Thomas Lee’s BitMine is turning to the preferred stock market to raise new capital for its Ethereum strategy, offering investors a 9.5% annual payout.

On June 3, the company revealed plans to sell 3 million shares of 9.50% Series A perpetual preferred stock at a stated consideration of $100, creating a potential raise of $300 million.

The shares are expected to trade on the New York Stock Exchange under the ticker BMNP if the listing is approved. Moelis & Company and Cantor are acting as joint lead bookrunners.

If sold in full, the offering would add approximately $28.5 million in annual dividend obligations, which will be paid weekly when declared by BitMine’s board.

The sale comes as the Ethereum Treasury business faces a sharper test of the corporate crypto model. Due to current market conditions, BitMine’s unrealized losses on ETH have exceeded $8 billion after ETH’s decline pushed the asset well below the company’s average purchase price.

Still, this move will deepen the link between the company’s balance sheet, the staking operation and the public market investors asked to finance the next phase of accumulation.

A payout built around Ethereum proceeds

BitMine said the proceeds from the offering may be used for general corporate purposes, including additional purchases of ETH and other digital assets, expansion of its staking and validator infrastructure, working capital, Ethereum-related strategic investments and repurchases of its common shares.

This broad use of the proceeds makes the offer more than just a balance sheet restoration. It could allow BitMine to continue accumulating ETH while market prices remain weak, cementing the company’s role as the largest public Ethereum treasury company.

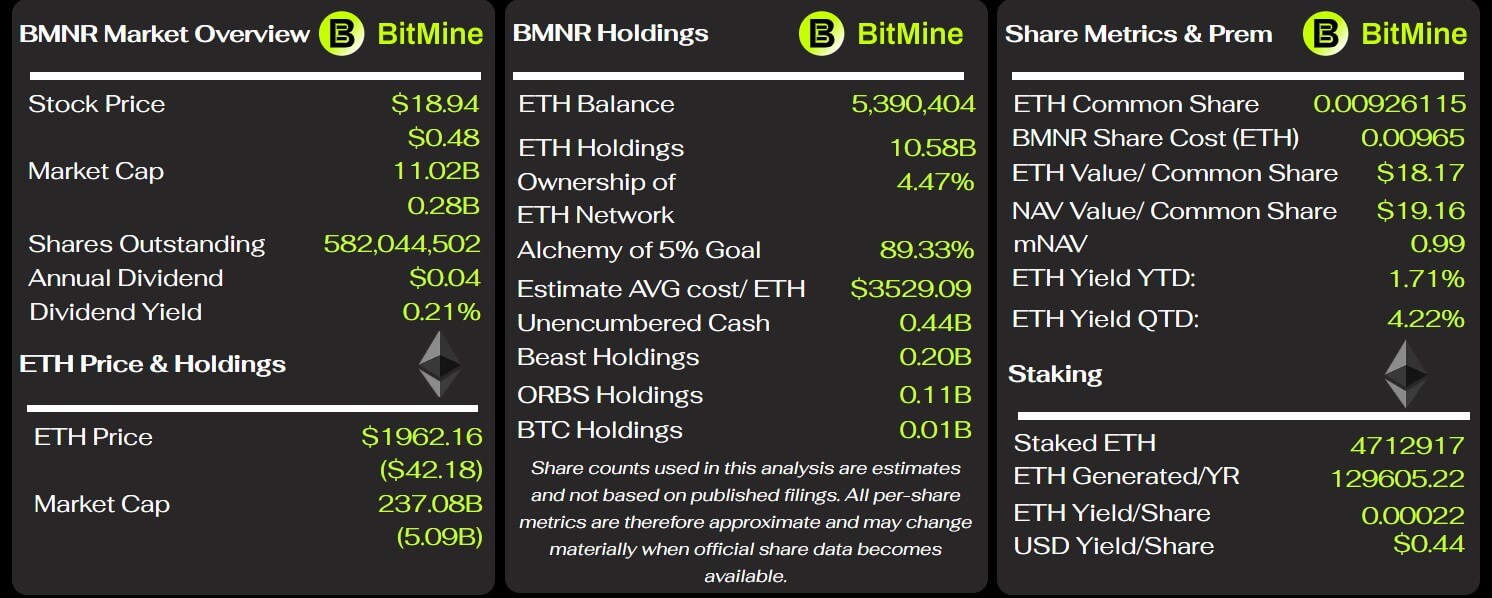

Over the past year, the company has built its ETH portfolio position through aggressive purchasing and currently owns over 5.3 million tokens. This represents approximately 4.5% of ETH’s circulating supply.

