The SEC is expected to release an innovation exemption for tokenized stocks as early as this week.

SEC Chairman Paul Atkins and Commissioner Hester Peirce had outlined the plan in February, describing a temporary, limited framework with volume limits, whitelisting buyers and sellers, automated market makers and temporary relief while the SEC develops longer-term rules.

Atkins confirmed in April that the agency was “on the verge” of releasing a cabin framework for compliant on-chain trading of tokenized securities.

Bloomberg Law reported the move on May 18which represents the clearest signal of crypto-adjacent securities policy in years, with implications that reach much further symbolic prizes.

What the exemption actually is

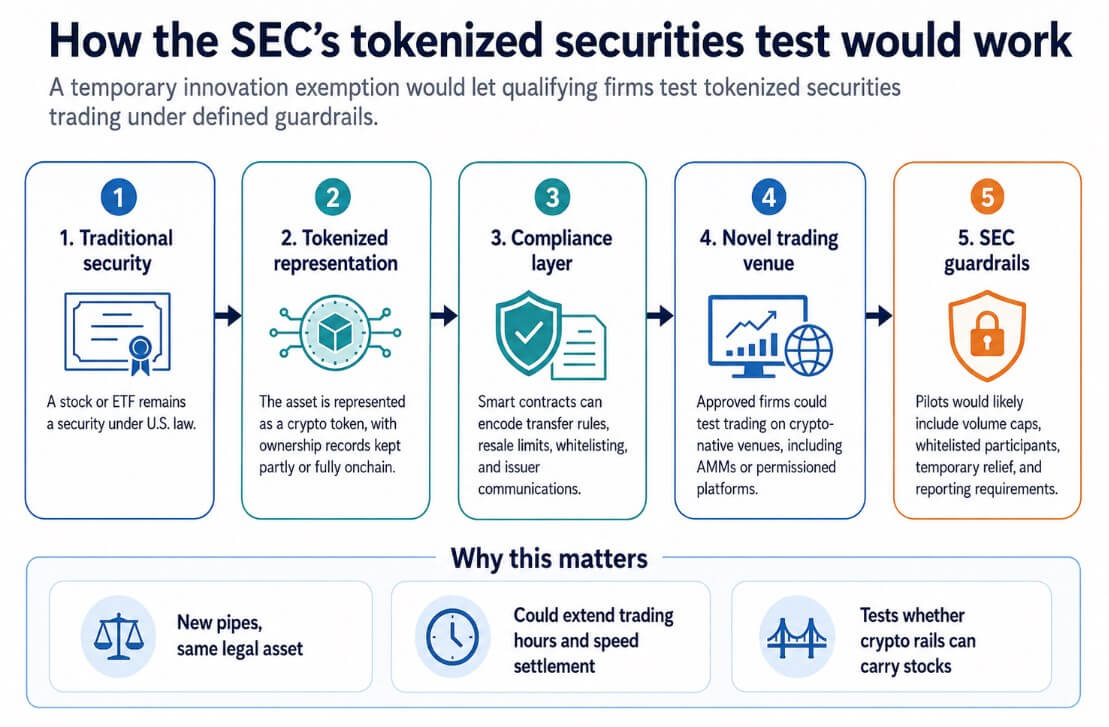

SEC staff defined tokenized securities in January 2026 as traditional securities represented as crypto assets, where crypto networks maintain some or all of the ownership information.

The legal status of the asset follows this regardless of its form, so federal securities laws apply regardless of whether a stock is on a blockchain or in a DTC account.

The innovation exemption would allow qualifying companies to test trading of tokenized securities on new platforms, including AMMs and potentially permissionless public blockchains, within defined parameters.

Atkins explicitly discussed embedding compliance controls directly into the smart contract code, including resale restrictions and communications between issuers and holders.

A tokenized security can include its own eligibility rules, transfer restrictions, and compliance logic, which are automatically provided at the time of transfer.

U.S. stocks have already moved from T+2 to T+1 in 2024, and the SEC has proposed the move as a way to make the market more resilient by reducing time, credit exposure and liquidity risk.

Tokenization further extends this logic with longer trading windows, near-instant settlement, fractional access, and programmable post-trade processing.

Nasdaq received SEC approval in March 2026 to trade certain DTC-eligible securities in token form on the same order book as traditional stocks, while maintaining T+1 settlement.

NYSE parent company ICE is separately developing a tokenized securities platform focused on 24/7 operations, instant settlement, dollar-sized orders and stablecoin-based financing, pending regulatory approval.

