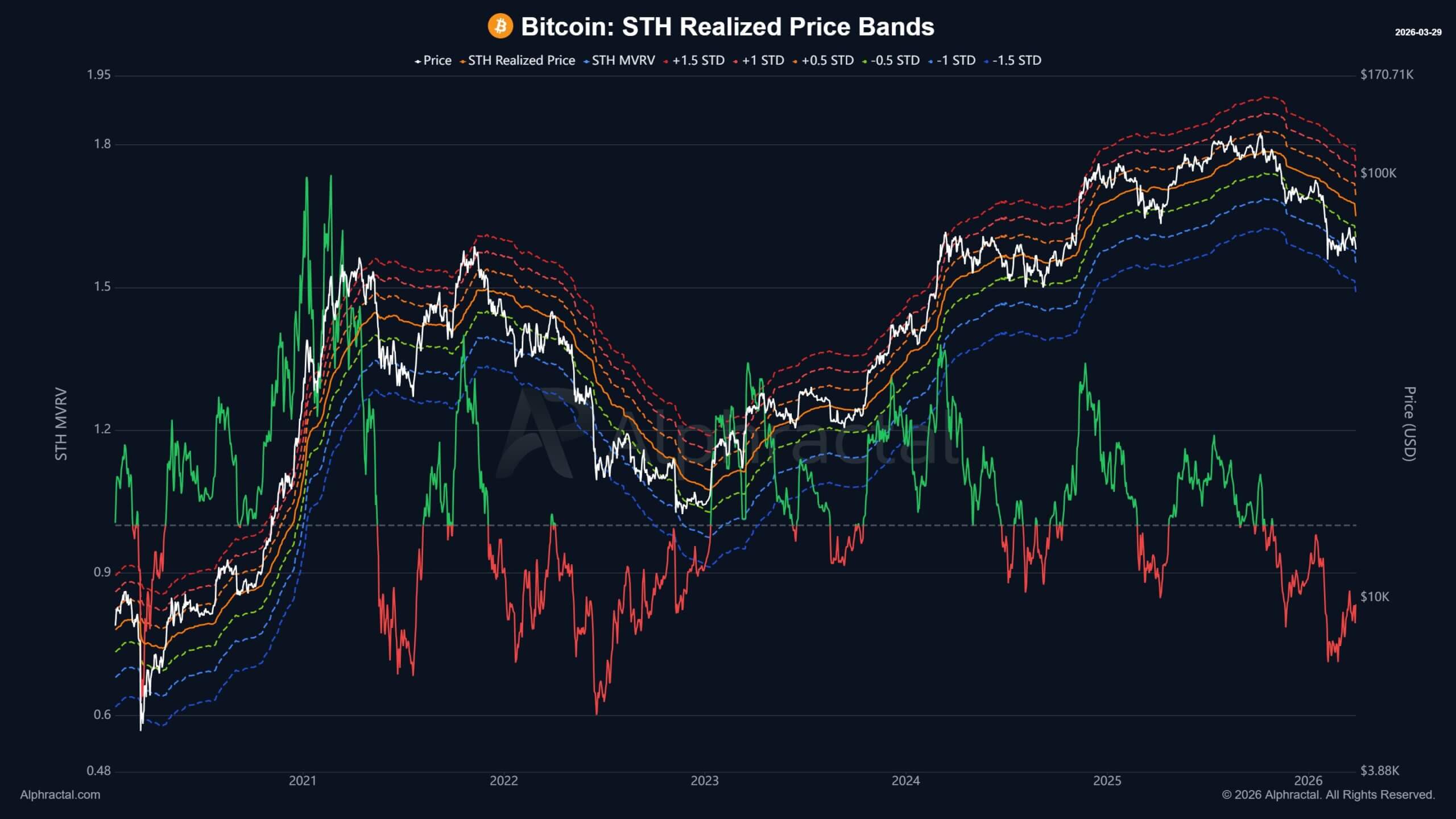

Alpharactal data shows that Bitcoin’s short-term holder realized that price ranges have fallen sharply in recent weeks, dropping to a level where traders are watching for signs of capitulation.

Joao Wedson, the company’s CEO, said previous cycles often completed a capitulation event as Bitcoin approached the lower blue band, creating a strong local buying opportunity. With that band lower, the model points to a possible bottom near $50,000 or slightly below.

Meanwhile, other commonly followed on-chain signals cluster in a similar range. Willy Woo has said Bitcoin could bottom between $46,000 and $54,000, while the CVDD bottom is around $45,500 and continues to rise gradually.

Together, these measures indicate that the zone where deep value buyers could begin to intervene has moved lower amid rising volatility and uncertainty.

