Kalshi is reportedly preparing to offer US perpetual crypto futures, while Polymarket today announced that perpetual contracts are coming to its platform and has opened signups for early access.

Hyperliquid’s documents support trading of outcome tokens alongside mainnet-implemented perpetuals via the Hyperliquid Improvement Proposal 4 (HIP-4).

Pump.fun has evolved in recent years into a social trading environment where users can browse coins, follow makers, watch live streams and trade tokens without leaving the app.

The common denominator of all four platforms is the logic of keeping users in a continuous speculative loop, capturing every stage of their risk appetite and making the exit costs so high that they never have to go anywhere else.

The economics driving convergence

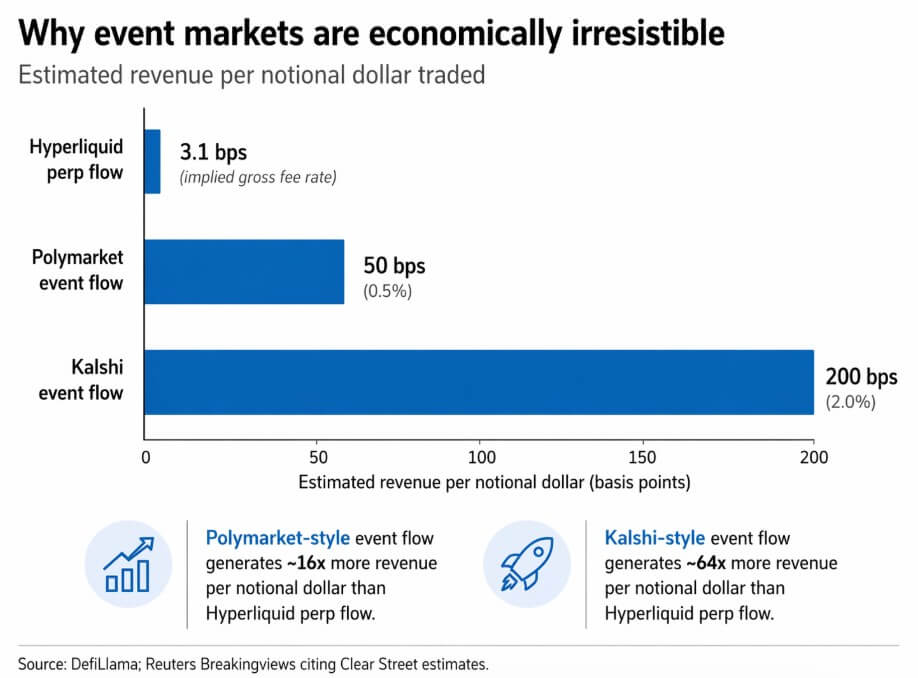

Hyperliquid currently books approximately $191 billion in 30-day perp volume, $61 million in 30-day fees and approximately $7.35 billion in open interest, which equates to an implied gross fee of approximately 3.1 basis points.

For event markets, Clear Street estimates 2026 volumes at $96 billion for Kalshi and $84 billion for Polymarket, with take rates of about 2% and 0.5%respectively.

At these speeds, the Kalshi-style event stream generates roughly 64 times as much revenue per notional dollar as Hyperliquid’s perp stream, and the Polymarket-style stream is about 16 times richer.

A perp exchange that adds event contracts is trying to attract a higher-margin flow from the same users it already has, while a prediction market platform that goes to perpetuals adds a continuous layer of revenue to a business that otherwise only earns when individual events are resolved.

The Financial Times reported in March that 5- and 15-minute crypto bets on Polymarket and Kalshi approximately $70 million in daily trading volume and accounted for more than half of the total trading on those platforms.

Short-term contracts now account for the majority of trading activity on both platforms, and their dominance helps explain why Hyperliquid’s testnet papers include a recurring HYPE price binary with a 3-minute settlement period.

The direction of travel in every major location is toward shorter, more repeatable, and more bankable cycles.

The moment of convergence

Hyperliquid built its identity on permissionless perpetuals and the deepest order book in crypto. The Mainnet HIP-3 protocol allows builders to implement custom offender contracts without approval.

The testnet is now documenting trading of outcome tokens with fee structures that only charge fees at closing or settlement, an architecture that makes opening event contracts cheap and expensive to walk away from.

Mainnet implementation of outcome contracts is just one decision away because the fee structure, settlement logic, and contract architecture are already documented.

Kalshi built his position through regulated event contracts overseen by the CFTC, running crypto forecasts on weekly and monthly horizons, and winning a federal legal battle when the Third Circuit ruled that the federal derivatives law prevents New Jersey’s attempt to block its sporting event contracts.

Kalshi is now reportedly preparing to add crypto perpetual futures, importing the always-on leveraged product that made crypto venues sticky.

Polymarket completed the picture his announcementwhich states that users can now ‘use’ the future, as they enter perpetual futures and open early access sign-ups.

The platform already manages 5-minute and 15-minute Bitcoin directional markets in addition to longer-horizon political and macro issues, conditioning the user base for short-term, high-frequency speculation.

Perpetuals extend that behavior into a continuous loop, as two of the largest prediction market platforms now explicitly target the same product stack that made crypto offenders dominant.

