Truth Social’s Bitcoin ETF plan is dead for now, and the fee war offers a more compelling explanation than Yorkville’s official rationale.

President Donald Trump-linked Truth Social Bitcoin ETF filed to withdraw its S-1 registration statement on May 19, saying it would no longer pursue the public offering “at this time.”

For investors looking for a Trump Bitcoin ETF, the filing now points away from basic BTC exposure and toward more complex ETF structures.

Yorkville America described this move as a strategic pivot toward more flexible ETF products under the Investment Company Act of 1940, and the SEC’s withdrawal letter confirms it was voluntary.

Spot Bitcoin and Ethereum ETPs fall outside the scope of the Investment Company Act of 1940, and the SEC directly tells investors that these products are “33 Act commodity trusts,” a legal structure that differs from the ’40 Act investment company framework, regardless of what the industry calls them.

Yorkville cited the ’40 Act’s flexibility, broader distribution and improved investor protections as reasons for concentrating product development there. The ’33 Act structure of spot Bitcoin ETPs was settled before the first US products launched in January 2024.

Bitcoin ETF’s withdrawal therefore looks less like a regulatory surprise than a product economics decision.

| Problem | Yorkville’s official reasoning | Market reading/article corner |

|---|---|---|

| Why the application was withdrawn | Yorkville said it is shifting product development from ’33 Act registrations to more flexible ’40 Act ETF strategies. | The pullback likely reflects the economics of launching a late, simple Bitcoin ETF in a fee-compressed market. |

| Regulatory structure | ’40 Act products offer broader investor protection, flexibility and distribution potential. | Spot Bitcoin and Ethereum ETPs were already known as ’33 Act commodity trust products, so this is valid, but not a new regulatory revelation. |

| Nature of the product withdrawn from the market | The Truth Social Bitcoin ETF is said to no longer be pursuing a public offering “at this time.” | The product was a passive spot BTC wrapper with little differentiation from BlackRock, Fidelity or other existing issuers. |

| Competitive problem | Yorkville did not frame the withdrawal primarily as a matter of compensation or scale. | Morgan Stanley’s 14 basis point product and BlackRock’s IBIT scale of $62.65 billion make it difficult for latecomers to compete. |

| What the twist indicates | Yorkville wants more flexible, differentiated ETF strategies under the ’40 Act. | Truth Social hasn’t abandoned crypto ETFs; it has probably left the least differentiated version of one. |

The Bitcoin ETF War Problem

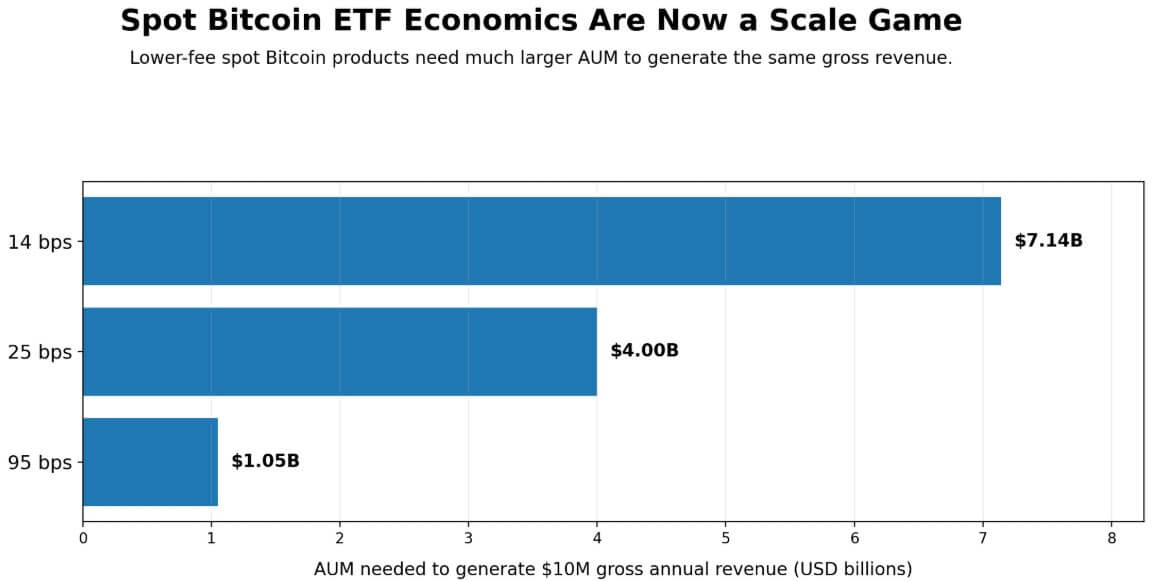

Morgan Stanley’s proposed Bitcoin Trust came in at 14 basis points, below the 15-25 basis point range used by many rivals.

BlackRock’s IBIT carries a management fee of 0.25% against net assets of $62.65 billion, creating economies of scale that will only increase over time. At 14 basis points, a manager needs $7.14 billion in assets under management to generate $10 million in gross annual revenue, and the threshold drops to $4 billion at 25 basis points.