Incumbent exchanges are building their own versions of the next pipe before crypto platforms can claim the market.

Coinbase sought SEC approval in 2025 to offer tokenized equity, a move that would reportedly put it in direct competition with retail brokers.

Kraken’s xStocks platform already offers 100 fully supported tokenized US stocks and ETFs outside the US market, and Robinhood has launched EU stock tokens while building a layer 2 blockchain for tokenization of real assets.

The SEC exemption would determine whether these crypto-native models can compete for U.S. investors within a regulated framework.

The window

Data from DefiLlama estimates the on-chain RWA market at nearly $30 billion, representing just 0.02% of global equity value, while SIFMA’s global stock market capitalization in 2024 was $126.7 trillion.

The stock-token segment is still in its early stages and the exemption could determine whether tokenized stocks expand into a regulated extension of US equities or remain a crypto side market.

SEC staff distinguishes issuer-sponsored tokenized securities, where the token represents a direct claim on the underlying stock, from third-party products, including custodial notes, linked securities and synthetic derivatives.

Robinhood’s EU stock tokens carry that distinction explicitly in their disclosures: they are derivatives that expose investors to counterparty and insolvency risks associated with Robinhood’s financial position.

A tokenized share can look identical in an app and have completely different legal rights depending on its structure.

Crypto rails enter the securities stack, or will incumbents control the upgrade?

If the pilots are successful and the exemption is expanded, issuer-sponsored tokenized equities and custodial tokenized securities will have clearer regulatory pathways, and crypto-native platforms will compete for tokenized equity flows alongside Nasdaq’s DTC-compatible model and ICE’s parallel digital platform.

Stablecoin settlement becomes a standard post-trade mechanism for liquid securities, and smart contract networks carrying tokenized shares become a sustainable infrastructure.

The winners extend beyond the companies launching products. Stablecoin issuers are gaining a settlement use case within regulated securities markets, and high-throughput programmable chains are benefiting from sustained demand from securities settlement activities.

Wallet providers and tokenization agents are entering a market previously controlled by broker-dealers, and the crypto-native trading stack is gaining a securities-grade use case, legitimizing it across jurisdictions.

However, if the SEC allows tokenization primarily through Nasdaq’s DTC-compatible model and ICE’s regulated venue. The innovation exemption for crypto-native and AMM-based trading remains limited, has a heavy volume cap or is limited to institutional participants.

Tokenization modernizes settlement mechanisms, and competitiveness for crypto-native platforms remains limited.

Broad exemptions for tokenized trading could undermine investor protection and market stability if trading in tokenized securities falls outside the long-standing protections of the securities markets.

Peirce warned that third-party tokenized shares could expose holders to counterparty and insolvency risks related to the tokenizing intermediary’s own financial position.

These risks provide regulators with a sustainable justification for keeping crypto-native platforms on the margins while incumbents absorb the technology upgrade.

The competitive card

Three models are now competing for the next effects pipe.

Nasdaq’s DTC-compatible approach keeps tokenized and traditional stocks on the same order book, with incumbents controlling settlement. ICE’s parallel digital location focuses on 24/7 operations and stablecoin financing. The crypto-native model tests whether securities can be traded on-chain via crypto infrastructure under SEC conditions.

| Model | Key players | How it works | What it means |

|---|---|---|---|

| Nasdaq/DTC compatible model | Nasdaq, DTC, broker-dealers | Tokenized and traditional stocks trade on the same order book; Maintain T+1 settlement | The incumbents are modernizing the pipeline without changing the market structure too much |

| ICE/NYSE digital location model | ICE, NYSE, regulated intermediaries | Parallel tokenized securities platform focused on 24/7 operations, instant settlement, dollar-sized orders and stablecoin financing | Wall Street is building its own onchain venue before crypto platforms take the lead |

| Crypto-native model | Coinbase-style platforms, Kraken-style products, AMMs, wallets, tokenization agents | Tokenized securities trading via crypto infrastructure under SEC exempt conditions | Crypto rails have a chance to compete for power in the stock market |

The SEC exemption determines which of these models can legally compete, and the scope of that provision sets the limit of the opening.

Atkins framed the exemption by allowing the market to discover whether the crypto infrastructure can transport shares more efficiently than the current set of location-clearing-custody.

That test, conducted under regulator supervision, with whitelisting of participants and volume limits, is the policy event that Bloomberg reported.

The SEC is letting crypto rails compete to carry stocks, and the exemption will measure whether they can win.