Pump.fun closes the circle from the dispensing side. The Android app bundles coin creation, creator tracking, livestream discovery, and memecoin trading into a single interface. Her own disclosures describe memecoins as “for entertainment purposes only.”

That language acts as a positioning statement about what the platform actually sells.

| Platform | Original core product | What it added/adds | How it keeps users informed | Primary monetization logic | Regulatory posture/risk |

|---|---|---|---|---|---|

| Hyperfluid | Perpetual futures/on-chain order book | Trade outcome tokens via HIP-4 on testnet, alongside perpetrators deployed by the mainnet builder | Users can stay in one location for continuous offender trading and betting on shorter duration outcomes | Perp fees for high volumes, with event-style products potentially generating richer revenue per user | Exposure to offshore/on-chain derivatives; outcome products raise additional classification questions |

| Kalshi | Regulated event contracts | It is reportedly preparing crypto perpetual futures | Combines betting on episodic events with always-on leveraged trading | High-margin event contract flow, where perpetrators continuously add revenue between event cycles | CFTC-backed framework, but active state law conflict over gambling classification |

| Polymarkt | Prediction markets | Announced perpetual contracts and early access sign-ups | Users are already being forced into frequent short-term crypto bets, with perpetrators expanding this into a continuous loop | Involvement in the prediction market plus volume and retention of future offenders | High regulatory ambiguity; added perpetrator functionality could increase exposure |

| Pumping fun | Memecoin launch pad | Social trading environment with browsing, creator following, live streams and trading in one app | Users can create, discover, follow, view and trade without leaving the interface | Attention grabbing, trading activity and repeat speculative participation | Memecoin research; “For entertainment purposes only” framing emphasizes the perception associated with gambling |

The regulatory fault line

The regulatory environment underlying this convergence is an active clash between two frameworks with incompatible principles.

On March 12, the CFTC opened a preliminary notice of proposed rulemaking in the area of prediction markets and claimed exclusive federal jurisdiction over it.

On April 6, the Third Circuit sided with Kalshi on jurisdictional grounds, although the dissenting judge wrote that Kalshi’s offering was virtually indistinguishable from sportsbook gambling.

On April 21, the New York Attorney General sued Coinbase and Gemini, arguing that their prediction market products constitute illegal gambling under state law and are accessible to users ages 18 to 20.

CME’s Terry Duffy has publicly called for clearer rules distinguishing event contracting from gambling, even as CME launched an event contracting platform with FanDuel.

Federal derivatives logic treats these instruments as market infrastructure, while state gambling logic treats them as gambling products that require casino-style licenses.

As more features are bundled onto fewer platforms, every new product launch becomes a matter of jurisdiction.

Polymarket’s announcement exacerbates that problem considerably. Existing short-duration crypto markets are already in regulatory limbo, and putting perpetuals on a product line that attorneys general are actively monitoring because gambling only increases exposure.

The roads ahead

If the CFTC’s regulations provide workable definitions and preventive clarity, the onshore super app model will accelerate. Kalshi adds perpetuals, Hyperliquid expands its outcome infrastructure to mainnet, and Polymarket’s perp launch deepens a product stack already used by millions for short-horizon betting.

Distribution partnerships normalize prediction markets as a standard brokerage feature, such as Plus500 distributing Kalshi contracts, and Fox integrates Kalshi data. In that environment, the venue that bundles perpetrators, event contracts, and asset creation into one interface captures a dominant share of retail speculative attention.

Bitcoin acts as a bridge asset while serving as a perpetual underlying asset and a prediction market feed.

| Scenario | Regulatory trigger | What happens to Hyperliquid | What happens to Kalshi / Polymarket | What it means for Bitcoin | Who benefits |

|---|---|---|---|---|---|

| Bull/onshore super app acceleration | The CFTC regulations provide workable definitions and stronger federal clarity | The outcome infrastructure moves from testnet to mainnet, moving Hyperliquid beyond pure perpetrators | Kalshi adds perpetrators; Polymarket deepens its short horizon plus leveraged stack | Bitcoin becomes the standard bridge between perpetrators, binaries and prediction contracts | Platforms with the broadest bundled product stack and strongest user retention |

| Bear/state crackdown and forced separation | The New York lawsuit is a success or inspires broader state enforcement | Hyperliquid is under increased pressure when it comes to how results-oriented products are positioned and made accessible | The expansion of Polymarket perpetrators becomes an immediate target; Kalshi is leaning more on federal protection, but still faces political heat | Bitcoin remains central, but has access to fragments across product types and jurisdictions | Locations that require a lot of compliance and companies that can segment products based on the legal regime |

The bear case is sweeping the states. If the New York lawsuit succeeds or prompts coordinated enforcement by other attorneys general, Polymarket’s expanding perpetrators will become an immediate target.

Separating high-risk prediction products from core trading to simultaneously comply with different regulatory regimes becomes the only viable path.

The locations that built compliance moats early would have structural benefits. At the same time, those who relied on regulatory ambiguity would face difficult choices about which license to choose and which products to cut.

Bitcoin is at the center of this race because it is the most liquid asset across all these platforms.

Any new user who understands Bitcoin price movements can immediately enter into a 15-minute contract on Polymarket, a Bitcoin dapper on Hyperliquid, or a “How High Will Bitcoin Get This Month?” contract on Kalshi.