Support is emerging, but stress continues to increase

Glassnode’s cost basis data indicates that the market is still trying to build support at higher levels.

According to the company, Bitcoin is trading at the low end of the $60,000 to $70,000 range, where newer buyers have gathered supply, but the size of that cluster remains smaller than the base that formed before stronger recoveries in previous cycles.

However, the pressure beneath the surface has become harder to ignore as BTC continues to struggle.

CEX.io’s Bitcoin Impact Index shows that more than 30% of Bitcoin held by long-term holders is now in the red, the highest share since 2023.

The company said more than 4.6 million Bitcoin owned by long-term holders are underwater, while 47% of all existing Bitcoin are now in losses, matching levels seen during the most stressed weeks of February.

This deterioration is notable because long-term holders have only recently started selling at a profit again.

By the end of last week, the SOPR had fallen to 0.724, wiping out six weeks of improvement and sending long-term holders selling at their biggest losses in three years. Short-term bonds were also under pressure, with realized gains and losses falling to their lowest levels since late January.

The pattern resembles previous degradation phases. CEX.io compared the current setup to mid-2018 and mid-2022, when a similar gap between price action and on-chain belief emerged before Bitcoin suffered another move lower.

The company said the latest jump in its stress index was the sharpest since late January, when Bitcoin recorded one of the toughest periods of 2026.

It is striking that at the same time market liquidity has weakened. Net flows of stablecoins to the exchanges went from a strongly positive daily average to a deeply negative value, removing one of the market’s main supports.

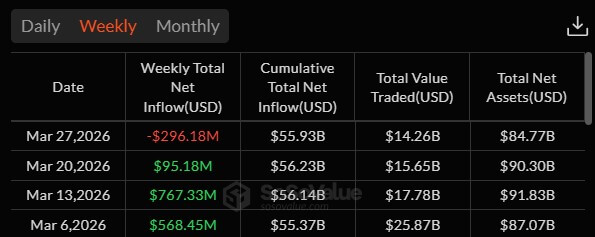

Data from SosoValue showed that spot Bitcoin ETFs posted net outflows of $296 million in the week to March 28, after four straight weeks of inflows, while spot Ethereum ETFs lost $206.58 million.

As institutional flows decline, the burden of support shifts back to spot buyers, long-term holders and short-term hedges.

The mining economy adds another layer of pressure. Between 15% and 20% of miners are now unprofitable after the hash price fell to a post-halving low in February of around $28 per petahash per second per day.

Their higher energy costs have increased the risk of government bond sales, while Bhutan’s steady selling of Bitcoin has reinforced the broader sense of supply glut in the market.

History points to a longer recovery

Meanwhile, caution is not limited to price targets. Ecoinometry, a BTC analysis platform, said A sharp recovery in Bitcoin rarely happens in isolation and typically requires a broader change in the macro environment, often including a shift in monetary policy.

That backdrop has not yet become supportive enough to justify expectations of a quick recovery.