Truth Social’s ETF platform fell far short of the scale needed to compete on those terms. In February, Yorkville managed five Truth Social-branded ETFs with total assets under $50 million, ahead of planned acquisitions of ideologically aligned funds.

That foundation makes it difficult to build the liquidity and tight spreads that institutions demand from Bitcoin exposure products, and distribution rests firmly with BlackRock and Morgan Stanley.

A fund that holds BTC through a custodian and tracks the price of Bitcoin will deliver the same economic outcome regardless of whether the issuer is BlackRock, Fidelity, or a Trump-branded newcomer.

When the product goes to market, competition is limited to fees, liquidity and distribution, categories where latecomers with smaller platforms lose by default.

The Truth Social Cronos Yield Maximizer ETF and Yorkville’s Bitcoin and Ethereum ETF deposits both contributed 0.95% of the fund’s total annual operating expenses while providing staking exposure or multi-asset construction, differentiated structures that justify higher fees.

A higher fee is only defensible with differentiated exposure, and Yorkville appears to have reached the same conclusion on its spot BTC application.

Where the compensation math lands

As regulatory clarity continues to increase and allocators’ interest in packaged crypto exposure expands beyond Bitcoin, Yorkville’s ’40 Act pivot positions it for the next product wave.

Goldman Sachs has filed a Bitcoin product that combines Bitcoin exposure with options-based income, and the approach shows where fee-based sustainable products will come from.

Truth Social has already charted the multi-asset route with the proposed Crypto Blue Chip ETF, which would hold approximately 70% BTC, 15% ETH, 8% SOL, 5% CRO and 2% XRP with stakes on eligible assets, a structure that charges higher fees and occupies a less crowded shelf.

| Scenario | Product path | Reimbursement logic | Required advantage | Likely outcome |

|---|---|---|---|---|

| Strategic repositioning | Yorkville builds ’40 Act crypto products with multi-asset exposure, staking-related features or option income. | Higher fees, such as 0.95%become defensible because the product offers more than just BTC exposure. | Clear differentiation plus sufficient demand from advisors or retail to scale beyond the current small AUM base. | The May 19 pullback looks like a smart reallocation away from exposure to commoditized spot BTC. |

| Niche product outcome | Truth Social is launching tiered crypto ETFs, but they remain small and politically branded. | Higher fees support limited operations, but not major franchise growth. Bee 0.95% on $50 millionthe gross annual turnover is only $475,000. | Loyal niche audience and a steady but modest influx. | The pivot produces viable niche products, but not a major ETF platform. |

| Breakthrough in distribution | Yorkville pairs differentiated crypto products with a major acquisition, seed capital or advisor network partnership. | Higher cost products become scalable as assets under management grow rapidly. | The distribution power is strong enough to compete with large ETF issuers. | Truth Social is becoming a more credible crypto ETF brand than just Bitcoin. |

| Withdraw and you can’t go anywhere | ’40 Act crypto products fail to accumulate meaningful assets, while large issuers dominate spot BTC flows. | The calculation of fees remains theoretical because AUM never reaches a feasible scale. | No; brand recognition cannot be translated into ETF distribution. | The pullback becomes less of a strategic pivot and more of a sign that the ETF economy has boxed Yorkville out of the market. |

In this scenario, the May 19 withdrawal appears to be a deliberate reallocation of archival resources toward products that can generate sustainable revenues from a smaller asset base.

A politically branded multi-asset crypto fund with return components occupies a truly differentiated market position. The brand gains recognition among a specific retail and advisor audience, the differentiated structure justifies the compensation and the compensation makes the business viable.

In the bear scenario, the Truth Social brand could be powerful in the right political context and still fall short of what the ETF distribution machine requires.

Advisors and institutional platforms are allocating crypto ETFs based on liquidity, fees and track record, and less than $50 million in assets under management across five existing ETFs demonstrates the disconnect between brand recognition and the advisor-driven distribution flows that determine ETFs’ long-term success.

If large issuers continue to dominate spot flows and differentiated ’40 Act products prove difficult to scale without an acquisition or partnership, Yorkville’s pivot could produce a series of niche products that never reach the AUM thresholds needed for a viable economy.

At 0.95% on $50 million, gross annual revenue is $475,000, enough to sustain operations but far below what franchise building requires.

Without a major acquisition to seed AUM or a distribution partnership with a large enough advisor network to drive flows, the product roadmap looks good on paper, while the economics remain theoretical.

Truth Social’s crypto product vehicle moved while its ambitions remained intact through the pullback.

The easy phase of spot-launching Bitcoin ETFs is over, and in a market where giants are already offering cheap, liquid Bitcoin exposure, the next successful crypto ETF must offer more than Bitcoin in a different package.

The linchpin of Yorkville’s ’40 Act is the right direction, and its implementation will determine whether it amounts to a strategic repositioning or a retreat with nowhere to go.