Notably, a large portion of that stack has been staked, allowing BitMine to earn protocol rewards while holding the tokens.

Chairman Thomas Lee has argued that these wagering rewards give Ethereum treasury firms an advantage over Bitcoin-focused vehicles. Unlike Bitcoin, ETH can generate returns through staking, allowing a company to earn returns without selling the underlying asset.

That distinction is central to BitMine’s new preferred shares. At a 9.5% coupon, the entire $300 million offering would cost about $548,000 per week in dividends.

BitMine has said that annual staking revenues are in the hundreds of millions of dollars, suggesting that the desired payout is small relative to the revenue the staked ETH could generate under normal market conditions.

Moreover, the broader Ethereum treasury sector is already moving in that direction. According to a study by staking provider Everstake, staking accounted for 60% of publicly traded ETH treasury companies’ disclosed revenues by 2025.

According to the report, the figure comes from companies that separately generated their staking-related revenue, demonstrating how active staking has become a bigger part of the public ETH treasury model.

That revenue mix helps explain why BitMine is banking on Ethereum’s return profile while asking investors to accept a flat 9.5% payout.

The company doesn’t just hold ETH as a treasury reserve. It seeks to convert that reserve into a recurring income base that can support capital market financing.

However, the company’s files also show why the structure is not risk-free.

BitMine does not pledge a special pool of wagering income to the preferred shares. Instead, the filing says dividends can be funded through available cash, ETH yield activities, security sales, future financing, or other sources.

Meanwhile, the company also warns that staking earnings may not be sufficient and staked ETH may not be immediately available for withdrawal or sale during periods of stress.

That caveat is central to the transaction, as the preferred shares convert a portion of BitMine’s Ethereum bet into a recurring cash obligation.

The STRC comparison of the Strategy has limits

BitMine’s move is very similar to the financing model used by Strategy, Michael Saylor’s Bitcoin treasury company, which has repeatedly used preferred stock and other securities to finance crypto accumulation and manage its capital structure.

Both companies use public market tools to translate investor demand for returns into balance sheet capacity to purchase digital assets. Both have sought to create securities that appeal to investors who may want exposure to a crypto treasury without directly owning the underlying token.

Both also operate in a market where the value of their key asset can change significantly before the cash obligation associated with the security matures.

However, this comparison has limits.

Strategy’s STRC Preferred is a variable rate product designed to keep stocks near their stated amount of $100. The dividend rate can be adjusted monthly, giving Strategy a tool to respond if market prices deviate from their levels.

BitMine’s preference set is simpler in one respect and stricter in another. It has a fixed coupon of 9.5%, paid out weekly in arrears when declared, rather than a variable rate that can be reset to affect the trading price.

However, if dividends are not paid, they will accumulate and compound on a weekly basis. The rate for unpaid dividends may increase over time, up to a maximum of 15% per year.

| Function | STRC | BitMine Series A |

|---|---|---|

| Publisher | Strategy, Bitcoin Treasury | BitMine, Ethereum Treasury |

| Security type | Perpetual preference | Perpetual preference |

| Dividend | Variable, currently 11.50% | Fixed 9.50% |

| Payment frequency | Monthly cash | Weekly cash, if stated |

| Goal | General business purposes, including Bitcoin purchases | General business purposes, including ETH/digital assets and staking infrastructure |

| Nominal/declared amount | $100 | $100 |

| Market stabilizing function | Dividend adjusted to keep price around $100 | The liquidation preference is adjusted using the market price formula, but no variable dividend is targeted |

| Repayment | STRC callable at $101 or higher, plus unpaid dividends | BitMine is callable at 110% in the first 18 months, 105% from 18 months to three years, 100% thereafter, plus unpaid dividends |

The preferred stock also includes a liquidation preference that starts at $100 and is adjusted based on a market price formula, without ever dropping below $100.

BitMine can redeem the shares at 110% of the stated amount for the first 18 months, 105% from 18 months to three years, and 100% after three years, plus accrued and unpaid dividends. Holders would also have redemption rights if certain fundamental changes occur.

These terms give BitMine flexibility, but they also show the price of raising capital in a weaker crypto market. A 9.5% payout is high enough to attract the attention of income investors, but also reflects the premium demanded of a company whose main asset base is tied to ETH.