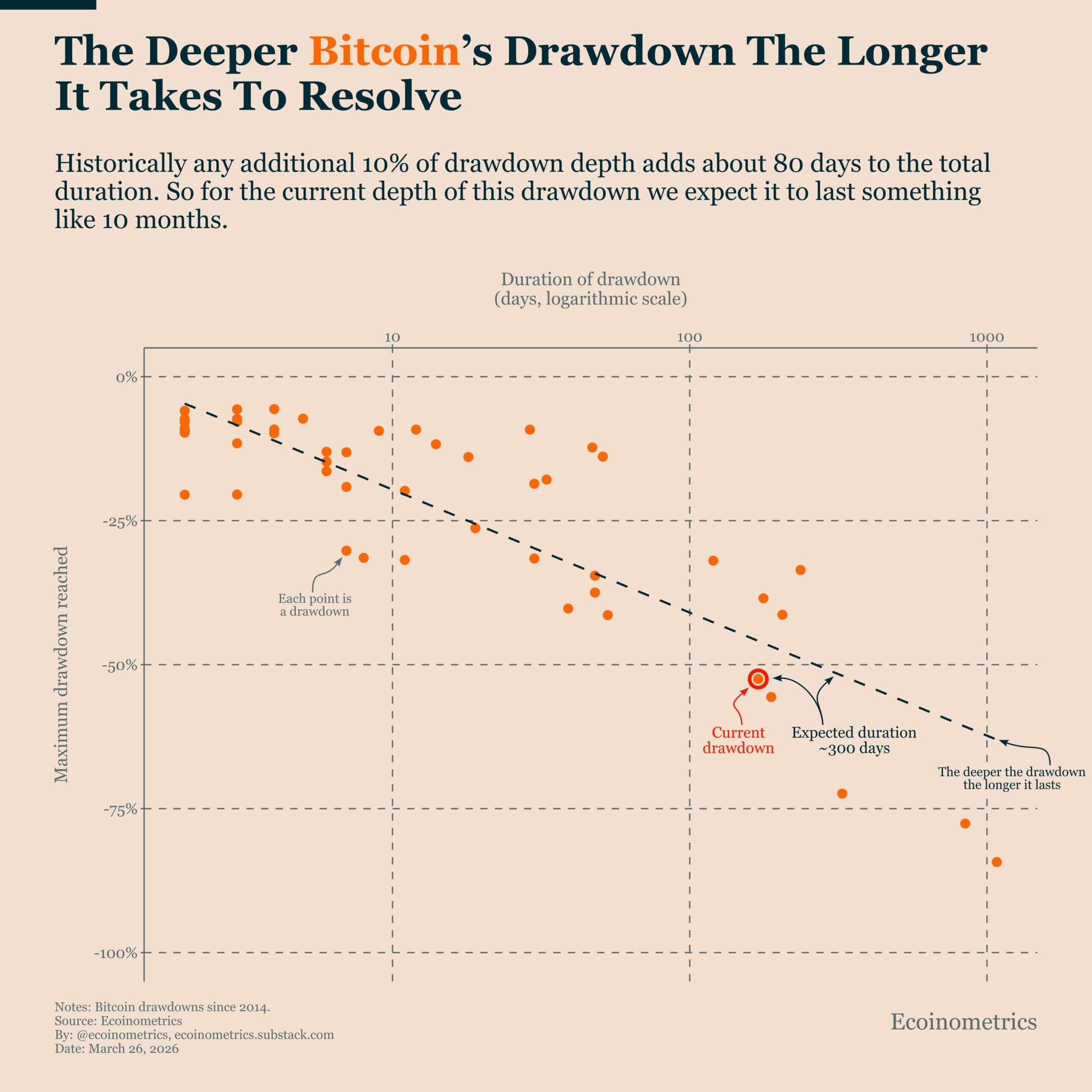

The company’s drawdown analysis helps explain why. Looking at Bitcoin cycles since 2014, Ecoinometrics found a consistent relationship between the depth of a sell-off and the time it takes for the market to fully recover.

For each additional 10% depth of drawdown, the total duration is typically increased by approximately 80 days. On that basis, the current decline implies a recovery period of about 300 days, while the market is only about halfway there.

That doesn’t rule out rallies. Bitcoin can rebound, consolidate and trace several times before a full recovery takes shape.

But the historical pattern argues against a linear return to previous highs. Even if the market moves toward a credible bottom zone, the path out of that zone may be slower and more uneven than bullish traders would like.

This is where the lower bottom and slower repair thesis models start to intersect. A token can be close to a washout area without being ready for a sustained new uptrend.

To achieve this, price support must be accompanied by stronger demand, more stable institutional flows and a macroeconomic backdrop that no longer tightens financial conditions.

The macro calendar takes over

The recovery timeline, already measured in months rather than weeks by several analysts, now hinges on a dense run of U.S. economic data that begins Monday with Fed Chairman Jerome Powell’s appearance at Harvard University.

Federal Reserve Chairman Jerome Powell is planned to participate in a moderated discussion at Harvard University on March 30, and the Bureau of Labor Statistics is expected to release its March employment report on April 3.

In between these events, investors are also looking at consumer confidence data and labor market figures to see if inflationary pressures from higher energy costs are starting to collide with softer growth.

Here the market would try to assess whether policymakers are dealing with a temporary shock or a combination that keeps rates restrictive for longer.

Bitcoin’s link to that debate has become more direct. The flagship digital asset is trading at the lower end of newer buyers’ cost bases, while oil, interest rate and labor market expectations continue to drive risk appetite for several assets.

Softer labor pressures combined with decreasing energy stress could help stabilize financial conditions and give Bitcoin room to maintain support. However, a stronger jobs data and persistent inflation expectations would point in the opposite direction, maintaining macro pressures and leaving the market vulnerable to another move lower.

For now, the Bitcoin market is caught between a market that is starting to look statistically cheap and a macro environment that is yet to have a decisive supportive effect. The models pointing towards $45,000 to $54,000 do not guarantee that the price will trade there.

Instead, they suggest that the market estimate of capitulation has moved lower, and that a sustainable recovery will likely depend as much on the next turn in the macro cycle as on the next bid in crypto itself.